Charitable Purpose vs Activity in Canada: Key Differences

Published on

January 7, 2025

Last updated on

July 19, 2026

When applying to register a charity in Canada, the CRA draws a firm distinction between charitable purposes and charitable activities. These are not interchangeable terms — and confusing them is one of the most common reasons charity registration applications are delayed or denied.

This guide explains exactly what each term means, how the CRA evaluates them in 2026, and how to make sure your organization gets both right from the start.

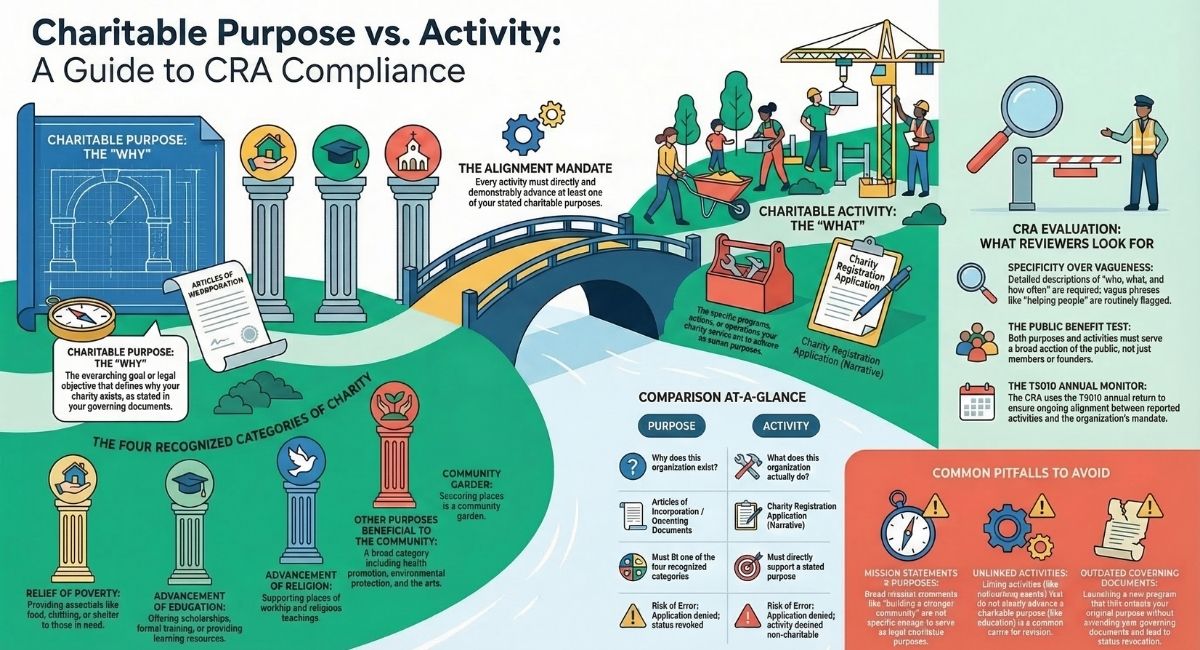

What Are Charitable Purposes?

Charitable purposes refer to the overarching goals or objectives that define why the organization exists. These purposes must fall under one or more of the four categories recognized as charitable under Canadian law:

- Relief of Poverty: Initiatives such as providing food, clothing, or shelter to those in need.

- Advancement of Education: Activities like offering scholarships, conducting educational programs, or providing resources for learning.

- Advancement of Religion: Supporting places of worship, religious teachings, or other spiritual activities.

- Other Purposes Beneficial to the Community: This broad category includes purposes like promoting health, protecting the environment, or supporting arts and culture.

The CRA requires that an organization’s purposes be clearly stated in its governing documents, such as its articles of incorporation. These purposes act as the foundation for all the organization’s activities. Clearly defining these purposes in the articles of incorporation is essential, as they serve as the legal and strategic blueprint for the charity’s existence.

What Are Charitable Activities?

Charitable activities are the specific actions or programs undertaken by a charity to achieve its charitable purposes. While purposes answer the question, “Why does this organization exist?” activities address “What does this organization do?”

Examples of charitable activities include:

- Relief of Poverty: Operating a food bank or distributing winter clothing to low-income families.

- Advancement of Education: Hosting free tutoring sessions or creating online learning resources.

- Advancement of Religion: Organizing worship services or distributing religious literature.

- Beneficial to the Community: Running a community garden or offering free health clinics.

The activities detailed in the actual charity application must directly demonstrate how they support the purposes outlined in the articles of incorporation. This alignment ensures that the CRA can clearly see the connection between the charity’s objectives and its day-to-day operations.

Charitable Purpose vs Charitable Activity: At a Glance

What the CRA Actually Looks For in 2026

When reviewing a charity application, the CRA examines purposes and activities together — not separately. Here is what reviewers specifically assess:

1. Are the purposes legally charitable? Your stated purposes must fit within one of the four recognized categories under Canadian common law: relief of poverty, advancement of education, advancement of religion, or other purposes beneficial to the community.

2. Are the activities described in enough detail? Vague activity descriptions such as "we will help people in need" are routinely flagged. The CRA expects a clear, specific account of what your organization will do, who it will serve, and how often.

3. Is there a direct link between purposes and activities? Each activity must demonstrably advance at least one charitable purpose. If your purpose is advancing education, but your main described activity is hosting networking events for professionals, the CRA will question the connection.

4. Do the activities benefit a sufficiently broad section of the public? Activities must serve the public — not just members, founders, or a closed group. This is known as the public benefit requirement, and it applies to both purposes and activities.

For guidance, the CRA publishes policy documents such as CPS-024 (Guidelines for Registering a Charity: Meeting the Public Benefit Test) and CG-019 (How to Draft Purposes for Charitable Registration). Reviewing these before submitting your application is strongly recommended.

Why Does the Difference Matter?

Understanding the distinction between charitable purposes and activities is essential for compliance and operational clarity. Here is why:

1. Compliance with CRA Requirements

The CRA evaluates an organization's eligibility for charitable status based on its stated purposes and the activities that support them. If the activities do not align with the purposes, the application may be denied, or the charity could face penalties. In 2026, the CRA continues to enforce strict alignment between purposes and activities. Applications that describe activities without clearly connecting them to a recognized charitable purpose are returned for revision — often adding months to the process.

2. Transparency and Accountability

Clearly defined purposes and activities ensure that donors and stakeholders understand how their contributions are used. Donors, funders, and granting bodies increasingly review a charity's T3010 annual return, where activities are reported publicly. Well-defined purposes and activities signal organizational credibility.

3. Operational Efficiency

When purposes and activities are well-defined, it becomes easier for the organization to plan, execute, and evaluate its programs.

4. Protection Against Revocation

If a registered charity begins conducting activities that no longer align with its stated purposes — without formally amending its governing documents — it risks losing its charitable status during a CRA audit. This is one of the leading causes of charitable status revocation in Canada.

Real-World Examples of Purpose vs Activity Alignment in Canada

✅ Aligned Example — Advancement of Education

- Purpose: To advance education by providing financial assistance to students from low-income families in Ontario.

- Activity: Administering an annual bursary program for post-secondary students who demonstrate financial need, with a formal application and selection process.

- Why it works: The activity is specific, measurable, and directly tied to the purpose.

❌ Misaligned Example — Advancement of Education

- Purpose: To advance education in Canada.

- Activity: Hosting fundraising galas and networking dinners for community members.

- Why it fails: The activities do not clearly advance education. The CRA will question whether the events serve a charitable function or primarily benefit the organizers.

✅ Aligned Example — Relief of Poverty

- Purpose: To relieve poverty by providing food, clothing, and essential goods to individuals experiencing homelessness in Toronto.

- Activity: Operating a weekly mobile food distribution program and partnering with shelters to distribute donated winter gear.

- Why it works: Both the who (individuals experiencing homelessness) and the what (food, clothing) directly match the purpose.

❌ Misaligned Example — Relief of Poverty

- Purpose: To relieve poverty among low-income families in Canada.

- Activity: Creating public art installations in urban centres.

Why it fails: Without a clearly documented connection between the art program and poverty relief, the CRA will not recognize this activity as charitable under this purpose.

Best Practices for Defining Purposes and Activities

- Draft Clear and Specific Purposes: Use precise language when writing your organization’s purposes. Avoid vague terms that could be interpreted in multiple ways. Ensure these are included in the articles of incorporation to provide a solid legal foundation.

- Ensure Activities Directly Support Purposes: Every activity should have a clear and measurable link to one or more of your charitable purposes. Highlight these in detail in the charity application to illustrate their relevance.

- Regularly Review and Update Documents: As your organization grows, periodically review your governing documents to ensure they accurately reflect your purposes and activities.

- Consult Experienced Charity Lawyers: When establishing or managing a charity, seeking advice from legal and professional advisors, especially charity lawyers, is essential. These experts possess in-depth knowledge of the legal frameworks, compliance requirements, and operational nuances specific to charities.

Common Mistakes When Defining Purposes and Activities

These are the errors the CRA most frequently flags in charity registration applications:

1. Purposes That Are Too Broad

Phrases like "to help the community" or "to promote wellness" are not legally charitable on their own. Your purpose must fit within a recognized category and be specific enough that the CRA can evaluate it.

2. Activities Listed Without Purpose Links

Listing what your charity does without explaining how those activities advance a charitable purpose is one of the most common reasons applications are returned for revision.

3. Mission Statements Used as Purposes

A mission statement is not the same as a charitable purpose. "To build a stronger Toronto" is a mission. "To advance education by providing free after-school tutoring to children in underserved Toronto neighbourhoods" is a purpose.

4. Failing to Update Governing Documents After a Program Change

If your charity launches a major new program after registration that falls outside your original stated purposes, you must apply to amend your governing documents before carrying out that activity. Failure to do so can trigger a CRA compliance review.

How the CRA Monitors Purposes and Activities

The CRA requires charities to file annual returns detailing their activities and how these align with their stated purposes. Failure to provide accurate or complete information can lead to audits or penalties. To maintain good standing:

- Keep detailed records of all activities.

- Ensure all programs directly support your purposes.

- Be transparent in reporting outcomes and expenditures.

As of 2026, the CRA continues to use the T3010 Registered Charity Information Return as its primary annual monitoring tool. Charities must accurately report their programs, resources spent, and how each activity connects to their charitable mandate. Discrepancies between what a charity reports and what it actually does can trigger a compliance review or audit. Keeping your governing documents current and your activity descriptions precise is the most effective protection against CRA scrutiny.

Conclusion

Getting the distinction between charitable purposes and activities right is one of the most critical steps in a successful charity registration application. A single misalignment — or vague language in your governing documents — can delay your application by months or trigger a CRA audit years down the road.

At B.I.G. Charity Law Group, we have helped thousands of Canadian charities get their purposes and activities right the first time. If you are starting a new charity or concerned your current documents may not meet CRA standards, we are here to help.

Call us at 416-488-5888,email us at dov.goldberg@charitylawgroup.ca, or book a free consultation.

Frequently Asked Questions

What is the difference between a charitable purpose and a charitable activity in Canada?

A charitable purpose is the reason your charity exists — such as relieving poverty or advancing education. A charitable activity is the specific program or action your charity takes to fulfil that purpose, such as running a food bank or offering free tutoring. Both must be clearly defined and aligned in your governing documents and registration application.

Can a charity have multiple charitable purposes?

Yes. Many registered charities in Canada have more than one charitable purpose, as long as each falls within a recognized category under Canadian law. All stated activities must support at least one of those purposes.

What happens if my charity's activities do not match its stated purposes?

The CRA may deny your registration application, require revisions, or — if the misalignment is discovered after registration — suspend or revoke your charitable status. It is essential to ensure alignment both at the application stage and on an ongoing basis.

Do I need to update my governing documents if my charity starts a new program?

If the new program falls outside your existing charitable purposes, yes — you must apply to amend your governing documents before carrying out that activity. Operating outside your stated purposes is a compliance violation under the Income Tax Act.

Where do purposes and activities appear in the charity registration process?

Charitable purposes must be written into your articles of incorporation or other founding documents. Activities are described in narrative detail within the charity registration application submitted to the CRA.

What is the public benefit requirement, and how does it apply to purposes and activities?

Both your purposes and your activities must demonstrate a clear benefit to the public — not just to a private group or your members. The CRA applies this test during registration and ongoing compliance reviews. An organization that benefits only its founders or a closed membership group will not qualify for charitable status.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)