How to Avoid Common Mistakes When Filing T3010 Return

Published on

April 2, 2024

Last updated on

July 8, 2026

We know how stressful it gets when our charity's T3010 return gets delayed or rejected because of simple mistakes we could have avoided.

We can prevent most T3010 filing errors by using the correct form version, including complete financial statements with matching fiscal year-ends, and ensuring all required signatures and attachments are in place. Common mistakes include filing incomplete returns, missing financial statements, and incorrect calculations that cause processing delays.

In this guide, we'll walk through the most frequent T3010 mistakes we see Canadian charities make and show you exactly how to avoid them.

Understanding the T3010 Return and Its Importance

The T3010 Registered Charity Information Return serves as our charity's annual accountability report to the Canada Revenue Agency. Understanding this form and its requirements helps us avoid costly mistakes and maintain our charitable status.

Filing errors or delays can result in significant penalties and jeopardize our organization's future.

What is the T3010 Registered Charity Information Return?

The T3010 is a comprehensive annual form that documents how we used our charitable funds and conducted our activities during the fiscal year. Every registered charity in Canada must complete this return, regardless of our organization's size or activity level.

The return includes detailed financial information about our revenue, expenses, assets, and liabilities. We must attach audited financial statements and complete specific schedules based on our charity's circumstances.

The form requires us to report on:

- Charitable programs and activities we conducted

- Fundraising costs and administrative expenses

- Directors and trustees information and compensation

- Transactions with non-arm's length parties

- Property holdings not used for charitable activities

We use the same T3010 form whether our charity raised $1,000 or $10 million during the fiscal year. However, larger charities face additional reporting requirements through Schedule 6.

Why Charities Must File the T3010

Filing our T3010 maintains our legal standing as a registered charity and preserves our tax-exempt status. The CRA uses this information to monitor our compliance with charitable regulations and ensure we're operating within our stated purposes.

We must file the T3010 to keep our charitable registration active and maintain our ability to issue official donation receipts. This annual filing demonstrates that we're using donations for legitimate charitable purposes and meeting our spending requirements.

The CRA monitors our compliance through several key requirements:

- Disbursement quota: Spend at least 3.5% of total assets on charitable activities

- Charitable purposes: Operate within our registered purposes and objects

- Fund accumulation: Follow rules for holding funds beyond one year

- Political activities: Stay within permitted limits for political activities

Our filing also shows transparency to donors and the public. The CRA publishes summary information from our T3010 on their website, allowing donors to research our organization before contributing.

Consequences of Filing Errors or Late Submission

Filing mistakes or missing deadlines can trigger serious consequences that threaten our charity's operations and reputation. The CRA imposes automatic penalties and may take enforcement action against non-compliant organizations.

Late filing results in penalties of $500 per month until we submit our return. The CRA can revoke our charitable status if we fail to file for one full year, permanently ending our tax-exempt status and receipting privileges.

Common consequences of filing errors include:

- Compliance letters: Requests for explanations or corrections

- Audit requests: Detailed reviews of our operations and finances

- Processing delays: Hold-ups that affect our annual filing schedule

- Penalty assessments: Financial costs for late or incorrect submissions

- Increased scrutiny: Enhanced monitoring of future returns

Repeated filing problems can result in increased scrutiny of future returns and potential restrictions on our operations. In severe cases, the CRA may suspend our receipting privileges or impose other sanctions before considering revocation.

Key Filing Requirements and Common Mistakes

Understanding the specific requirements and deadlines for T3010 filing helps us avoid the most frequent errors that charities make. Many of these mistakes stem from misunderstanding basic filing rules or overlooking critical documentation requirements.

Proper preparation and attention to detail can prevent most compliance issues and processing delays.

Critical T3010 Filing Deadlines

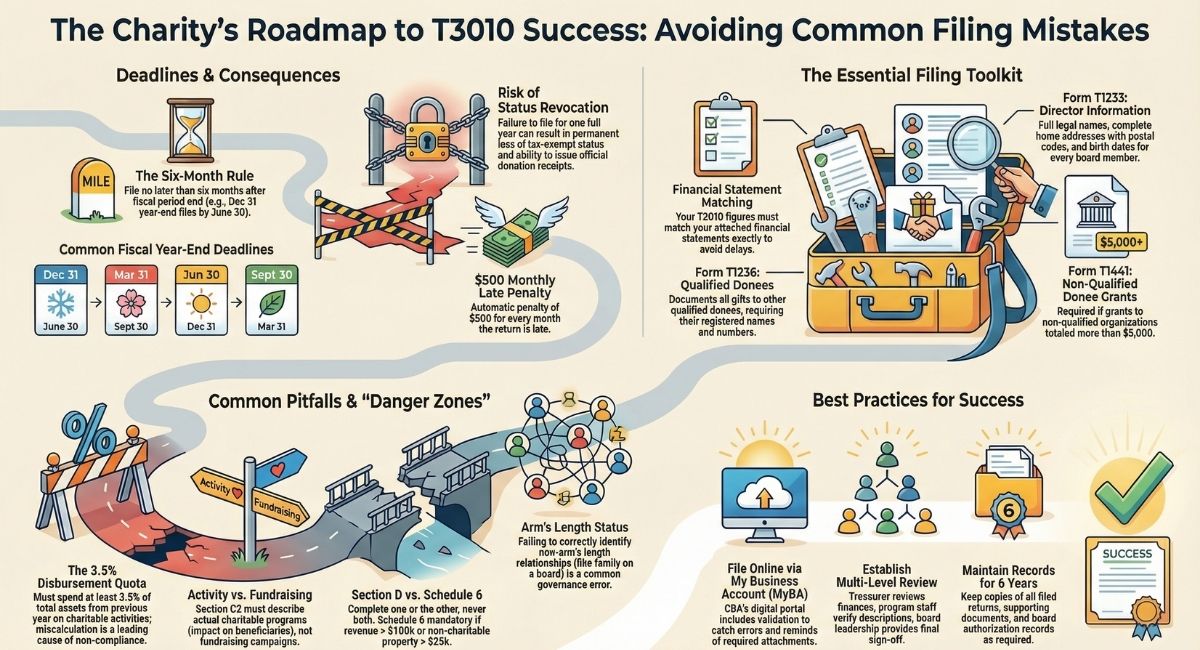

We must file our complete T3010 return no later than six months after the end of our fiscal period. Missing this deadline triggers automatic penalties and puts our charitable status at risk.

The filing deadline depends entirely on our charity's fiscal year-end date. For example, charities with a December 31 fiscal year-end must file by June 30, while those with a March 31 year-end must file by September 30.

Key filing deadlines include:

- January 31 year-end: File by July 31

- March 31 year-end: File by September 30

- June 30 year-end: File by December 31

- September 30 year-end: File by March 31

- December 31 year-end: File by June 30

Charities with fiscal years ending on or after December 31, 2023 must use T3010 version 24, which includes updated disbursement quota requirements and new reporting sections.

We cannot request extensions for T3010 filing deadlines. The CRA may revoke our charitable status for failure to file, which means we can no longer issue official donation receipts or remain tax-exempt.

Major Oversights That Lead to Non-Compliance

Many charities lose their registration due to preventable oversights that seem minor but have serious legal consequences. These compliance failures often result from misunderstanding basic charity law requirements or poor internal processes.

The most serious oversight is failing to meet the disbursement quota. We must spend at least 3.5% of our total assets from the previous year on charitable activities. Many charities miscalculate this requirement or fail to track their spending properly.

Common major oversights include:

- Using wrong T3010 version: Filing with outdated forms that don't reflect current requirements

- Missing financial statement attachments: Submitting returns without required audited statements

- Incorrect disbursement quota calculations: Misunderstanding what counts toward the 3.5% requirement

- Unreported related party transactions: Failing to disclose payments to directors or connected organizations

- Incomplete signatures: Missing required director or trustee signatures in Section E

Operating outside our charitable purposes represents another critical oversight. We must ensure all our activities align with the objects stated in our governing documents and CRA registration.

Accumulating funds without permission also creates compliance problems. We can only hold funds beyond one year if we receive specific CRA approval or meet certain exemption criteria.

Mistakes with Incomplete or Missing Information

Incomplete T3010 returns cause processing delays and often trigger CRA compliance reviews. These information gaps force us to file amended returns and may result in penalties or increased scrutiny.

Missing director and trustee information represents one of the most common filing errors. We must provide complete details for all board members, including full names, addresses, dates of birth, and arm's length status.

Critical information that charities frequently omit includes:

- Form T1235: Complete director, trustee, and official information with postal codes and birth dates

- Form T1236: Registration numbers for all qualified donees that received our gifts

- Detailed program descriptions: Specific explanations of charitable activities (not fundraising) in Section C2

- Financial statement reconciliation: Ensuring our T3010 figures match attached audited statements

- Property reporting: Details about assets not used directly in charitable activities

Incorrect financial calculations create serious problems when our T3010 totals don't balance. Lines 4500 to 4650 must equal line 4700 in Section D, and lines 4860 to 4920 must equal line 4950.

We must choose between completing Section D or Schedule 6 based on our charity's size and circumstances. Using both sections or selecting the wrong one creates filing errors that require amendments.

Preparing Your Financial Statements and Supporting Documents

Accurate financial statements form the foundation of our T3010 filing and demonstrate our accountability to donors and regulators. Many T3010 rejections stem from incomplete, inconsistent, or improperly prepared financial documentation.

Proper preparation of financial statements and attachments prevents processing delays and compliance issues with the CRA.

How to Prepare Audited and Unaudited Financial Statements

We must include complete financial statements with every T3010 filing, regardless of our charity's size or revenue level. The CRA recommends professional audits for charities with income over $250,000, while smaller organizations can have their treasurer sign unaudited statements.

Financial statements should include at least a statement of assets and liabilities (balance sheet) and a statement of revenue and expenditures (income statement), along with any prepared notes about accounting policies, investment details, revenue sources, and transactions with non-arm's length parties.

Our financial statements must include these essential components:

- Statement of assets and liabilities (balance sheet) showing our financial position

- Statement of revenue and expenditures (income statement) detailing our fiscal year activity

- Notes to financial statements explaining accounting policies and significant transactions

- Details of investments including maturity dates and interest rates

- Sources of revenue such as government grants or donation categories

- Non-arm's length transactions with related parties or organizations

We must choose either the cash basis method or the accrual basis method for financial reporting and use that same method consistently throughout our entire T3010 return. However, we must always use the cash method to report gifts we received, regardless of our chosen accounting method.

Professional audited statements provide additional credibility and may be required by funders or provincial regulations. Audited statements must follow Canadian accounting standards and include the auditor's opinion letter.

Avoiding Errors in Statement of Financial Position and Operations

Financial statement errors create cascading problems throughout our T3010 filing when numbers don't reconcile between our statements and the return. These discrepancies trigger CRA inquiries and often require amended filings.

The most critical requirement is ensuring our T3010 financial figures match our attached financial statements exactly. Any variance between these documents will cause processing delays and compliance questions.

Common financial statement errors include:

- Misclassification of expenses between charitable programs, fundraising, and administration

- Incorrect asset valuation for investments, property, or equipment

- Missing restricted fund reporting for donor-designated or endowment funds

- Incomplete related party disclosures for transactions with directors or connected organizations

- Wrong fiscal period dates that don't match our T3010 filing period

- Inconsistent accounting methods mixing cash and accrual reporting within the same statement

Revenue classification errors frequently occur when we incorrectly categorize government grants

, donations, or program fees. We must properly distinguish between charitable donations, government funding, and earned revenue from programs or services.

Our statement of operations must clearly show the true cost of our charitable programs versus fundraising and administrative expenses. The CRA uses this breakdown to assess our operational efficiency and compliance with spending requirements.

Asset reporting mistakes often involve failing to properly classify restricted assets, investments held for charitable purposes, or property not used in our charitable activities.

Providing the Right Attachments with Your T3010

Missing or incorrect attachments represent one of the most frequent causes of T3010 processing delays. We must include all required supporting documents with specific information that matches our return data.

Form T1235 provides complete information about our directors, trustees, and like officials. This form requires full names, complete addresses including postal codes, dates of birth, and arm's length status for every board member.

Essential T3010 attachments include:

- Complete financial statements with all required components and notes

- Form T1235: Director, trustee, and official information with all required details

- Form T1236: Registration numbers for all qualified donees that received our gifts

- Auditor's report if we're filing audited financial statements

- Detailed program descriptions explaining our charitable activities and their impact

- Related party transaction details for any non-arm's length dealings

Form T1236 documents all gifts we made to qualified donees during our fiscal year. We must provide the complete registered name and registration number for each recipient organization, along with the exact amount of our gift.

Missing signatures in Section E frequently cause return rejections. We must have a director, trustee, or like official sign and date this section to certify the accuracy of our filing.

Provincial registration certificates may be required in some jurisdictions where we operate, especially if we conduct fundraising activities or operate across provincial boundaries.

Completing Major Sections and Schedules of the T3010

The T3010 form contains several critical sections that require careful attention to detail and proper understanding of when to use each section. Mistakes in these major sections often trigger CRA compliance reviews and processing delays.

Version 24 of the T3010 makes updates to disbursement quota requirements with an entirely new schedule, asks foundations additional questions, and makes adjustments to Schedule 6 for detailed financial information.

Navigating Section D and Schedule 6 Accurately

We must choose between completing Section D or Schedule 6 for our financial reporting, but never both. This decision depends on our charity's size, revenue, and specific circumstances outlined in the CRA guidelines.

We cannot fill out both Section D and Schedule 6, or parts of both. Making the wrong choice creates filing errors that require amended returns and often triggers compliance inquiries.

We must complete Schedule 6 instead of Section D if any of the following apply to our charity:

- Gross revenue exceeds $100,000 during the fiscal year

- Property not used in charitable activities exceeds $25,000 in value

- Permission to accumulate funds has been granted by the CRA for the fiscal year

- Complex financial structure requires detailed reporting beyond Section D capabilities

Section D serves smaller charities with straightforward operations and limited assets. If we use Section D, lines 4500 to 4650 (excluding line 4505) must equal line 4700, and lines 4860 to 4920 must equal line 4950.

Schedule 6 provides detailed financial information for larger charities and those with complex operations. When completing Schedule 6, lines 4500, 4510 to 4580, and 4600 to 4650 must equal line 4700, while lines 4800 to 4920 must equal line 4950.

We can only enter amounts on lines 5500 and 5510 in Schedule 6 if we have received specific permission to accumulate funds. Lines 5900 and 5910 are for reporting property that we own but don't use for charitable activities.

Common Section D and Schedule 6 errors include using the wrong form for our charity's circumstances, failing to balance required line totals, and incorrectly reporting accumulated funds without proper authorization.

Reporting Charitable Activities and Programs Clearly

Section C2 requires us to describe our charitable activities, not our fundraising efforts. This distinction causes frequent filing errors when charities focus on how they raise money rather than what they accomplish with those funds.

We must provide specific, detailed descriptions of our actual charitable programs and their impact on beneficiaries. Generic statements like "helping people" or "community support" don't meet CRA requirements for program reporting.

Our charitable activity descriptions should include:

- Specific programs we delivered during the fiscal year

- Target beneficiaries who received our services or support

- Geographic areas where we conducted our charitable work

- Measurable outcomes and impact on the communities we serve

- Partner organizations we worked with to deliver programs

- Resources committed to each major charitable activity

Avoid fundraising descriptions in Section C2. We shouldn't describe our charity drives, events, or donation campaigns as charitable activities. These are fundraising methods, not charitable programs.

Program impact reporting helps demonstrate our effectiveness and accountability. We should explain how our charitable activities address specific community needs and create positive change for our beneficiaries.

Multi-program charities need to describe each significant charitable activity separately. We can't lump all our programs together under one generic description.

Inactive periods still require reporting. If we didn't conduct charitable activities during a fiscal year, we must explain why and what steps we're taking to resume operations.

Mistakes When Reporting Fundraising Activities

Fundraising cost reporting frequently contains errors that can trigger CRA audits and compliance questions. We must accurately distinguish between fundraising expenses, charitable program costs, and administrative expenses throughout our T3010 filing.

Misclassifying fundraising costs as charitable expenses inflates our reported charitable spending and can make us appear to meet disbursement quota requirements when we actually don't. This creates serious compliance issues.

Common fundraising reporting mistakes include:

- Classifying event expenses incorrectly when events combine fundraising with charitable activities

- Allocating staff time improperly between fundraising, programs, and administration

- Reporting fundraising revenue without corresponding expense allocation

- Missing gift-in-kind valuations for donated goods or services used in fundraising

- Incorrect professional fundraiser reporting and commission structures

- Omitting fundraising licenses required in various provinces

Professional fundraiser relationships require detailed reporting including their names, addresses, and amounts paid for services. We must report both commissions and flat-fee arrangements with external fundraising organizations.

Special event reporting creates particular challenges when events serve both fundraising and charitable purposes. We need to carefully allocate costs and revenues between these different functions.

Direct mail and online fundraising costs must include all associated expenses such as printing, postage, payment processing fees, and staff time devoted to campaign development and management.

Gift processing costs should be allocated to fundraising rather than charitable activities, including receipt preparation, donor database management, and acknowledgment communications.

Correctly Disclosing Directors, Trustees, and Donations

Accurate reporting of our governance structure and charitable giving requires careful attention to specific forms and detailed information requirements. Missing or incorrect information about directors, trustees, and donations frequently triggers CRA compliance reviews and processing delays.

The T3010 includes mandatory reporting schedules that must be completed with precise details about our board members and all charitable gifts we made during the fiscal year.

Filling Out Form T1235 and Arm's Length Status

Form T1235 identifies our board of directors, trustees, and like officials and must be submitted with every annual T3010 return. This form requires complete information for every person who served on our board during any part of the fiscal year.

We must provide comprehensive details for each board member including full legal names, complete home addresses with postal codes, dates of birth, and their arm's length status with respect to our charity.

Form T1235 requires us to report:

- Full legal names of all directors, trustees, and like officials

- Complete home addresses including street address, city, province, and postal code

- Dates of birth for each board member (month, day, and year)

- Arm's length status indicating their relationship to the charity

- Positions held such as president, secretary, treasurer, or director

- Compensation received including salaries, fees, or other payments

Arm's length status determines whether board members have special relationships with our charity that could create conflicts of interest. Non-arm's length relationships include family members of other directors, major donors, or individuals with significant business relationships with our organization.

Common Form T1235 errors include missing postal codes, incomplete addresses, wrong birth dates, and incorrect arm's length designations. We must update this form whenever board membership changes during our fiscal year.

Privacy considerations require us to obtain consent from board members before including their personal information on Form T1235, since this information becomes part of our public filing with the CRA.

Compensation reporting must include all payments made to directors, including meeting fees, travel reimbursements, and any other financial benefits they received from our charity during the fiscal year.

Completing Form T1236 for Qualified Donees

Form T1236 identifies all gifts we made to qualified donees and other organizations during our fiscal year and must be submitted along with our annual T3010 return. This form requires specific information about each recipient organization and the exact amounts we provided.

We must complete Form T1236 for every gift made to qualified donees, regardless of the amount. Missing this form or providing incomplete information can delay processing and trigger compliance questions.

Form T1236 requires us to provide:

- Complete registered names of all qualified donee recipients

- Registration numbers for each qualified donee organization

- Exact gift amounts provided during our fiscal year

- Types of gifts such as cash, property, or other assets

- Purpose restrictions if gifts were designated for specific programs

- Geographic locations where recipient organizations operate

Qualified donee verification requires us to confirm that recipient organizations maintain their registered charity status at the time we made our gifts. We can verify this information through the CRA's online charity listings.

Gift timing matters for T3010 reporting. We report gifts based on when we made them during our fiscal year, not when recipients received or used the funds.

Property gifts require fair market value assessments and detailed descriptions of the assets we transferred to qualified donees. We must obtain proper valuations for significant property gifts.

International qualified donees have specific reporting requirements when we make gifts to foreign charitable organizations that maintain qualified donee status in Canada.

New Rules for Grants to Non-Qualified Donees with Form T1441

Form T1441 is required when we make grants totaling more than $5,000 to non-qualified donees (grantees) during our fiscal year. This new form implements the qualifying disbursement regime that allows registered charities to work with non-qualified organizations under specific conditions.

Form T1441 requires detailed information about grants made to non-qualified donees, including information about the grant recipients (grantees). We must demonstrate that these grants qualify as charitable disbursements under the Income Tax Act.

Form T1441 reporting requirements include:

- Complete grantee information including names, addresses, and organizational details

- Grant amounts and purposes with specific descriptions of charitable activities funded

- Monitoring and oversight procedures we use to ensure proper use of grant funds

- Documentation requirements including grant agreements and reporting schedules

- Due diligence processes we followed before making grants to non-qualified donees

- Compliance verification showing grantees operate exclusively for charitable purposes

Qualifying disbursement criteria require that grants to non-qualified donees fund activities that would be charitable if carried out directly by our organization. We must maintain oversight and control over how these funds are used.

Documentation standards for Form T1441 require comprehensive grant agreements that specify charitable purposes, reporting requirements, and our right to monitor grantee activities and recover unused funds.

Due diligence obligations include verifying that grantees operate exclusively for charitable purposes and have the capacity to carry out the funded charitable activities effectively.

Reporting thresholds mean we must file Form T1441 when our total grants to all non-qualified donees exceed $5,000 during the fiscal year, regardless of individual grant sizes.

Filing Best Practices and CRA Compliance

Proper filing procedures and compliance practices help ensure our T3010 submission processes smoothly and meets all CRA requirements. The transition to digital-first filing methods offers significant advantages in accuracy, speed, and compliance verification.

To avoid delays, we should sign up to file our returns online using My Business Account (MyBA) or Represent a Client. Understanding the available filing options and establishing proper review procedures protects our charity from costly mistakes and processing delays.

Choosing Between Online and Paper Filing

We should file our T3010 information return online through our CRA account using the interactive form or CRA-certified software. Filing online ensures we identify all necessary forms, sections, schedules and appendices, and receive reminders to attach required documentation.

The CRA strongly encourages online filing as part of their digital-by-default approach. Online services help us avoid delays, possibilities of errors, and the risk of the information return getting lost.

Online filing advantages include:

- Built-in validation that catches common errors before submission

- Automatic form selection based on our charity's circumstances and revenue

- Required attachment reminders ensuring we don't miss supporting documents

- Immediate confirmation of successful filing and processing

- Faster processing times typically within days rather than weeks

- Next-day updates to the public List of Charities database

CRA-certified software options provide professional-grade filing capabilities for larger charities or those using accounting firms. We can upload and submit our software-generated return directly through our CRA account in My Business Account or Represent a Client.

Paper filing limitations mean we must print and mail our completed return to the Charities Directorate in Summerside, PEI. Paper returns take longer to process and lack the validation features of online filing.

Mailing address for paper returns: Charities Directorate

Canada Revenue Agency

105-275 Pope Road

Summerside PE C1N 6E8

Using My Business Account or Represent a Client

Filing our T3010 through My Business Account is easy. It helps us identify all necessary forms, sections, schedules and appendices. It also reminds us to attach required documentation.

My Business Account (MyBA) serves charities that handle their own T3010 filing internally. This account provides direct access to our charity's information and filing history with the CRA.

Represent a Client accounts allow authorized representatives like accountants, lawyers, or consultants to file returns on our behalf. Professional representatives often use this system to manage multiple charity accounts.

Setting up online filing requires:

- Valid CRA login credentials linked to our charity's business number

- Authorized signing authority for the person accessing the account

- Current contact information including address, phone, and email details

- Security verification through multi-factor authentication

- Representative authorization if using professional services

Account management responsibilities include keeping our contact information current, updating authorized users when board membership changes, and maintaining proper security protocols.

Access levels can be customized to allow different staff members appropriate permissions for viewing information, preparing returns, or authorizing final submissions.

Technical requirements include compatible web browsers, reliable internet connections, and ability to upload PDF attachments for financial statements and supporting documents.

Review and Sign-Off Procedures for Charity Administrators

Establishing proper review and approval processes helps prevent filing errors and ensures our T3010 accurately reflects our charity's operations and financial position.

Multi-level review should involve our treasurer or finance committee reviewing financial information, program staff verifying activity descriptions, and board leadership providing final authorization.

Essential review procedures include:

- Financial reconciliation ensuring T3010 figures match our audited financial statements

- Program description accuracy verifying that Section C2 describes actual charitable activities

- Director information verification confirming Form T1235 contains current, complete details

- Supporting document checklist ensuring all required attachments are included

- Calculation verification checking that required line totals balance properly

- Deadline compliance confirming filing will occur before the six-month deadline

Board authorization typically requires formal approval from our board of directors before final submission. Many charities pass board resolutions authorizing specific officers to sign and file the T3010.

Documentation retention means keeping copies of our filed T3010, all supporting documents, and board authorization records for at least six years as required by CRA regulations.

Amendment procedures should be established in case we discover errors after filing. We must file amended returns promptly when significant errors are identified.

Professional oversight through qualified accountants or charity law specialists can provide additional validation and reduce compliance risks, especially for complex returns or first-time filings.

Long-Term Strategies to Prevent Future Mistakes

Building robust internal systems and maintaining proper oversight helps us avoid T3010 filing errors year after year. Proactive compliance management protects our charitable status and reduces the stress of annual filing deadlines.

Establishing consistent procedures and maintaining accurate records throughout the year makes T3010 preparation much easier and more reliable.

Institute Internal Controls and Annual Reviews

Strong internal controls help us maintain accurate financial records and ensure compliance with charity regulations throughout the year. Regular review processes catch potential problems before they become serious filing errors.

We should establish clear procedures for financial management, program reporting, and board governance that support accurate T3010 preparation. These systems work best when multiple people understand our processes and can provide oversight.

Essential internal controls include:

- Monthly financial reconciliation comparing bank statements to accounting records

- Quarterly disbursement quota tracking ensuring we meet annual spending requirements

- Board meeting documentation with detailed minutes of all governance decisions

- Expense approval procedures requiring proper authorization for all expenditures

- Donation receipt systems ensuring accurate and timely receipt issuance

- Program activity tracking documenting charitable activities and their outcomes

Annual review procedures should include comprehensive assessment of our financial controls, program effectiveness, and compliance with charity law requirements. We should schedule this review well before our T3010 filing deadline.

Segregation of duties prevents errors and fraud by ensuring different people handle financial transactions, record-keeping, and approval processes. No single person should control all aspects of our financial management.

Documentation standards require written policies for expense reimbursement, purchasing procedures, donation processing, and financial reporting. Clear written procedures help maintain consistency when staff or board members change.

Regular training for board members and staff ensures everyone understands their compliance responsibilities and knows how to implement our internal control procedures properly.

Maintain Records and Track Disbursement Quota

Proper record-keeping supports accurate T3010 filing and protects us during CRA audits or compliance reviews. We must maintain comprehensive documentation for all our financial transactions and charitable activities.

A registered charity must keep adequate books and records that allow the CRA to verify revenues, including all charitable donations received, verify that resources are spent on charitable programs, and verify that the charity's purposes and activities continue to be charitable.

Our record-keeping requirements include:

- Governing documents including incorporating documents, constitution, bylaws

- Financial statements and supporting documentation for all fiscal years

- Official donation receipts and copies of all receipts issued

- Annual information returns including all filed T3010 forms and attachments

- Meeting minutes for board, committee, and member meetings

- Source documents such as invoices, contracts, bank statements, and expense accounts

Records must be kept at the Canadian address that the charity has on file with the CRA, including all books and records related to any activity carried on outside Canada.

Disbursement quota tracking requires ongoing monitoring of our charitable spending throughout the fiscal year. We must spend at least 3.5% of our total assets from the previous year on charitable activities and qualifying disbursements.

Retention periods vary by document type:

- Donation receipts: Minimum 2 years from the end of the calendar year donations were made

- Financial statements and T3010 forms: 6 years from the end of the last tax year they relate to

- Governing documents and meeting minutes: For the life of the charity plus 2 years after revocation

- 10-year gift records: For the life of the charity plus 2 years after revocation

Electronic record-keeping is acceptable but must follow specific requirements. Electronic records must be kept in an electronically readable format and be accessible from Canada, even if backup copies are stored elsewhere.

Know When to Consult a Charity Lawyer or Expert

Professional guidance helps us navigate complex charity law requirements and avoid costly compliance mistakes. Knowing when to seek expert advice can save our organization significant time, money, and regulatory problems.

We should consult charity law specialists when facing significant organizational changes, complex transactions, or regulatory uncertainties. Professional advice is especially important for new charities or organizations with limited compliance experience.

Situations requiring professional consultation include:

- Establishing new charities and navigating the registration process

- Major program changes that might affect our charitable purposes

- Complex financial transactions involving property transfers or investments

- Related party dealings with directors, major donors, or connected organizations

- Compliance issues arising from CRA audits or enforcement actions

- Merger or dissolution procedures requiring legal documentation

Qualified charity lawyers specialize in the Income Tax Act provisions governing registered charities and understand both federal and provincial regulatory requirements.

Charity accounting specialists provide expertise in financial statement preparation, T3010 completion, and ongoing compliance management systems.

Professional associations like the Canadian Association of Gift Planners and Association of Fundraising Professionals offer continuing education and networking opportunities for charity professionals.

Cost-benefit analysis should consider the potential consequences of compliance mistakes versus the cost of professional advice. CRA penalties, audit costs, and potential loss of charitable status often far exceed professional consultation fees.

Ongoing relationships with qualified professionals provide continuity and familiarity with our organization's specific circumstances and compliance history.

Conclusion

Filing our T3010 correctly protects our charity's future and demonstrates our commitment to transparency and accountability. The strategies we've outlined help us avoid the most common mistakes that lead to processing delays, penalties, and compliance issues with the CRA.

Building strong internal controls and maintaining proper records throughout the year makes T3010 preparation much easier and more reliable. When we establish consistent procedures and seek professional guidance when needed, we can focus on our charitable mission instead of worrying about regulatory compliance.

For complex T3010 situations or ongoing charity law support, the experienced team at Charity Law Group provides specialized guidance to help Canadian charities navigate regulatory requirements successfully. Visit https://www.charitylawgroup.ca/ to learn how we can support your organization's compliance and governance needs.

Frequently Asked Questions

These frequently asked questions address the most common concerns we encounter when helping charities navigate T3010 filing requirements and compliance issues.

What are the common errors to avoid when completing the T3010 Registered Charity Information Return?

The most frequent errors include using outdated T3010 forms, missing required attachments like Forms T1235 and T1236, incomplete director information without postal codes or birth dates, and financial calculations that don't balance properly.

What is the penalty for late filing T3010?

Late filing results in automatic penalties of $500 per month until we submit our return. The CRA can revoke our charitable status if we fail to file for one full year.

What are the essential documents that need to be attached to the T3010 return?

Essential attachments include complete financial statements, Form T1235 with director information, Form T1236 for qualified donee gifts, and Form T1441 if grants to non-qualified donees exceed $5,000.

Is there a penalty for filing an amended return?

No, the CRA does not impose specific penalties for voluntarily filing amended T3010 returns to correct errors.

How do I correct an error for filing the T3010 form, and what are the implications of mistakes?

We can request changes online through My Business Account or by mail to the Charities Directorate. Mistakes can cause processing delays and may trigger compliance reviews.

What happens if I don't amend my return?

Failing to amend known errors can escalate into serious compliance issues, including penalties, sanctions, or potential loss of charitable registration.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)