A Guide to CRA Compliance for Private Foundations in Canada

Published on

June 23, 2024

Last updated on

July 15, 2026

Private foundations play a crucial role in charitable giving, but managing them comes with several limitations and requirements. If you're considering setting up a private foundation in Canada, it's important to understand these restrictions and obligations. Let's explore what these limitations are and how they affect the operation of private foundations.

Administrative and Financial Compliance Requirements

Operating a private foundation offers a rich and rewarding experience, although it may come with its own set of complex challenges. There are considerable administrative and financial tasks that must be handled correctly.

- Corporate Procedures: Foundations need to follow specific corporate procedures. This means regularly holding meetings and documenting them accurately.

- Corporate Filings: Foundations must complete regular filings with government authorities to ensure they remain in good standing and operate transparently.

- Annual Information Returns (Form T3010): Every year, foundations must file this form, which details their activities, finances, and compliance with charity laws.

- Keeping Books and Records: Accurate and thorough records of all financial transactions and activities are essential. This is crucial for audits and demonstrating accountability.

Donation Receipts: When receiving donations, foundations must issue receipts that meet specific regulatory requirements, allowing donors to claim tax deductions.

Common Compliance Mistakes to Avoid

Many private foundations run into trouble with the CRA due to preventable errors. Here are the most common mistakes:

1. Missing T3010 Filing Deadlines

The T3010 must be filed within six months of your fiscal year-end. Late filing can result in penalties of $500 or more, and repeated late filings may trigger a CRA audit or compliance review.

2. Inadequate Meeting Minutes Documentation

Board meetings must be documented with proper minutes that include dates, attendees, motions passed, and voting records. Poor documentation makes it difficult to prove governance compliance during audits.

3. Improper Donation Receipt Issuance

Donation receipts must include specific information mandated by the CRA, including the charity's registration number, donor name, date of donation, eligible amount, and proper signatures. Missing or incorrect information can lead to loss of receipting privileges.

4. Poor Record Retention Practices

The CRA requires foundations to keep books and records for at least seven years. This includes financial statements, receipts, board minutes, investment records, and correspondence. Disposing of records too early can create serious problems during audits.

5. Not Updating Corporate Filings After Board Changes

When directors or officers change, foundations must update their records with both the CRA and provincial corporate registries. Failing to do so can result in correspondence going to the wrong people and compliance issues.

6. Confusing Qualified vs. Non-Qualified Investments

Many foundations inadvertently hold non-qualified investments without realizing it. This can lead to penalties and intermediate sanctions.

7. Miscalculating the Disbursement Quota

The disbursement quota calculation is complex and must be done correctly. Underspending can result in penalties, while overspending may deplete the foundation's assets too quickly.

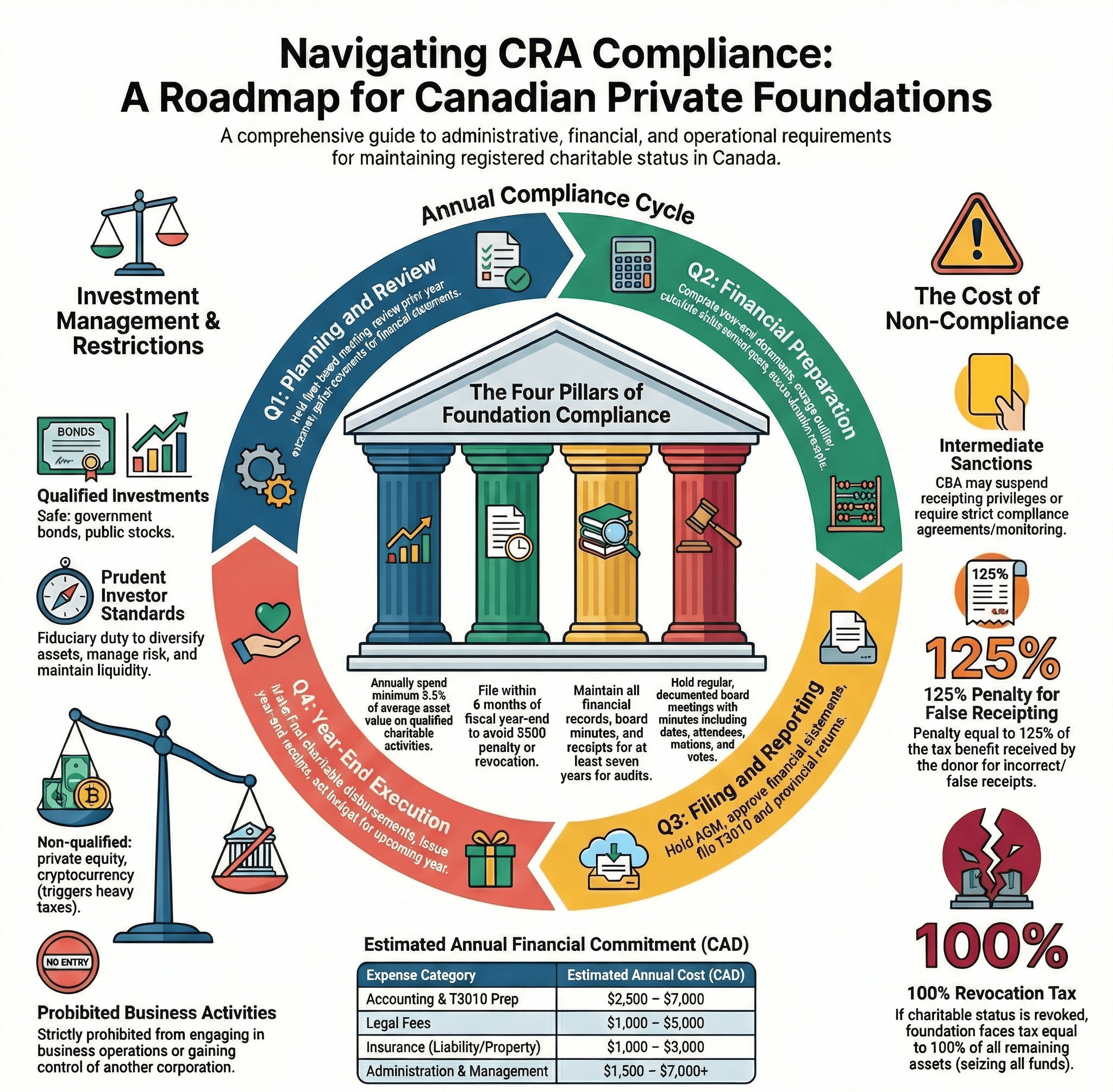

Step-by-Step: Annual Compliance Timeline for Private Foundations

Staying compliant is easier when you know what to do and when. Here's a month-by-month breakdown of key compliance activities:

January - March (Q1): Planning and Review

- Hold first quarter board meeting

- Review previous year's activities and outcomes

- Assess investment portfolio performance

- Begin planning for the year's charitable activities

- Review and update foundation policies if needed

- Start gathering documents for year-end financial statements

April - June (Q2): Financial Preparation

- Complete year-end financial statements (if fiscal year ends March 31)

- Engage accountant or auditor for financial review

- Begin disbursement quota calculations

- Review grant applications received

- Update donor acknowledgment procedures

- Ensure all donation receipts from previous year were properly issued

July - September (Q3): Annual Meeting and Filing

- Hold Annual General Meeting (AGM)

- Approve financial statements

- Elect or re-elect directors

- Prepare and file T3010 Information Return

- File provincial corporate returns

- Review insurance coverage (directors' liability, property, etc.)

- Conduct mid-year financial review

October - December (Q4): Year-End Planning

- Calculate projected disbursement quota for current year

- Make year-end charitable disbursements to meet quota

- Issue year-end donation receipts to donors

- Review investment strategy with advisors

- Plan next year's budget and charitable activities

- Update strategic plan if applicable

- Prepare for upcoming AGM

Ongoing Throughout the Year:

- Maintain accurate financial records

- Document all board decisions

- Issue donation receipts within 30 days

- Monitor investment portfolio

- Keep CRA informed of address or director changes

- Respond promptly to any CRA correspondence

Provincial Statutes Impacting Private Foundations

Private foundations must also adhere to various provincial laws that govern charities. For example, for private foundations located in Toronto, Mississauga, Brampton, Hamilton, Ottawa, or across Ontario:

- Ontario Public Guardian and Trustee: In Ontario, this office ensures that charities comply with laws and operate for the public benefit.

- Charities Accounting Act: This Act outlines how charities must manage their finances.

- Trustee Act: This Act provides guidelines on how trustees should manage the charity's assets.

Operational Restrictions Under the Act

The Act places several restrictions on how private foundations can operate:

- No Business Activities: Private foundations are prohibited from engaging in business activities. Their focus must solely be on charitable endeavors.

- Debt Restrictions: Foundations can only incur debts for specific purposes, such as covering current operating expenses, buying and selling investments, or managing charitable activities.

- Control of Corporations: Private foundations cannot gain control of another corporation, except under certain conditions, such as receiving it as a gift, within set limits.

- Disbursement Quota (DQ) Requirements: Foundations must meet the DQ, which requires them to spend a minimum amount on charitable activities annually.

What Happens If You Violate These Restrictions?

Understanding the consequences of non-compliance is crucial for foundation directors and officers.

Types of Penalties:

1. Financial Penalties The CRA can impose monetary penalties for various infractions:

- Late filing of T3010: $500 minimum

- Issuing false receipts: 125% of the tax benefit received by the donor

- Failing to meet disbursement quota: Penalty equal to the shortfall amount

- Holding non-qualified investments: Tax on income earned from those investments

2. Intermediate Sanctions Before revoking charitable status, the CRA may impose intermediate sanctions such as:

- Suspension of receipting privileges (temporary or long-term)

- Compliance agreements with strict monitoring

- Requirement to provide additional information or documentation

- Restrictions on certain activities

3. Revocation of Charitable Status The most severe consequence is revocation of charitable registration. This can occur when:

- The foundation repeatedly fails to file required returns

- The foundation operates outside its charitable purposes

- The foundation provides improper benefits to directors or donors

- The foundation engages in prohibited activities like business operations

- The foundation fails to meet disbursement quota requirements over multiple years

4. Revocation Tax If charitable status is revoked, the foundation faces a revocation tax equal to 100% of the remaining assets. This effectively eliminates any remaining funds that could have been used for charitable purposes.

Remediation Steps:

If your foundation faces compliance issues:

- Respond immediately to any CRA correspondence

- Seek legal advice from a charity law specialist

- Prepare a detailed remediation plan

- Implement corrective measures quickly

- Document all corrective actions taken

- Consider voluntary disclosure if errors are discovered

- Improve internal controls to prevent future violations

Tax Implications for Donations

Donating to private foundations can have significant tax implications, especially for certain types of contributions:

- Ecologically Sensitive Land: Donating ecologically sensitive land to a private foundation does not exempt the donor from capital gains tax, which might influence the donor's decision.

- Non-Qualifying Securities: Donations of non-qualifying securities, such as certain shares and financial instruments, to private foundations face strict regulations.

Rules on Loanbacks and Non-Qualified Investments

Private foundations must navigate rules regarding loanbacks and non-qualified investments carefully:

- Loanbacks: Loans made to the foundation’s donors or related parties are heavily regulated to prevent misuse of charitable funds.

- Non-Qualified Investments: Foundations need to be cautious about their investments. Holding non-qualified investments can lead to penalties and risks for the foundation.

Investment Management for Private Foundations

Proper investment management is essential for private foundations to maintain their charitable capacity while meeting CRA compliance requirements.

Qualified vs. Non-Qualified Investments Explained

Qualified Investments are investments that private foundations are permitted to hold. These include:

- Government bonds (federal and provincial)

- Publicly traded stocks on designated stock exchanges

- Mutual funds and exchange-traded funds (ETFs)

- Guaranteed investment certificates (GICs) from Canadian financial institutions

- Bonds and securities of Canadian corporations listed on designated exchanges

Non-Qualified Investments are investments that private foundations should avoid or hold only under specific circumstances:

- Shares in private corporations (with exceptions)

- Real estate not used for charitable purposes

- Investments in related businesses

- Certain types of debt obligations

- Any investment that could be considered speculative or risky

The Consequences of Holding Non-Qualified Investments

If your foundation holds non-qualified investments:

- The foundation may be subject to a special tax on income earned from these investments

- Directors may face personal liability in some circumstances

- The CRA may impose intermediate sanctions

- Repeated violations could lead to revocation of charitable status

Prudent Investor Standards

Foundation directors have a fiduciary duty to invest funds prudently. This means:

1. Diversification Don't put all assets in one type of investment. Spread risk across various asset classes and sectors.

2. Risk Management Assess the foundation's risk tolerance based on its time horizon, spending needs, and charitable goals.

3. Regular Review Investment portfolios should be reviewed at least quarterly, with comprehensive annual reviews.

4. Document Investment Decisions Keep records of why specific investments were chosen and how they align with the foundation's investment policy.

5. Consider Liquidity Needs Ensure sufficient liquid assets to meet disbursement quota requirements and operational expenses.

Working with Investment Advisers

Many foundations benefit from professional investment advice. When selecting an adviser:

- Choose advisers with experience in charitable foundation management

- Ensure they understand CRA compliance requirements

- Require regular written reports and recommendations

- Establish clear communication protocols

- Set expectations for performance benchmarks

- Ensure they understand the foundation's values and mission

Creating an Investment Policy Statement

Every private foundation should have a written investment policy that addresses:

- Investment objectives and goals

- Asset allocation targets

- Risk tolerance levels

- Permitted and prohibited investments

- Rebalancing procedures

- Roles and responsibilities

- Performance measurement criteria

- Review and amendment procedures

CRA Guidance Updates

Recent CRA guidance has clarified several investment-related issues:

- Cryptocurrency: Generally considered non-qualified investments for private foundations

- ESG Investing: Socially responsible investments are permitted if they meet qualified investment criteria

- Foreign Investments: Must be qualified investments under Canadian tax law

- Private Equity: Generally non-qualified unless specific exemptions apply

Best Practices for Foundation Investment Management

- Adopt a formal investment policy and review it annually

- Ensure all directors understand their fiduciary investment duties

- Document all investment decisions in board minutes

- Monitor investment performance against benchmarks

- Ensure investments align with the foundation's charitable purpose

- Maintain adequate liquidity for disbursement quota requirements

- Consider both financial returns and charitable impact

- Stay informed about CRA policy changes

Conclusion

Private foundations provide a structured and effective way to support charitable causes, and while they come with numerous limitations and compliance requirements, understanding and adhering to these rules is crucial. By following these regulations, foundations can ensure they operate effectively and continue to make a positive impact on their communities.

Key Takeaways:

- Stay current with T3010 filing deadlines and disbursement quota requirements

- Maintain thorough documentation of all board decisions and financial transactions

- Review investment portfolios regularly to ensure compliance with qualified investment rules

- Plan charitable disbursements strategically throughout the year

- Seek professional advice when facing complex compliance issues

- Keep informed about CRA policy updates and guidance changes

The experienced charity and foundation lawyers at B.I.G. Charity Law Group Professional Corporation are highly regarded in providing reliable legal counsel to philanthropists, family foundations, and private foundations across Canada. Contact us today at 416-488-5888 or ask@charitylawgroup.ca to discuss your foundation law matters and benefit from our unique exclusive practice-area focus.

We are committed to supporting your charitable endeavours and ensuring compliance with the legal requirements governing Canadian foundations, whether in Toronto, across Ontario, or anywhere in Canada.

Frequently Asked Questions About Private Foundation Compliance

What is the difference between a private foundation and a public foundation in Canada?

Private foundations are typically funded by one family or individual, with more than 50% of directors being related parties. They face stricter rules on business activities, investments, and corporate control. Public foundations receive funding from multiple unrelated sources, must have more than 50% unrelated directors, and have greater operational flexibility with fewer investment restrictions.

How much does it cost to maintain a private foundation annually?

Annual costs typically range from $5,000 to $25,000 or more, including accounting ($2,000-$5,000), legal fees ($1,000-$5,000), T3010 preparation ($500-$2,000), investment management fees (0.5%-2% of assets), insurance ($1,000-$3,000), and administrative costs ($1,000-$5,000). Foundations with assets under $500,000 may find administrative costs consume a significant portion of available funds.

Can a private foundation donate to individuals?

Generally, no. Private foundations must distribute funds to qualified donees like registered charities, municipalities, and certain government organizations. Direct donations to individuals are only permitted when the foundation operates its own charitable programs with proper needs assessments, maintains direction and control, and selects recipients based on charitable need rather than personal relationships.

What percentage of assets must a private foundation spend each year?

Private foundations must spend 3.5% of their average asset base (calculated over the previous 24 months) annually on qualified charitable activities. This is called the disbursement quota. For example, a foundation with $1 million in assets must spend at least $35,000 per year on charitable activities.

Do private foundations pay taxes in Canada?

Private foundations registered as charities are generally exempt from income tax. However, they may face tax on non-qualified investments, income from business activities, revocation tax (100% of assets if charitable status is revoked), and penalties for non-compliance. Investment income earned on qualified investments is tax-exempt.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)