Are Canadian Nonprofits & Charities Allowed to Distribute Profits to Their Members?

Published on

August 12, 2024

Last updated on

July 26, 2026

Canadian nonprofits and charities follow strict rules about managing money. Many people wonder if these organizations can share profits or assets with members.

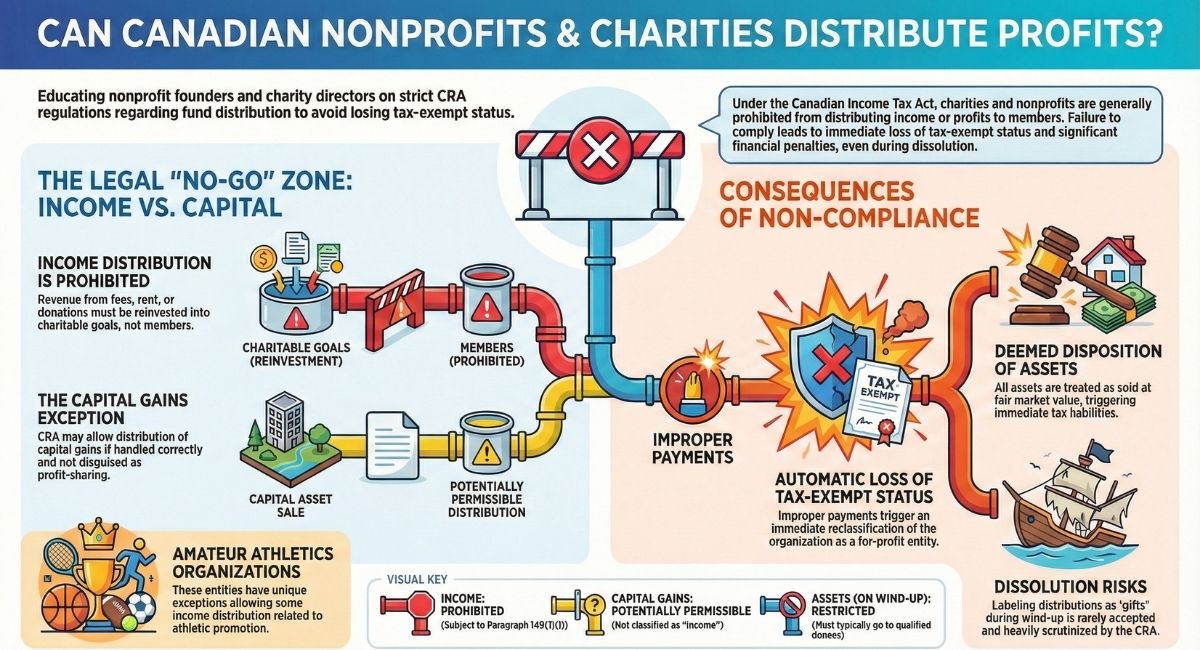

The straightforward answer is no—Canadian charities and most nonprofits cannot distribute profits or income to their members without risking their tax-exempt status.

Charities must use their income to support their charitable purposes. In some cases, such as winding up operations, rules about distributing capital or assets become relevant.

Even during dissolution, these rules are complex. Distributing income to members can cause serious consequences, including loss of tax exemption.

Understanding the difference between income, capital gains, and assets is important for anyone involved with these organizations. We will look at how these rules work and what nonprofits and charities need to consider before distributing any funds to members.

Legal Framework for Distributing Profits in Canadian Nonprofits and Charities

Canada has strict and detailed rules for distributing profits among members of nonprofits and charities. We need to understand legal distinctions, tax rules, and how government agencies enforce these rules to protect tax benefits.

Key Differences Between Nonprofits and Charities

Nonprofits and charities are different types of organizations under Canadian law. Each has specific legal frameworks.

Nonprofits serve their members or the public without aiming to generate profits for distribution. If a nonprofit makes profits, it must reinvest them in the organization’s activities, not pay them out to members.

Charities exist solely to pursue purposes like relief of poverty, education, or religion. They must operate for public benefit and cannot distribute income or assets to members or directors.

All profits must support charitable goals. This rule applies to both income and assets.

Overview of the Income Tax Act and Tax-Exempt Status

The Income Tax Act defines tax-exempt status, which is crucial for charities. Under paragraph 149(1)(l), charitable organizations do not pay income tax if they meet specific requirements.

They cannot distribute income or capital gains to members, shareholders, or anyone personally. Charities may hold or sell investments, but if they distribute proceeds, they can only return capital, not income.

Distributing income profits risks losing tax-exempt status and can trigger tax penalties.

Role of the Canada Revenue Agency in Enforcement

The Canada Revenue Agency (CRA) oversees compliance with nonprofit and charity rules. They monitor if organizations distribute profits improperly or act for personal benefit.

CRA can revoke tax-exempt status if a charity distributes income to members. They also examine distributions disguised as gifts or other payments to members.

CRA evaluates the intent, timing, and nature of distributions. Losing tax-exempt status leads to financial consequences, including paying taxes on asset dispositions.

Rules on Profit Distribution for Nonprofits

We must distinguish profits, income, and capital gains when discussing distributions. Certain organizations have exceptions, but improper distribution can lead to loss of tax-exempt status.

Definition of Income Versus Capital Gains

Under the Income Tax Act, income and capital gains are treated differently for nonprofits. Income usually comes from activities related to the nonprofit’s purpose, such as donations, fees, or rent.

This income cannot be distributed to members without threatening tax-exempt status. Capital gains arise from selling assets like shares or property that have increased in value.

The CRA considers capital gains as part of the organization's capital, not income. Nonprofits may distribute capital gains to members without automatically losing tax-exempt status, if the distribution is not disguised profit sharing or dividends.

Distributing income to members is prohibited. Distributing capital gains must be handled carefully and only under proper legal guidance.

Exceptions for Amateur Athletics Organizations

Nonprofits promoting amateur athletics in Canada have special rules. These organizations can distribute income to their members under certain conditions.

This exception recognizes the unique nature of amateur sports, where participants may receive funds directly related to athletic activities. For example, income from events or sponsorships can sometimes be shared with athletes or teams legally.

This exemption is limited. It applies only if the organization qualifies under paragraph 149(1)(l) of the Income Tax Act and if distributions are reasonable and related to promoting amateur athletics.

Noncompliance can still risk the loss of tax-exempt status.

Consequences of Improper Distributions

If a nonprofit distributes income or profits improperly, the consequences are significant. The Canada Revenue Agency will consider that the organization has lost its tax-exempt status.

The process includes a deemed disposition of all assets at fair market value, which triggers immediate tax implications.

The organization then loses its exemption, and any capital dividend account balance is eliminated. The nonprofit must pay taxes like a for-profit entity.

Members who receive improper distributions could also face tax liabilities. Nonprofits must strictly follow rules on income distribution and seek expert advice when dissolving or reallocating assets.

Charity Law and Distribution of Profits in Canadian Registered Charities

We must follow strict rules when handling profits and assets in Canadian registered charities. These rules protect the charity’s purpose and prevent improper financial benefits to members.

This helps the charity stay compliant with registration and tax-exempt status.

Prohibitions on Income Distribution to Members

Canadian registered charities cannot distribute income to members, shareholders, or directors. Money earned through the charity’s regular activities cannot be paid out as profits or dividends.

The Income Tax Act states that charitable income must be used to further the charity’s purpose. Any distribution of income to members risks the charity losing its tax-exempt status.

This applies even during the winding-up or dissolution of the charity, except in rare cases like organizations supporting amateur athletics. The Canada Revenue Agency (CRA) checks such transfers closely to prevent improper benefits.

Charitable Purposes and Use of Assets

Our assets, including profits, must advance our charitable purposes. Activities should benefit the public, such as relief of poverty, education, or other recognized charitable goals.

When a charity holds investments or capital gains, it cannot use those assets for members’ personal benefit. Distributing capital gains to members carries legal risks unless done correctly.

All assets must support charitable work or be transferred appropriately upon winding up.

Charitable Registration Compliance

We must comply with CRA rules and reporting requirements to maintain charitable registration. Any changes in operations, such as distributing assets or changing activities, must be reported to the Charities Directorate for approval.

Failing to follow rules around income and asset distribution can cause immediate loss of tax-exempt status. This triggers a deemed disposition of assets and other tax consequences.

Consulting legal and tax professionals helps ensure distributions do not jeopardize our registration or mission.

Treatment of Assets and Capital Gains Upon Dissolution

When a Canadian charity or nonprofit dissolves, it must handle assets and capital gains carefully to follow CRA rules. Distributing assets improperly can risk tax-exempt status and lead to tax consequences.

Distributing Assets on Wind-Up

During dissolution, charities must distribute remaining assets according to strict rules. Assets cannot be given to members or shareholders if they represent income.

Usually, assets are transferred to other qualified charities or nonprofits. Capital assets, like investments or property, are handled differently.

The CRA allows distribution of capital, including capital gains, to members only if these gains are not classified as income. The organization must ensure asset distribution does not conflict with its purpose or tax-exempt framework.

Distribution as a Gift or Refund

Some nonprofits or charities may consider calling asset distributions “gifts” or refunds. The CRA examines these payments closely.

If the distribution comes from income or is seen as personal benefit, it risks loss of tax-exempt status. For incorporated charities, members are often treated like shareholders, making any distribution similar to a shareholder benefit.

Even if labelled a gift, the CRA looks at timing, purpose, and context. “Gifts” from income or profits are not an effective way to distribute assets to members.

Tax Consequences of Losing Status

If a charity or nonprofit distributes income or violates CRA rules during dissolution, it loses tax-exempt status immediately. This triggers several consequences:

- The charity is deemed to have sold all assets at fair market value.

- The organization loses its tax-exempt status.

- Any capital dividend account balance is reduced to zero and cannot be paid out.

The organization then faces significant tax costs and loses important tax privileges. We must follow these rules when managing assets on wind-up to avoid penalties.

Asset Distribution During Charity Dissolution

When a charity in Canada decides to dissolve or wind up its operations, a crucial question arises: How should it distribute its assets without jeopardizing its tax-exempt status? The Canada Revenue Agency (CRA) recently issued a ruling that sheds light on this important topic. This article will break down the key points of this ruling, explain the implications for charities, and provide guidance on how to navigate these complex rules.

Understanding the Legal Framework for Charities in Canada

First, it's essential to clarify what type of organization we are discussing. In Canada, a charity is a tax-exempt entity as defined under paragraph 149(1)(l) of the Income Tax Act. Unlike a for-profit organization, a charity must operate exclusively for purposes other than profit. Additionally, no part of the organization's income should be paid out or made available for the personal benefit of any member, proprietor, or shareholder. An exception to this rule exists only for organizations that promote amateur athletics in Canada.

The CRA Ruling: What Prompted the Discussion?

The CRA's ruling was in response to a charity that had acquired shares of a private company at a nominal cost, which then significantly appreciated in value. The charity wanted to distribute these shares or the proceeds from their sale to some of its members before or during its dissolution. The central question was whether such a distribution would cause the charity to lose its tax-exempt status.

Distributing Capital Gains: What Are the Rules?

One critical aspect of the CRA's ruling revolves around the distribution of capital gains. Charities must be cautious when dealing with investments or assets, as using them for purposes unrelated to the organization's objectives can threaten their tax-exempt status. Holding onto investments, like shares, for an extended period might be seen as operating for profit, which is not allowed.

When it comes to distributing the proceeds from the sale of such investments, the CRA clarified an important point: capital gains, whether taxable or non-taxable, do not count as "income" under paragraph 149(1)(l). This distinction is crucial because income cannot be distributed to members without risking the charity's tax-exempt status. Therefore, a charity can distribute its capital or capital gains to members while retaining its tax-exempt status, provided it does not distribute any portion considered income.

Distributing Assets During Wind-Up: What Are the Limitations?

Even during the wind-up process, the rule against distributing income to members remains in effect. The only exception is for members that meet the specific criteria related to promoting amateur athletics in Canada. For all other members, the charity cannot distribute any income, regardless of their tax-exempt status or whether they are qualified donees.

This rule also applies to the distribution of assets during wind-up. If distributing these assets would result in any portion of the income being shared with members, the charity could lose its tax-exempt status.

Consequences of Losing Tax-Exempt Status

Losing tax-exempt status has significant consequences for a charity. According to the CRA, if a charity undertakes an action that disqualifies it from its tax-exempt status, a series of events is triggered immediately:

- Deemed Disposition of Assets: The charity is deemed to have sold all its assets and reacquired them at fair market value while still tax-exempt.

- Loss of Tax-Exempt Status: The charity then loses its tax-exempt status.

- Reduction of Capital Dividend Account: Finally, any amount added to the capital dividend account due to the deemed disposition is reduced to zero, meaning it cannot be paid out to members.

Can Distributions Be Characterized as Gifts?

Some charities might consider characterizing distributions to members as "gifts" to circumvent the rules. However, the CRA's ruling clarifies that this approach is rarely viable. The CRA will closely scrutinize the circumstances surrounding the distribution, including the type of charity, the nature of the payment, its timing, and its purpose.

For incorporated charities, the CRA is likely to view such payments as shareholder benefits, given that members of non-share capital corporations are treated as shareholders for this purpose. If the charity is unincorporated, the nature of the payout will depend on its context. For example, during a wind-up, a payout could be considered compensation for the member's rights, resulting in a capital gain for the member.

However, even if the distribution is genuinely a gift, if it forms part of the charity's income, distributing it to members will still cause the organization to lose its tax-exempt status.

Navigating the rules around asset distribution and maintaining tax-exempt status can be complex for Canadian charities. The CRA's ruling offers valuable guidance but also highlights the risks involved if a charity is considering any payout to members, whether before or during a wind-up, it is essential to keep the statutory definition of a tax-exempt charity in mind and seek expert advice to ensure compliance with the law.

By understanding and following these rules, charities can avoid the significant tax consequences that come with losing their tax-exempt status, ensuring they continue to serve their communities effectively. This detailed guide is designed to help Canadian charities navigate the complex regulations surrounding asset distribution and tax-exempt status. It emphasizes the importance of careful planning and consultation with legal and tax professionals to ensure compliance with the law.

Fundraising and Revenue Generation: Maintaining Compliance

We must balance raising revenue with strict rules to protect our nonprofit or charity’s tax-exempt status. How we raise and report funds affects our credibility and legal standing with the CRA.

Fundraising and Revenue Rules for Nonprofits

Our fundraising activities must align with our charitable purposes. Fundraising supports our work but is not a charitable activity itself.

We can generate revenue, but it must further our core charitable goals. If activities become profit-focused or unrelated to our mission, the CRA may question our tax-exempt status.

We cannot distribute profits to members, shareholders, or insiders. Surplus funds must be reinvested into charitable programs.

Registered charities face additional limits. They must not hold investments just to make gains and must use assets to support their mission.

We must also follow CRA rules on what counts as income and how capital gains are treated.

Reporting, Transparency, and Accountability

Accurate records and clear reporting are critical for public trust and compliance. The CRA requires detailed disclosure of fundraising costs, revenues, and spending.

We must file annual returns and financial reports that show the link between income and charitable activities. Transparency helps donors see how their donations support programs versus fundraising expenses.

Accountability means keeping good records of all donations and using official donation receipts when needed. We must never distribute income or assets to members if that risks our tax-exempt status.

By meeting these reporting standards, we safeguard our status and show responsible stewardship of public and donor funds.

Recent Legal Developments and Best Practices

We need to follow recent regulatory updates and adopt clear policies to protect our organizations. This includes adapting to new rules, strengthening governance, and seeking expert advice for complex issues about asset distribution and tax-exempt status.

Law Changes and Their Impact

The Canada Revenue Agency (CRA) recently clarified rules on asset distribution for charities. Charities cannot distribute income to members without risking their tax-exempt status.

Capital gains and capital assets can be distributed under certain conditions without losing this status. The key is separating income from capital.

The CRA’s rulings emphasize that gifts or distributions to members from the charity’s income can cause penalties. Charities must carefully manage investments and distributions, especially during wind-up or dissolution.

Legislation changes in 2025 introduce stricter filing and reporting requirements. These require more detailed documentation on financial activities and adherence to federal rules for not-for-profits and charities.

Best Practices for Board Governance

Our boards must enforce strong policies for asset management and conflict of interest. Clear rules about member benefits must be written and followed.

Boards should regularly review these policies for compliance with CRA guidelines. We should document all asset distribution decisions thoroughly.

Transparency helps prevent risks of losing charitable status. Training board members on legal responsibilities and updates is important for sound governance.

It is also best to separate capital funds from income funds in records. This accounting practice prevents distributions of capital from being mistaken for income and avoids regulatory issues.

Consulting Experts for Complex Situations

When you handle asset distribution or profit-sharing, consult charity law experts. CRA rules are detailed and complex.

If you don’t follow these rules, your organization could face severe consequences. Engage lawyers or accountants who specialize in charity law before making major financial decisions.

This is especially important during wind-up or when managing investments. Expert advice helps you understand CRA rulings and provincial laws.

Professional guidance also helps you plan strategically to keep your tax-exempt status. Stay informed about legal updates and prepare for new tax filing requirements coming in 2026.

Conclusion

If your nonprofit or charity wants to distribute profits or assets to members, you must understand the strict rules. Income usually cannot be shared with members without risking your tax-exempt status.

Exceptions are rare, especially for charities focused on amateur athletics. Contact B.I.G. Charity Law Group for guidance tailored to your situation.

Whether you are winding up or managing ongoing operations, we help you navigate regulations to protect your tax status and mission. Reach us at dov.goldberg@charitylawgroup.ca or call 416-488-5888.

Schedule a FREE consultation with us at CharityLawGroup.ca to discuss your needs and ensure compliance under Canadian law.

We support your charitable work with clear, reliable advice.

Frequently Asked Questions

We clarify key details about how Canadian charities and nonprofits operate financially. This includes their ability to earn profit, differences between them, board member compensation, financial transparency, and rules around sharing profits.

Can charities make a profit in Canada?

Yes, charities in Canada can generate profit. The profit must support their charitable activities and cannot go to members or stakeholders.

What is the difference between a nonprofit and a charity in Canada?

A charity is a registered organization focused on specific charitable purposes and enjoys tax-exempt status. A nonprofit may operate for social or community goals but does not always have tax-exempt status.

Can nonprofit board members be paid in Canada?

Board members of nonprofits can be paid, but compensation must be reasonable and follow the organization's rules. Excessive payment may put the nonprofit’s standing at risk.

Do nonprofits have to disclose financials to the public in Canada?

Registered charities must file annual financial returns with the Canada Revenue Agency (CRA), and these are publicly accessible. Some nonprofits also disclose financials voluntarily or if required by law.

What constraints are placed on profit sharing among stakeholders in Canadian nonprofit entities?

Nonprofits and charities cannot share profits or income with members, directors, or officers. They must reinvest any profits in advancing the organization’s mission.

How does the Canada Revenue Agency regulate profit disbursement within charitable institutions?

The CRA does not allow charities to distribute income to members, except in rare cases like promoting amateur athletics.

If a charity distributes profits as income, it can lose its tax-exempt status.

Charities may distribute capital gains if these do not count as income.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)