How to Start a Private Foundation in Toronto, Ontario

Published on

September 11, 2024

Last updated on

February 10, 2026

Foundations, whether private or public, play a significant role in supporting charitable causes across Canada. If you’re considering starting a foundation in Toronto, Ontario, or anywhere else in Canada, understanding the process, responsibilities, and differences between private and public foundations is crucial.

The CRA has updated its disbursement quota rules for private foundations, making it more important than ever to understand your compliance obligations before you begin.

This guide will walk you through the key steps and considerations, as well as highlight the benefits of establishing either type of foundation.

What Is a Private and Public Foundation in Canada?

In Canada, both private and public foundations are registered charities that provide financial support to other charitable organizations. The main difference between the two lies in their funding sources and operational models:

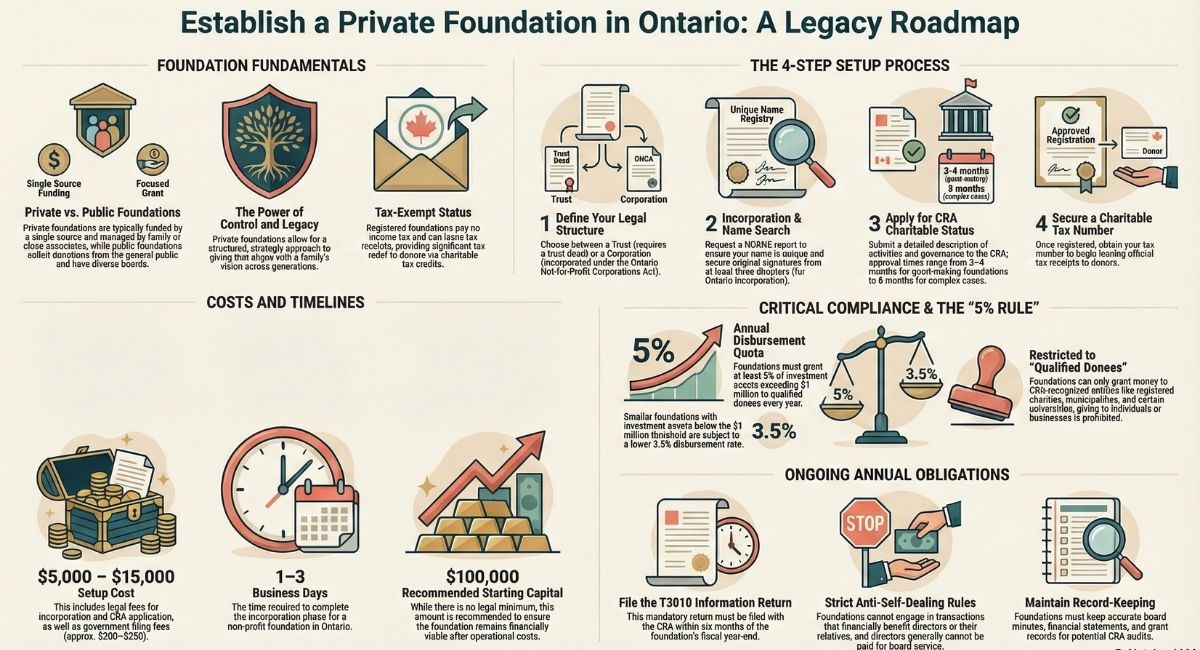

- Private Foundation: Typically funded by a single individual, family, or corporation. It is managed by a small group of trustees or directors, often family members, who control the distribution of funds. Private foundations usually do not engage in active fundraising or solicit donations from the public.

- Public Foundation: Funded by a broader group of individuals, corporations, and other foundations. Public foundations actively raise funds and often have a more diverse board of directors. They are more involved in public fundraising campaigns and may support a wider range of charitable initiatives.

Both types of foundations are tax-exempt when registered with the Canada Revenue Agency (CRA) and focus on supporting charitable causes either through grants or by conducting their own charitable activities.

How to Set Up a Public or Private Foundation in Canada?

Setting up a foundation in Canada lets you support causes you care about while getting tax benefits. The setup process is similar for both public and private foundations, but key differences affect your choice. Private foundations use your own money and give you more control. Public foundations collect donations from many sources and follow different rules.

Whether you’re setting up a private or public foundation, the process is similar, though certain elements will vary depending on the foundation type.

Determine the Legal Structure: Trust or Corporation

Foundations in Canada can be established either as a trust or a corporation. If setting up a trust, you will need to create a trust deed. If establishing a corporation, you will need to incorporate the foundation under provincial, territorial, or federal law. In Ontario, you would register your foundation under the Ontario Not-for-Profit Corporations Act (ONCA).

Incorporation and Name Selection

Choosing a unique name is an important step in the process. If the name includes a person’s name, written consent from the individual or family may be required. To ensure that your chosen name is unique, you can request a NUANS (Newly Upgraded Automated Name Search) report, which checks for similar business names across Canada.

Apply for Charitable Status with the CRA

After incorporation, the next step is applying for charitable status with the CRA. This is a crucial step because it allows your foundation to be tax-exempt and issue tax receipts to donors. The application process involves submitting detailed documentation, including a description of the foundation's activities, governance structure, and charitable purposes.

The CRA will determine whether your foundation qualifies as a private foundation, public foundation, or charitable organization based on factors such as funding sources, the relationship between directors or trustees, and the foundation's operational goals. Public foundations must demonstrate a broader funding base and typically have more external directors than private foundations.

Board of Directors for Foundation

Both private and public foundations require a board of directors. In Ontario, at least three directors are required to incorporate a foundation under ONCA. Each director must provide an original signature on the incorporation documents. Directors must be at least 18 years of age and cannot be undischarged bankrupts at the time of appointment.

Public foundations typically have a larger and more diverse board compared to private foundations, which are often family-run. Federally incorporated private foundations can suffice with just one director.

Apply for a Charitable Tax Number

Once your foundation is registered as a charity with the CRA, it can apply for a charitable tax number. This allows the foundation to issue tax receipts to donors, which can be a major incentive for contributions.

Disbursement Quota Rules for Private Foundations in Canada

One of the most important — and recently updated — compliance requirements for private foundations in Canada is the disbursement quota (DQ). As of 2023, the federal government increased the disbursement quota for registered charities and private foundations, and these rules remain in effect for 2025 and beyond.

Here is what you need to know:

- Private foundations must disburse at least 5% of their investment assets annually for assets exceeding $1 million (based on the prior fiscal year-end value).

- Assets under $1 million remain subject to a 3.5% disbursement rate.

- These funds must be distributed to qualified donees — registered charities, municipalities, certain universities, and other organizations recognized by the CRA.

- The CRA can grant relief from the disbursement quota in certain circumstances, such as when a foundation is saving funds for a large capital project.

- Failure to meet the annual disbursement quota can result in a penalty tax under the Income Tax Act.

If you are planning to set up a private foundation in Toronto or anywhere in Ontario, your legal and accounting team should build a disbursement plan into your foundation's governance structure from day one.

What Can a Private Foundation in Canada Grant To?

A common question from founders setting up a private foundation in Toronto and across Ontario is: who or what can we actually give money to?

In Canada, private foundations are generally restricted to making grants to qualified donees only. This is an important legal constraint that many new founders are not aware of.

Qualified donees include:

- Registered charities (the most common recipient)

- Canadian municipalities

- The federal and provincial governments of Canada

- Certain foreign charitable organizations to which the Government of Canada has made a gift

- Registered Canadian amateur athletic associations

- Registered journalism organizations

- Certain universities outside Canada listed in Schedule VIII of the Income Tax Regulations

Private foundations cannot simply grant money to individuals, unregistered organizations, or businesses — even if those recipients are doing valuable charitable work. If a foundation makes a grant to an organization that is not a qualified donee, it risks losing its charitable registration.

There is also a concept known as a "direction" grant, where a foundation attempts to direct a registered charity on how to use donated funds. This must be handled carefully to ensure the receiving charity retains full control over the use of the funds, or the foundation could face compliance issues with the CRA.

How Much Does It Cost to Start a Private or Public Foundation?

Starting a foundation in Canada involves some legal and administrative costs. If you choose to work with a lawyer experienced in charity law, expect fees to range from $7,000 to $15,000 for comprehensive assistance throughout the setup process. The figures below reflect 2025 estimates — government filing fees are subject to change, and you should confirm current rates with your lawyer or the applicable government registry.

- Incorporating a Foundation: Incorporation fees for a non-profit foundation (whether private or public) typically range between $2,000 and $3,000 in legal fees. Additionally, you will need to pay government filing fees, which can range between $200–$250, depending on which provincial or federal jurisdiction the foundation is incorporating in. A typical foundation can be incorporated in as little as 1–3 business days.

- Application for Charitable and Foundation Status: Applying for charitable and foundation registration with the CRA can take 6–8 months, depending on the complexity of the foundation's operations and the CRA's review process. However, most family and private foundations that are exclusively donating to other registered charities are approved within 3–4 months, on average.

What Are the Benefits of Starting a Foundation in Canada?

Both private and public foundations offer several advantages:

- Tax Benefits: Registered foundations are exempt from paying income tax in Canada. They can also issue tax receipts to donors, which provides significant tax relief through charitable tax credits.

- Philanthropic Legacy: Foundations, particularly private ones, offer families an opportunity to build a lasting legacy. They allow individuals or families to maintain control over how funds are distributed, ensuring that donations align with their philanthropic vision for generations to come.

- Control and Flexibility: Private foundations, in particular, offer control over decision-making and grant distribution. Public foundations, while more reliant on external donations, also benefit from having a wider reach and broader community support.

- Structured Giving: Foundations provide a structured and strategic approach to charitable giving. Whether through grants, scholarships, or direct donations to charities, foundations allow for more organized philanthropic efforts that align with long-term goals.

Ongoing Compliance: What Private Foundations Must Do Each Year

Setting up a private foundation is just the beginning. Once registered, your foundation has ongoing legal and regulatory obligations it must meet every year to maintain its charitable status with the CRA. Many founders in Toronto and across Ontario are not fully aware of these requirements until they are already registered.

Here is what your private foundation must do on an annual basis:

1. File the T3010 Annual Information Return

Every registered charity, including private foundations, must file the T3010 Annual Information Return with the CRA within six months of the end of its fiscal year. This return discloses the foundation's revenues, disbursements, grants made, and director information. Failure to file on time can result in the revocation of charitable status.

2. Meet the Annual Disbursement Quota

As outlined above, private foundations must disburse at least 5% of investment assets over $1 million each year. Your accountant and legal team should review your disbursement obligations annually to ensure compliance.

3. Avoid Self-Dealing Transactions

Private foundations are subject to strict self-dealing rules under the Income Tax Act. This means the foundation cannot make grants or business transactions that benefit directors, officers, or their related persons. For example, a private foundation cannot grant funds to a business owned by one of its directors, even if that business does charitable work.

4. Maintain Proper Records and Minutes

Your foundation must keep accurate records of board meeting minutes, resolutions, grant decisions, and financial statements. The CRA may request these during an audit or compliance review.

5. Notify the CRA of Material Changes

If your foundation changes its address, adds or removes directors, amends its governing documents, or significantly changes its activities, you must notify the CRA in a timely manner. Failing to keep the CRA updated can create compliance issues during your annual filing or at the time of an audit.

Staying on top of these obligations is much easier when you have experienced charity lawyers and accountants supporting your foundation from day one.

Is Starting a Private or Public Foundation Right for You?

Setting up a private or public foundation in Toronto can be a rewarding way to support charitable causes and leave a lasting philanthropic legacy. Both private and public foundations offer significant tax benefits, control over charitable giving, and the opportunity to make a lasting impact on communities and causes that matter most to you.

Before starting the process, it’s important to consult with experienced charity and not-for-profit lawyers to ensure that your foundation complies with all regulatory requirements and aligns with your charitable goals. Whether you're setting up a private family foundation or a public foundation that reaches out to the wider community, the steps outlined above can help guide you through the process. Set up a free call with our team at 416-488-5888 or schedule a call here.

Frequently Asked Questions

Get quick answers to common questions about setting up foundations in Canada.

What is the minimum amount to start a private foundation?

There's no legal minimum amount required to start a private foundation in Canada. However, you should have enough funds to cover setup costs (typically $5,000-$15,000) plus ongoing operational expenses. Most experts recommend starting with at least $100,000 to make the foundation financially viable long-term.

How much does it cost to start a foundation in Canada?

Starting a foundation typically costs between $5,000 and $15,000. This includes legal fees for incorporation ($2,000-$8,000), application fees to Canada Revenue Agency, accounting setup, and initial administrative costs. Annual operating costs range from $3,000-$10,000 depending on the foundation's size and activities.

What is the difference between a foundation and a private foundation?

A foundation is a general term for charitable organizations that distribute grants. A private foundation is a specific type funded primarily by one source (individual, family, or corporation) with more control over grant-making. Public foundations receive donations from multiple sources and have broader public involvement in their governance.

What is the alternative to a private foundation?

Main alternatives include donor-advised funds (simpler and cheaper to set up), charitable remainder trusts, direct giving to existing charities, or establishing a fund within a community foundation. Donor-advised funds offer similar tax benefits with less administrative burden and lower minimums.

What is the structure of a private foundation?

A private foundation operates as a non-profit corporation with a board of directors (minimum 3 members). The structure includes founding documents, bylaws, and policies for grant-making. The board oversees operations, approves grants, and ensures compliance with charitable regulations and annual disbursement requirements.

Can a private foundation in Canada pay its directors?

Generally, directors of private foundations cannot receive remuneration for their services as directors. Paying directors for board service can constitute a self-dealing transaction and put the foundation's charitable status at risk. In some cases, a director who is also employed by the foundation in a staff capacity may receive a salary for their employment role, but this requires careful legal review to ensure compliance with the Income Tax Act.

How long does it take to register a private foundation in Canada?

Incorporation typically takes 1–3 business days. CRA registration for charitable and foundation status generally takes 6–8 months, though private foundations that exclusively make grants to registered charities are often approved within 3–4 months.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)