CRA Draft Guidance on Charity Administration and Management

Published on

February 25, 2026

Last updated on

March 2, 2026

The Canada Revenue Agency is working on draft guidance about administration and management for registered charities. This new guidance will help charities understand what the CRA expects regarding their operations and daily activities.

While the final version has not been released, charities need to be aware of possible changes and their impact. The CRA has shared some early details through presentations and sector updates.

These details suggest that the guidance will cover important areas affecting how registered charities operate. Understanding CRA expectations will help your charity stay compliant and avoid registration issues.

This article explains what the CRA has shared about administration and management. It also covers why the guidance matters and how your charity can prepare.

You will learn about key areas the guidance might address, how it relates to other compliance rules, and practical steps your charity should take now.

What Is The CRA Charities Directorate Working On?

The Charities Directorate has set several priorities for the 2024-2025 fiscal year and beyond. These efforts aim to improve the program for registered charities and strengthen the sector.

Modernization efforts are a main focus. The directorate is updating internal processes and procedures to better serve charities.

The directorate has three main goals for modernization:

- Enhance operational processes and procedures

- Promote compliance and trust

- Lay a strong foundation for the future

Service improvements are already making a difference. The directorate streamlined the application review process, resulting in a 29% increase in decisions compared to the previous year.

Staff exceeded targets for phone enquiries and accessibility. Education and outreach activities also expanded, with updated guidance documents and new web pages.

Staff attended key events to build relationships with sector stakeholders. Internal training is another focus, with an emphasis on knowledge-sharing and building staff capacity.

This approach creates a stronger base for informed decision-making. The directorate continues to support reviews of the Charities program to ensure it meets sector needs and protects integrity.

All these initiatives aim to make the Charities Directorate a trusted, fair, and people-centred regulator.

Why Administration And Management Guidance Matters For Canadian Charities

Registered charities in Canada must follow strict rules set by the CRA's Charities Directorate. The draft guidance clarifies what organizations can and cannot do to remain compliant.

Key reasons this guidance is important:

- Sets clear boundaries for administrative spending and activities

- Helps charities avoid compliance mistakes

- Provides practical advice for operating a registered charity

- Reduces the risk of audits, sanctions, or loss of charitable status

The CRA registers organizations and monitors their activities to ensure compliance with Canadian charity law. Without clear guidance, charities may struggle to know if their administrative practices meet standards.

Many organizations wonder how much they can spend on administration versus charitable purposes. The draft guidance addresses these questions and covers management practices and proper use of resources.

The Charities Directorate provides education and handles compliance activities. Clear guidance helps charities make better decisions and focus on their mission.

Charity regulation in Canada requires balancing effective operations with proper resource allocation. The guidance offers a reference point for building policies and procedures.

Organizations that follow CRA guidance are more likely to keep their registered status and avoid penalties. Understanding administration and management rules protects both the charity and its donors.

Key Areas The CRA Draft Guidance On Administration And Management Is Expected To Cover

The CRA's upcoming guidance will address how charities should structure governance, manage financial controls, and protect assets. These requirements affect daily operations, from board meetings to issuing donation receipts.

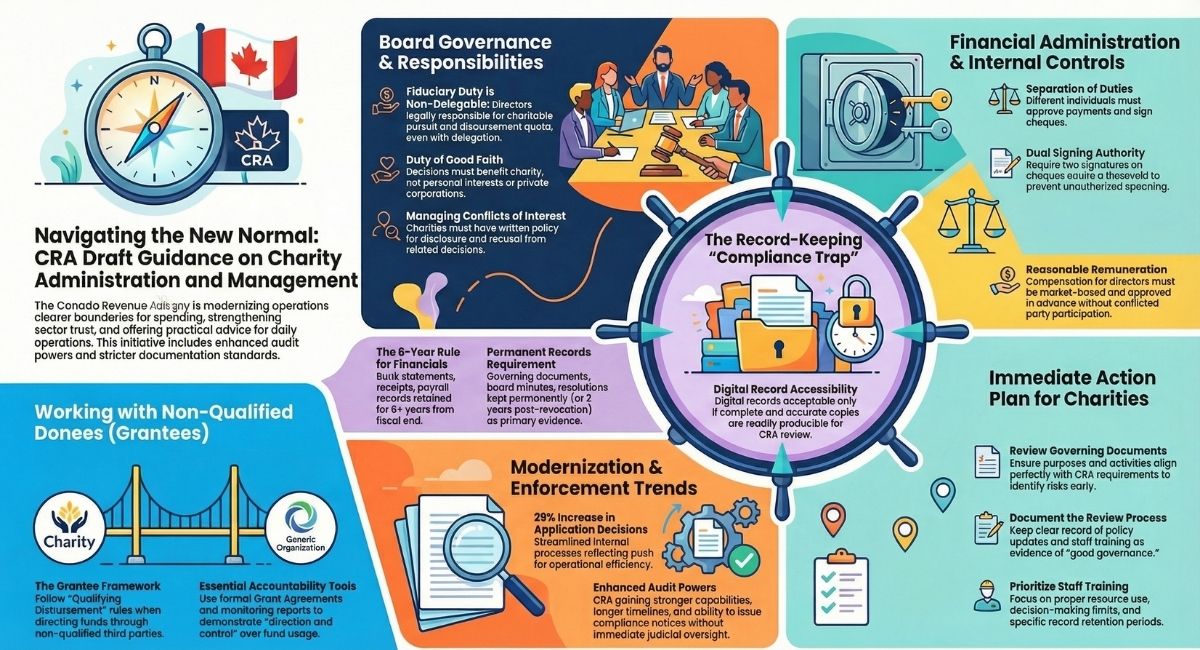

Director And Officer Responsibilities

Directors and officers have legal obligations to ensure their charity operates within the Income Tax Act and pursues charitable activities. Board members must understand the charity's governing documents and make informed decisions.

They need to attend meetings regularly and review financial statements before approval. Directors must ensure the charity meets its disbursement quota each year.

Board members cannot simply rely on staff or other directors for governance matters. The guidance will stress that directors must act honestly and in good faith, making decisions that benefit the charity.

Directors who fail to meet these standards may put the charity's registration at risk.

Delegation Of Authority And Internal Controls

Charities can delegate tasks, but the board remains responsible for oversight. The guidance will describe how boards should set clear delegation policies outlining decision-making and spending authority.

Internal controls protect assets and ensure accurate records. The CRA expects charities to separate duties, such as having different people approve payments and sign cheques.

Written policies help document these controls. Charities should establish procedures for handling donations, issuing receipts, and managing expenses.

Regular reviews of controls help identify weaknesses early.

Conflicts Of Interest Policies

A written conflict of interest policy helps board members manage situations where personal interests could affect judgment. Charities must have and consistently follow these policies.

Board members must disclose conflicts, including financial interests and relationships. A director with a conflict should not participate in related discussions or votes.

The policy should cover transactions with related parties, including remuneration. Charities must document how they identified and addressed conflicts, as the CRA reviews these records during audits.

Financial Administration And Signing Authorities

The board must decide who can sign cheques, approve expenses, and make financial commitments. Written signing authority policies help prevent unauthorized spending.

Most charities require two signatures on cheques above a certain amount. The guidance recommends setting thresholds based on the charity's size and activities.

Signing officers should review supporting documents before signing. The board should approve the annual budget and monitor actual spending throughout the year.

Regular financial reports help directors oversee funds and ensure support for charitable activities.

Record-Keeping Obligations

Charities must keep books and records documenting all transactions and decisions. The CRA requires these records to be kept in Canada, but retention periods vary depending on the type of record — and getting this wrong is one of the most common compliance traps.

Under CRA Guidance CG-002, the following financial records must be retained for at least six years from the end of the fiscal period they relate to: financial statements and supporting documents, bank statements and cancelled cheques, donation records and copies of official donation receipts, employment records and payroll information, and contracts and agreements with third parties.

However, board meeting minutes, resolutions, and governing documents must be kept permanently — or for at least two years after the charity's registration is revoked. These records are the primary evidence of a charity's governance and decision-making, and the CRA treats them differently from financial records. Disposing of them after only six years is a serious compliance error that charities should avoid.

Digital records are acceptable if the charity can produce them when requested. Records must be complete, accurate, and organized for CRA review.

Remuneration Of Directors And Related Parties

Charities can pay reasonable compensation to directors, officers, and related parties for actual services provided. The guidance will explain what the CRA considers reasonable based on market rates and qualifications.

The board must approve all remuneration in advance. Directors with a conflict should not participate in the decision.

The charity must document the reasons for compensation and keep evidence of comparable salaries. Excessive remuneration can lead to loss of registered status.

The CRA checks if payments represent fair value or private benefit. Charities should review compensation regularly and update policies as needed.

Use Of Charity Assets

All charity property and funds must be used for charitable activities or gifts to qualified donees. The guidance will address how to protect assets from misuse.

Charities cannot operate for the benefit of private individuals or corporations. Asset use policies should explain how the organization safeguards property and resources.

The board must ensure any personal use of assets is minimal, documented, and reimbursed at fair market value. When directing funds through third-party organizations that are not qualified donees — referred to under the CRA's updated statutory framework as Grantees — charities must follow the Qualifying Disbursement rules introduced under Bill C-19.

Under these rules, a charity cannot simply transfer funds to a Grantee and count it as a qualifying disbursement. The charity must retain direction and control over how those funds are used. To demonstrate this, charities are required to use specific accountability tools, including a formal Grant Agreement that sets out roles, permitted uses of funds, and reporting obligations, as well as ongoing monitoring reports that confirm the Grantee is using the funds for the intended charitable purpose.

Governing documents should include provisions for transferring assets to qualified donees if the charity dissolves.

How CRA Draft Guidance Fits Into The Broader Compliance Picture

The CRA is expanding its enforcement powers in tax compliance. Recent draft legislation shows a focus on better tax transparency and stronger audit capabilities.

Key enforcement areas include:

- Information requests and compliance orders

- Cross-border reporting requirements

- Enhanced audit powers with longer timelines

- Stricter documentation standards

The draft guidance on administration and management is part of this broader oversight. The CRA is gaining more tools to verify that charities meet their obligations.

These changes affect how charities document activities and maintain records. Financial institutions face similar scrutiny, and the CRA consulted on reporting standard updates in 2025 to combat tax avoidance.

What this means for charities:

The agency can now issue compliance notices in some cases without immediate judicial oversight. Charities must keep detailed documentation of decisions and operations, including board minutes and financial records.

Tax shelters remain under watch as part of CRA’s strategy. While most charities do not operate tax shelters, some compliance obligations overlap, such as record-keeping and financial transparency.

Charities should expect more detailed charity audits in the future. The CRA’s enhanced powers mean auditors may request more documentation and conduct thorough reviews.

Organizations need strong internal processes to meet these higher standards.

What Your Charity Should Do Right Now

Charities should review their governing documents to ensure purposes and activities align with CRA requirements. This helps identify potential compliance issues early.

Board members should focus on these key areas:

- Review meeting minutes and decision-making processes

- Document major administrative and management decisions

- Ensure separation between operational and governance roles

- Verify that compensation practices follow CRA guidelines

Organizations should compare current practices to the draft guidance framework. This includes decision-making about resources, staff, and program delivery.

Charities can access CRA’s new resources to better understand compliance requirements. These materials help organizations adapt to changes without needing pre-approval.

Leadership teams should prioritize staff training on these topics:

- Proper use of charitable resources

- Decision-making authority and limits

- Record-keeping requirements

- Conflict of interest policies

Attending CRA and sector webinars offers valuable updates and practical examples. These sessions also provide opportunities to ask questions.

Organizations should document their review process and any policy changes. This creates a clear record of compliance efforts and shows good governance to the CRA.

Charities may want to consult legal advisors or charity law specialists for complex issues. Professional guidance ensures the organization interprets requirements correctly and implements needed changes.

How B.I.G. Charity Law Group Can Help

B.I.G. Charity Law Group specializes in charity and non-profit law across Canada. The firm has worked with charitable organizations since 2015.

Their team focuses only on legal issues that affect charities and non-profits.

The firm helps charities understand and follow CRA's draft guidance on administration and management. They can review a charity's current practices to find areas that may not meet new requirements.

This includes checking governance structures. They also review internal policies and operational procedures.

Services the firm provides include:

- Registration applications for new charities

- Compliance reviews and audits

- Guidance on proper tax receipt issuance

- Help with CRA inquiries or audits

- Board governance advice

- Policy development and updates

The lawyers at B.I.G. Charity Law Group explain complex legal requirements in clear terms. They work with charities to create practical solutions that meet legal standards and support the organization's mission.

When charities need to update their operations, the firm provides step-by-step guidance. They help organizations prepare for CRA reviews by ensuring policies and procedures align with current regulations.

The firm also assists charities dealing with CRA concerns. This includes responding to compliance letters and resolving disputes about charitable status.

Organizations can contact B.I.G. Charity Law Group to discuss specific legal concerns. The firm offers consultations to help charities assess their current situation and determine next steps.

Frequently Asked Questions

The CRA's draft guidance on administration and management raises questions about compliance requirements, governance standards, record-keeping, relationships with non-qualified donees, resource allocation, and transparency obligations for registered charities.

How can Canadian registered charities ensure they are compliant with the new administration and management guidance?

Registered charities should review their current practices against the draft guidance as soon as the final version is released. This includes examining how they allocate resources between charitable activities and administrative functions.

Charities must ensure their T3010 return accurately reflects their administration and management expenses. The CRA uses this annual return to monitor how organizations spend their funds and whether they maintain proper oversight.

Board members and staff should receive training on the updated requirements. This helps everyone understand their responsibilities and reduces the risk of non-compliance.

What are the key changes to the Canada Revenue Agency's expectations for charity governance?

The CRA is developing clearer standards for how charities should govern themselves and manage their operations. These standards will likely address board oversight responsibilities and decision-making processes.

Charities can expect more detailed guidance on the difference between governance activities and day-to-day management. The CRA wants to ensure board members provide proper oversight without crossing into operational roles that belong to staff.

The guidance may also clarify acceptable levels of management and administration expenses. While charities need administrative functions, the CRA expects most resources to go toward charitable purposes.

Could you outline the steps for proper record-keeping as per the updated CRA guidelines for registered charities?

Charities must maintain books and records that show how they spend their money on both programs and administration. These records need to demonstrate that qualifying disbursements meet the required thresholds each year.

Documentation should include board meeting minutes that show governance decisions and oversight activities. This proves the board is actively managing the charity's affairs.

Financial records must clearly separate charitable activities from administration and management costs. This breakdown is essential for completing the T3010 return accurately and showing the CRA how resources are allocated.

Charities should keep records for at least six years from the end of the fiscal period. These documents must be available for CRA review upon request.

What are the implications of the new guidance for a charity's relationship with non-qualified donees?

The guidance will likely address how charities can work with non-qualified donees while maintaining control over their resources. Charities remain responsible for ensuring funds are used for charitable purposes even when working with other organizations.

A charity cannot simply transfer funds to a non-qualified donee and count this as a qualifying disbursement. The charity must maintain direction and control over how the funds are used.

Charities need written agreements that outline roles, responsibilities, and reporting requirements when working with non-qualified donees. These agreements help demonstrate that the charity retains control over its resources.

How might the updated CRA guidance affect the allocation of a registered charity's resources?

Charities will need to evaluate whether their current spending on administration and management falls within acceptable ranges. The guidance may provide benchmarks or frameworks for assessing whether administrative costs are reasonable.

Organizations should review their qualifying disbursements to ensure they meet the disbursement quota requirements. Administrative expenses typically do not count toward this quota, so excessive administration costs could create compliance issues.

Charities may need to adjust their budgets to ensure sufficient resources go toward direct charitable activities. This could involve reducing administrative overhead or finding more efficient ways to manage operations.

The guidance might also clarify which expenses count as program delivery versus administration. This distinction affects how charities report their activities on the T3010 return.

What measures should be taken to adhere to the transparency requirements set forth by the CRA in the updated guidance?

Charities should ensure their T3010 return is complete and accurate. This return is a primary transparency tool that the public can access to see how charities spend their money and conduct their operations.

Organizations need to maintain clear documentation of their governance processes and major decisions. This includes keeping minutes of board meetings and records of how the board oversees management.

Charities should be prepared to explain their administration and management expenses to stakeholders. They should have clear reasons for spending decisions and be able to show how these costs support charitable purposes.

Public communication materials should accurately reflect how the charity operates and allocates its resources. Misleading information about administration costs or program spending could raise concerns with the CRA.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

.png)