Common Tax Receipt Mistakes and How to Avoid Them

Published on

December 17, 2024

Last updated on

March 2, 2026

Donation receipting is one of the most common compliance failures among Canadian registered charities. A single error — a missing serial number, an incorrect eligible amount, or a receipt issued without active registration — can trigger a CRA audit or result in serious penalties, including suspension of receipting privileges. Whether your charity is new or well-established, understanding the rules around gifting and receipting is essential to protecting your registered status.

This guide covers the most common tax receipt mistakes Canadian charities make, what the CRA requires on every official donation receipt, and exactly how to stay compliant.

What Does Receiving a Gift Entail?

Before issuing an official donation receipt, a charity or qualified donee must verify that the contribution meets the definition of a gift under the Income Tax Act. Additionally, the charity needs to determine the eligible amount of the gift, which depends on three critical factors:

- Fair Market Value of the Donated Property The fair market value is the price the donated property would fetch in an open market between a willing buyer and seller. An accurate valuation is essential to determine the correct receiptable amount.

- Fair Market Value of Any Advantage Given to the Donor If the donor receives something in return for their contribution, such as event tickets, promotional items, or services, the value of this advantage must be deducted from the fair market value of the gift. The remaining amount is the eligible amount for receipting.

- Application of the Deemed Fair Market Value Rule When non-cash gifts like artwork, securities, or property are donated, the deemed fair market value rule may apply. This rule ensures that the receipt reflects the property's value on the donation date or the donor's cost, whichever is lower, preventing inflated valuations.

Helpful Resources:

To better understand what qualifies as a gift and how to assess it, consult:

How to Properly Issue Donation Receipts

Issuing donation receipts is one of the most scrutinized aspects of charity compliance in Canada. Improper receipting is not only a common mistake but also a frequent reason for audits by the Canada Revenue Agency (CRA). Following the guidelines below will help ensure your charity remains compliant.

Who Can Issue Donation Receipts?

Only registered charities or qualified donees, such as certain public organizations, may issue official donation receipts. If your organization isn't registered, it cannot provide tax-deductible receipts.

Mandatory Information on Donation Receipts

Every official donation receipt must include specific details as required under the Income Tax Act:

- The charity's name and registration number

- The date of the donation

- The donor's name and address

- A detailed description of any non-cash gift

- The fair market value of the gift and any advantage received by the donor

- The eligible amount of the gift for tax purposes

- A unique serial number for the receipt

For guidance, refer to CRA's Sample Official Donation Receipts. These examples can help your charity prepare compliant receipts.

✅ Quick Reference: Official Donation Receipt Checklist

Use this checklist every time your charity issues an official donation receipt to ensure full CRA compliance:

- [ ] Charity's full legal name

- [ ] Charity's CRA registration number

- [ ] Unique serial number (each receipt must have its own number — never reuse)

- [ ] Statement that it is an official receipt for income tax purposes

- [ ] City or town where the receipt was issued

- [ ] Date the donation was received

- [ ] Date the receipt was issued (if different from donation date)

- [ ] Donor's full legal name

- [ ] Donor's full address

- [ ] Description of donated property (for non-cash gifts)

- [ ] Fair market value of the donated property

- [ ] Fair market value of any advantage provided to the donor

- [ ] Eligible amount of the gift (FMV minus advantage)

- [ ] Signature of an authorized charity representative (recommended)

If your charity issues electronic receipts by email, all of the above still applies. No special CRA approval is required for digital receipts, but they must meet the exact same standards as paper ones.

No Obligation to Issue Receipts

Interestingly, there's no legal requirement for charities to issue donation receipts. However, donors cannot claim a charitable tax credit or deduction without an official receipt. While timely issuance of receipts is not mandatory, doing so promptly fosters goodwill with donors.

Tools to Simplify Receipting

To streamline the receipting process, use CRA's Checklist for Issuing Complete and Accurate Donation Receipts. This ensures every receipt issued meets compliance standards.

Common Mistakes to Avoid

To prevent issues during audits or donor disputes, watch for these common errors:

1. Inaccurate Valuation of Non-Cash Gifts

Always seek professional appraisals for high-value or unique non-cash donations to determine fair market value accurately. Using an inflated or estimated value without proper documentation is one of the most frequent audit triggers. See our guide on determining fair market value for non-cash gifts for more detail.

2. Omitting Required Information on Receipts

Cross-check every receipt against the CRA's checklist to ensure all mandatory details are included. Even one missing field — such as the city of issue or a serial number — can make a receipt non-compliant.

3. Improper Deduction of Donor Advantages

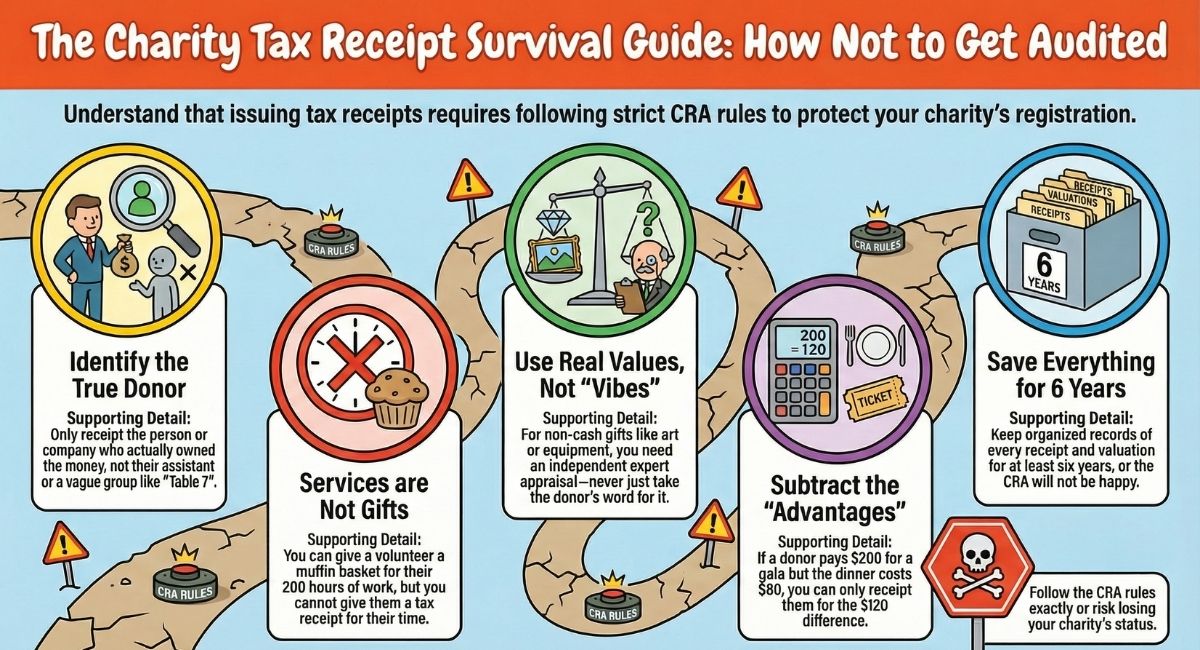

If the donor receives any benefit — such as merchandise, event tickets, or dinner — the fair market value of that benefit must be subtracted from the donation amount. Only the eligible amount (the remainder) can be receipted. This is also known as split receipting. Learn more about split receipting rules here.

4. Issuing Receipts Without Active Registration

Double-check that your charity's CRA registration status is active before issuing any donation receipts. If your registration has been revoked or suspended, issuing receipts is not permitted and can result in serious penalties.

5. Backdating Donation Receipts

Every official donation receipt must reflect the actual date the gift was received by the charity. Backdating a receipt to a prior tax year — for example, issuing a receipt dated December 31 for a donation received in January — is a serious violation of the Income Tax Act. The CRA considers this a false receipt, which can result in revocation of charitable status. Receipts must always be dated on or after the date the donation was actually received.

6. Issuing Receipts for Volunteer Time or Donated Services

This is one of the most common and well-intentioned mistakes charities make. Volunteer hours and donated services do not qualify as gifts under the Income Tax Act and cannot be receipted under any circumstances. The CRA is explicit on this point: only a transfer of property (cash, securities, real property, or certain other assets) qualifies as a gift. If a volunteer or service provider wishes to donate, they must first invoice the charity, the charity must pay that invoice, and the individual may then donate the funds back to the charity — at which point a receipt may be issued for the cash donation.

7. Issuing Receipts for Membership Fees

Membership fees generally do not qualify as charitable gifts because the member receives something of value in return — access to programs, services, or benefits. Only the portion of the membership fee that genuinely exceeds the fair market value of the membership benefits may be receipted. If the benefits of membership are equal to or greater than the fee paid, no receipt can be issued. Charities must assess membership benefits carefully and document their fair market value.

8. Receipting a Pledge Before Payment Is Received

A pledge or promise to donate is not a gift. A charitable donation receipt cannot be issued until the actual donation has been received by the charity. Issuing a receipt for a pledge — even one that is very likely to be fulfilled — is not permitted under the Income Tax Act. The receipt must be dated on or after the date the funds or property are actually received.

9. Missing, Incorrect, or Duplicate Serial Numbers

Every official donation receipt must carry a unique serial number. The CRA uses serial numbers to track receipts during audits. Reusing a serial number, skipping numbers without documentation, or omitting serial numbers entirely are compliance errors that raise red flags. Your charity should maintain a sequential receipt register and keep records of all cancelled or voided receipts as well.

10. Receipting Ineligible Donations — Raffle Tickets and Auction Items

Raffle or lottery ticket purchases are not charitable gifts and cannot be receipted under any circumstances. The purchase of a raffle ticket is a transaction, not a donation, and the CRA is clear that no official receipt may be issued. For auction items, the rules are different but still restricted: only the amount paid over and above the fair market value of the item received is eligible for a receipt. If a donor pays $200 for an item worth $200, no receipt can be issued. If they pay $300 for that same item, only $100 may be receipted. See our full article on issuing tax receipts for auction items for more detail.

11. Failing to Meet Electronic Receipt Requirements

Many charities now issue donation receipts by email or through their donor management software. Electronic receipts are permitted by the CRA without any special approval, but they must contain every mandatory field that a paper receipt requires. A PDF attached to an email, a receipt generated through a donation platform, or a receipt portal login — all must meet the same standard. The format does not matter; the content does. Ensure your receipting software or template includes all required fields and generates a unique serial number for each receipt issued.

How to Correct a Mistake on a Donation Receipt

Even with the best systems in place, errors on donation receipts can happen. The good news is that the CRA does allow registered charities to correct receipting mistakes — but only in a specific way.

You cannot simply cross out the error, use correction fluid (white-out), or edit a digital receipt and re-send it. The correct process is:

- Cancel the original receipt. Mark the original receipt as "cancelled" and keep it on file. Your charity's records must contain the cancelled copy.

- Issue a new receipt. Prepare a corrected receipt with a new, unique serial number. The corrected receipt should clearly note that it replaces the cancelled receipt (referencing the original serial number is good practice).

- Retain both copies. Keep the cancelled receipt and the replacement receipt in your records. The CRA expects to see both if your charity is audited.

Charities are required to retain copies of all donation receipts — including cancelled ones — for a minimum of two years after the last tax year in which the receipt could be used. Best practice is to retain all receipting records for at least six years.

For a detailed walkthrough of this process, see our article: How Can a Registered Charity Correct Mistakes on Tax Receipts?

Why Compliance Matters

Non-compliance with gifting and receipting rules can lead to severe consequences for Canadian charities, including fines, suspension of receipting privileges, or loss of registered status. Staying informed and following the CRA's guidelines ensures your charity maintains donors' trust and avoids legal troubles.

Generosity drives the charitable sector, and Canadian charities play a vital role in channelling that spirit to create meaningful impact. By understanding and adhering to the rules for gifting and receipting, your charity can maximise its potential while fostering transparency and trust.

For further clarification, consult CRA resources or seek professional advice to navigate complex cases. With proper practices in place, your charity will be well-positioned to thrive during every giving season and beyond.

Frequently Asked Questions: Donation Receipts for Canadian Charities

Can a Canadian charity issue a receipt for donated services or volunteer time?

No. Volunteer time and donated services do not qualify as gifts under the Income Tax Act and cannot be receipted. Only the transfer of property — such as cash, publicly traded securities, or real property — qualifies as a charitable gift eligible for an official donation receipt.

What happens if a charity issues a receipt with an error?

The charity must cancel the original receipt, keep it on file, and issue a corrected receipt with a new serial number. Receipts cannot be altered after they are issued. Both the cancelled and corrected receipts must be retained in the charity's records.

Is a Canadian charity required to issue a donation receipt?

No. There is no legal obligation for a registered charity to issue donation receipts. However, donors cannot claim a charitable tax credit or deduction without one, so issuing receipts promptly is strongly encouraged as a matter of good donor relations and transparency.

Can donation receipts be issued electronically in Canada?

Yes. The CRA permits electronic donation receipts — including PDF receipts sent by email or generated through a donor portal — without any special approval. However, electronic receipts must contain all the same mandatory information required on a paper receipt.

What is the eligible amount of a gift, and how is it calculated?

The eligible amount is the portion of a donation that qualifies for a tax receipt. It is calculated by taking the fair market value of the donated property and subtracting the fair market value of any advantage received by the donor in return. For example, if a donor gives $500 and receives event tickets worth $75, the eligible amount is $425.

Can a charity issue a receipt for a pledge before the donation is paid?

No. A pledge is not a gift under the Income Tax Act. An official donation receipt can only be issued once the actual donation — whether cash or property — has been received by the charity. The receipt must be dated on or after the date the gift was received.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)