Why Removing Charitable Status from Churches and Mosques is a Bad Idea

Published on

February 6, 2025

Last updated on

July 26, 2026

Removing the "advancement of religion" as a charitable purpose under the Income Tax Act would fundamentally alter how thousands of churches, mosques, synagogues, and other faith-based organizations operate. This change could jeopardize vital community services and raise serious questions about religious freedom.

The proposal affects about 40 percent of Canadian charities with religious affiliations. These organizations provide essential services like food banks, homeless shelters, and disaster relief programs that benefit all Canadians.

According to Canada Revenue Agency data, approximately 32,000 religious charities currently hold registered status. These organizations collectively receive billions in annual donations, with the tax receipt system incentivizing Canadian generosity. The services they provide reach millions of Canadians yearly, including many who have no religious affiliation.

While Parliament's prorogation has stalled the recommendation, the debate shows changing attitudes toward the role of religious institutions in Canada.

We will examine the current charitable status framework and analyze the potential impacts on communities. This policy change could affect both religious organizations and the broader charitable sector.

The implications reach beyond tax policy, touching on religious freedom, community support systems, and the relationship between faith and public service.

Overview of Charitable Status in Canada

Charitable status in Canada follows specific legal definitions and tax regulations. The Income Tax Act recognizes four main charitable purposes, including the advancement of religion, which gives significant tax benefits to qualifying organizations.

The House of Commons Standing Committee on Finance recently released a report packed with budget recommendations.

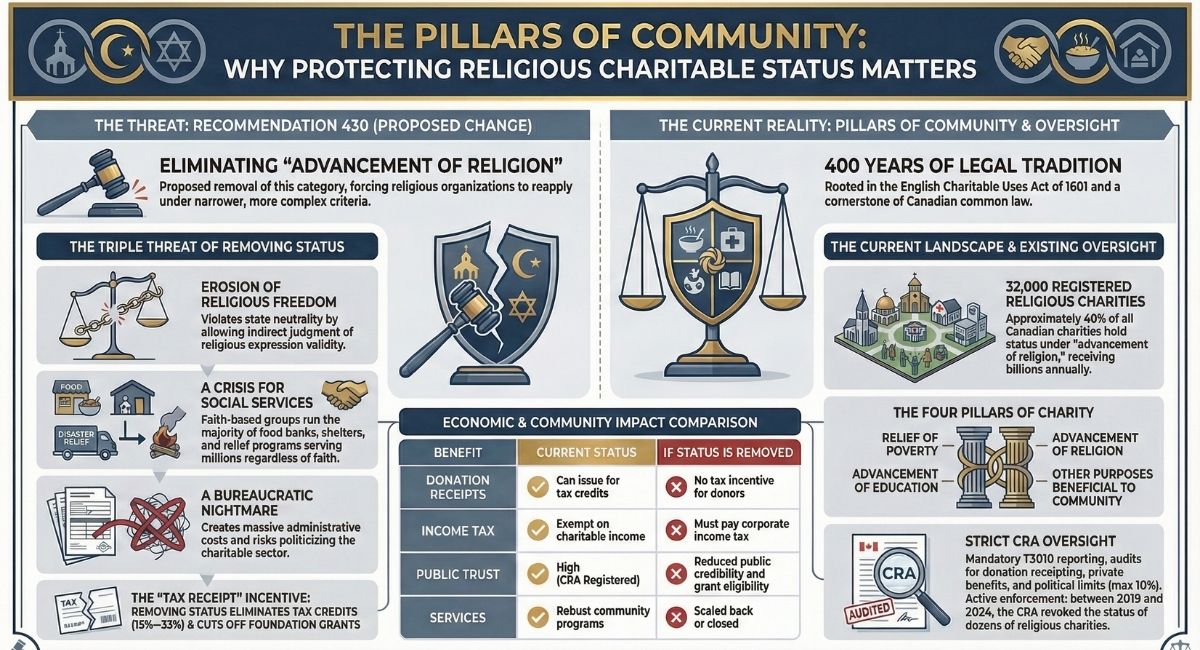

One in particular, Recommendation 430, has raised serious concerns: it proposes changing the definition of "charity" in the Income Tax Act to remove the "advancement of religion" as an automatic charitable purpose.

While seemingly straightforward, this seemingly simple change could have significant, widespread and negative, repercussions for Canadians. [It's important to note, however, that due to the recent prorogation of Parliament, this proposal, along with all other pending parliamentary business, is currently off the table. This means it won't be considered in its current form and would need to be reintroduced in a future session.]

While this buys some time, it doesn't diminish the importance of understanding the potential impact of such a change. The fact that this recommendation was even put forward by a parliamentary committee is very troubling. It signals a potential shift in attitudes towards religious institutions and their role in Canadian society, suggesting that some members of Parliament are willing to reconsider the long-standing principles underpinning charitable status.

This underlying sentiment remains, even if the specific proposal is temporarily stalled, and warrants careful attention as it could resurface in future debates. Here are three key reasons why this proposal, and the thinking behind it, is not a good idea and could lead to unintended consequences:

1. Erodes Freedom of Religion and Belief: Canada is a nation built on the fundamental principle of freedom of religion and belief. This includes the right to practice one's faith without undue interference. Removing the charitable status of religious organizations could be seen as a subtle, yet significant, erosion of this fundamental freedom. It creates a system where the government indirectly judges the validity of religious expression, potentially leading to discrimination and chilling religious activity. This isn't about giving religious groups a "free pass"; it's about ensuring the government remains neutral in matters of faith, as enshrined in our Charter of Rights and Freedoms.

2. Impacts Vital Community Services: Many religious organizations provide crucial social services that benefit all Canadians, regardless of their religious beliefs. Food banks, homeless shelters, addiction support groups, and disaster relief efforts are often run or supported by faith-based charities. Altering their charitable status could jeopardize their funding, making it more difficult to deliver these essential services to the most vulnerable members of our society. This isn't about subsidizing religion; it's about recognizing the valuable work these organizations do in filling gaps in our social safety net. Weakening them ultimately hurts the communities they serve.

3. Creates a Bureaucratic Nightmare: Redefining "charity" and requiring religious organizations to re-apply for charitable status based on other criteria opens a Pandora's Box of bureaucratic red tape. This would create a costly and time-consuming process for both the charities and the government. Imagine the administrative burden of evaluating the "worthiness" of every religious organization seeking charitable status. Who decides? What criteria are used? This process is not only inefficient but also risks politicizing charitable giving, potentially leading to arbitrary decisions and a chilling effect on philanthropic activity. It's a recipe for administrative headaches and potential abuse.

While the stated intent behind Recommendation 430 might be to create a more "level playing field," the unintended consequences could be far-reaching and detrimental to Canadian society.

Bottom line, Recommendation 430 threatens religious freedom, jeopardizes vital community services, and creates unnecessary bureaucratic hurdles. For these reasons, this proposal, even in its currently stalled state (as the government is prorogued, with all legislation needing to be retabled), and the underlying sentiment it represents, deserves serious reconsideration.

Definition of Charitable Purpose

The Income Tax Act defines four categories of charitable purpose: relief of poverty, advancement of education, advancement of religion, and other purposes beneficial to the community.

Religious organizations qualify automatically under the advancement of religion category. Churches, mosques, temples, and synagogues don't need to prove additional community benefits.

Each category receives the same tax benefits. Organizations can issue tax receipts to donors and don't pay income tax on their charitable activities.

The Canada Revenue Agency oversees these definitions and ensures organizations meet the legal requirements for charitable status.

Origins of Advancement of Religion

The advancement of religion as a charitable purpose comes from English common law. This legal tradition dates back over 400 years in British courts.

Canadian law adopted these principles when our legal system was established. The concept recognizes that religious activities benefit society as a whole.

Courts have traditionally viewed religious practice as inherently charitable, assuming that spiritual guidance and moral instruction serve the public good.

The Charitable Uses Act of 1601 in England first established these principles. Canadian courts have referenced this law for centuries when making charitable status decisions.

Role of Income Tax Act

The Income Tax Act formally defines charitable purposes in Canadian tax law. This federal legislation governs how charitable organizations operate and receive benefits.

Section 149.1 outlines the requirements for charitable status. Organizations must be established and operated only for charitable purposes.

Charitable organizations pay no income tax on income used for charitable purposes, and donors can claim tax credits for their contributions.

The Act also sets rules for how charities must operate. They cannot engage in prohibited political activities and must file annual returns with the Canada Revenue Agency.

Parliament must approve changes to the Income Tax Act. Any modifications to charitable purpose definitions would need new legislation.

What CRA Currently Requires from Religious Charities

Before discussing potential changes, it's important to understand that religious charities don't operate without oversight. The Canada Revenue Agency already maintains strict compliance requirements for all registered charities, including religious organizations.

Current Oversight Mechanisms

Religious charities must follow the same rules as all other Canadian charities. The CRA monitors their activities through annual reporting, compliance audits, and complaint investigations.

All registered charities, including churches and mosques, must operate exclusively for charitable purposes. They cannot provide private benefits to members or directors beyond reasonable compensation.

Annual Reporting Requirements

Every religious charity must file a T3010 Registered Charity Information Return annually. This detailed form requires organizations to report their revenues, expenses, assets, and activities.

The T3010 form includes:

- Total revenues broken down by source (donations, government funding, program revenues)

- Complete financial statements showing all expenses

- Compensation paid to the 10 highest-paid positions

- Description of programs and charitable activities

- Details of political activities (if any)

Religious organizations that fail to file their T3010 for two consecutive years automatically lose their charitable status.

Compliance Audits and Reviews

The CRA conducts regular audits of religious charities, just like any other registered charity. These audits examine whether the organization operates according to the Income Tax Act.

Auditors review:

- Donation receipting practices

- Use of charitable funds

- Governance structures

- Record-keeping systems

- Political activity compliance

Religious charities face the same penalties as other charities for non-compliance, including warnings, penalties, and potential revocation of charitable status.

Revocation Statistics

The CRA revokes charitable status from religious organizations that violate the rules. Between 2019 and 2024, the CRA revoked registration from dozens of religious charities for various compliance failures.

Common reasons for revocation include:

- Issuing false donation receipts

- Providing private benefits to members

- Operating for non-charitable purposes

- Failing to maintain adequate books and records

- Engaging in excessive political activities

Common Compliance Issues for Religious Charities

Religious organizations face several compliance challenges unique to their structure. The CRA has identified these as frequent areas of concern:

Donation Receipting Problems: Some religious organizations issue receipts for non-qualifying donations, such as tuition fees for religious schools or payments for services rendered.

Private Benefit Issues: Religious charities sometimes provide benefits to congregation members that exceed what's permitted under charity law, such as subsidized housing or employment preferences.

Political Activity Limits: Religious organizations must ensure their advocacy work stays within the permitted limits. Charities can use up to 10 percent of their resources on political activities, but these must be non-partisan and connected to their charitable purposes.

Why This Matters to the Current Debate

Religious charities already operate under significant government oversight. They're not given a "free pass" simply because they advance religion. The CRA holds them to the same standards as food banks, educational institutions, and poverty relief organizations.

This existing framework demonstrates that charitable status for religious organizations doesn't mean lack of accountability. Any discussion about removing "advancement of religion" as a charitable purpose should acknowledge that these organizations already face substantial regulatory requirements.

Recent Policy Recommendations and Developments

The House of Commons Standing Committee on Finance released a comprehensive report in December 2024 with 462 recommendations for the 2025 federal budget. Two recommendations target religious organizations and anti-abortion groups, potentially removing their charitable status under current tax laws.

Standing Committee on Finance and Its Report

The Standing Committee on Finance tabled Report 21 in the House of Commons on December 13, 2024. This report focused on pre-budget consultations for the 2025 budget.

The 300-page document contained 462 recommendations on federal spending and taxation. Two recommendations specifically targeted charitable organizations based on their religious or ideological purposes.

The report followed consultations with stakeholders across Canada. Because of Parliament's prorogation, all pending business became stalled and the recommendations cannot move forward without reintroduction in a future session.

The finance committee's report represents the views of participating MPs. It does not guarantee government action but signals possible policy directions at the federal level.

Recommendation 430 and Advancement of Religion

Recommendation 430 states: "Amend the Income Tax Act to provide a definition of a charity which would remove the privileged status of 'advancement of religion' as a charitable purpose."

Currently, Canadian law allows organizations to obtain charitable status for four main purposes:

- Relief of poverty

- Advancement of education

- Advancement of religion

- Other purposes beneficial to the community

This recommendation would eliminate the third category. Churches, mosques, synagogues, temples, and other religious organizations rely on this classification for their charitable status.

The change would force religious organizations to reapply under different criteria. They would need to show their work falls under poverty relief, education, or community benefit categories.

Religious groups call this proposal "irresponsible" and a threat to religious freedom. They argue it creates government interference in matters of faith and belief.

Recommendation 429 and Anti-Abortion Organizations

Recommendation 429 proposes that the government "no longer provide charitable status to anti-abortion organizations."

This recommendation targets organizations whose main purpose involves opposing abortion services or advocating for pro-life positions. Many of these groups currently have charitable status.

The proposal would affect organizations like pregnancy support centres, pro-life advocacy groups, and educational organizations focused on alternatives to abortion.

Religious and pro-life groups strongly oppose this recommendation. They see it as targeting organizations based on their beliefs rather than their charitable activities.

Both recommendations 429 and 430 could restrict charitable status for faith-based organizations. Many religious groups operate both as places of worship and as providers of social services or advocacy work.

Impacts of Removing Charitable Status from Churches and Mosques

Removing charitable status would create significant financial barriers for religious organizations. The changes would affect how churches, mosques, and synagogues receive funding and deliver essential services across Canada.

Effect on Donations and Tax Receipts

Churches, mosques, and synagogues would lose their ability to issue charitable tax receipts under the proposed changes. Donors could no longer claim tax deductions for their contributions to places of worship.

Current donation benefits include:

- Tax receipts for donations over $20

- Tax credits worth 15% to 33% of donation amounts

- Ability to carry forward unused credits for five years

Without these incentives, donation levels would likely drop. Many religious Canadians give because tax benefits make their contributions more affordable.

Religious charities would also lose access to foundation grants and other charitable funding sources. Most foundations only donate to registered charities, cutting off important revenue streams for faith-based organizations.

The financial impact extends beyond weekly offerings. Churches and mosques rely on larger donations for building maintenance, community programs, and staff salaries. Reduced giving would force many organizations to cut services or close entirely.

Economic and Social Contributions to Canadian Society

Religious organizations provide essential services that benefit all Canadians. Food banks, homeless shelters, and addiction support programs run by churches, mosques, and synagogues serve thousands of people daily.

Key services provided by religious charities:

- Emergency food assistance through community food banks

- Temporary housing and shelter programs

- Mental health and addiction counselling

- Senior care and support services

- Youth programs and after-school activities

These programs fill critical gaps in our social safety net. Government services often have long wait times or limited capacity, making religious charities vital partners in community support.

The economic impact reaches beyond direct services. Religious organizations employ thousands of Canadians and purchase goods and services from local businesses. They maintain historic buildings, operate community centres, and host cultural events that strengthen neighbourhoods.

Without charitable status, many of these contributions would disappear as organizations struggle with reduced funding and increased tax burdens.

The Role of Religious Charities in Local Communities

Religious organizations provide essential services that reach far beyond their congregations. They support vulnerable populations and strengthen community bonds.

About 40 per cent of Canadian charities fall under the advancement of religion category. These groups deliver social services regardless of religious affiliation.

Social Support and Community Services

Religious groups operate some of Canada's most vital community programs. Churches run food banks that feed thousands of families each week. Mosques provide emergency shelter during harsh winters. Synagogues offer addiction recovery programs.

The Canadian Council of Christian Charities reports that faith-based organizations focus heavily on relief of poverty initiatives. These programs include hot meal services, clothing drives, and housing assistance.

Many religious organizations partner with secular non-profits to expand their reach. A single church might host several community services under one roof, creating efficient hubs where people can access help.

Christian charities operate hundreds of homeless shelters across Canada. Religious organizations also provide disaster relief when floods or fires strike. They respond quickly because they already have established networks and volunteers.

Volunteering and Civic Engagement

Religious charities mobilize thousands of volunteers who donate millions of hours each year. The Evangelical Fellowship of Canada notes that faith communities create strong volunteer networks that extend beyond Sunday services.

These volunteers staff soup kitchens, mentor youth, and visit elderly residents in care homes. They organize neighbourhood cleanups and support newcomer settlement programs.

Research organization Cardus has found that religious participation increases civic engagement overall. People active in faith communities are more likely to volunteer for secular causes too.

They serve on school boards, coach sports teams, and participate in local politics. Religious organizations teach civic responsibility through their programs and connect people to broader community needs.

Analysis of Arguments For and Against Policy Change

The debate over removing "advancement of religion" as a charitable purpose centers on two main viewpoints. Supporters argue for more equal treatment across all organizations, while opponents warn about threats to religious freedom and community services.

Arguments for Removing Charitable Status

Proponents believe religious organizations receive unfair advantages compared to other groups. They argue that automatic charitable status based on religious purpose creates an unequal system.

Some supporters think religious groups should prove their community benefit like other charities do. Under current law, organizations must show they help with poverty relief, education advancement, or community benefit—except religious groups.

The BC Humanist Association and similar groups have argued that religious privilege in tax law violates church-state separation principles. They believe government should not favour religious activities through tax benefits.

Key arguments include:

- Religious organizations get automatic benefits others must earn

- Tax receipts for donations should require proven public benefit

- Current system favours faith-based groups unfairly

During pre-budget consultations, some groups suggested this change would create a more level playing field. They argue religious organizations that help communities can still qualify under other charitable categories.

Reasons Opposing Policy Change

Religious groups and their supporters strongly oppose removing charitable status for several reasons. The Conservative Party has created petitions against what they call the "NDP-Liberal-dominated finance committee" recommendation.

Freedom of religion concerns top the opposition arguments. Many see this change as government interference in religious practice. Canada's Charter of Rights and Freedoms protects religious freedom, and opponents view this as an attack on that principle.

Religious organizations provide large amounts of community service across Canada. Churches, mosques, and synagogues run food banks, homeless shelters, and disaster relief programs that help all Canadians.

Administrative problems would also result from this change. Thousands of religious organizations would need to reapply for charitable status, creating massive bureaucracy for both charities and government officials.

Opposition groups argue this policy would hurt vulnerable people who depend on faith-based social services. They say supporters of the change underestimate how much religious groups contribute to Canadian society.

Potential Long-term Consequences for the Charitable Sector

Removing religious charitable status could destabilize Canada's charitable framework. This change would affect about 40 percent of Canadian charities and reshape support for community organizations.

Threats to the Charitable Sector's Stability

The Finance Committee's recommendation would alter Canada's charitable landscape. Religious organizations make up a large part of the sector, running thousands of food banks, shelters, and community programs.

Immediate structural impacts include:

- Loss of charitable status for tens of thousands of parishes, mosques, and synagogues

- Reduced donation incentives as tax receipts disappear

- Potential closure of faith-based social services

We could see a domino effect across the sector. When religious charities lose funding, other organizations must fill the gaps.

This puts enormous strain on remaining charities and government services. Every religious organization would need to reapply under different criteria, creating large administrative costs for both charities and the Canada Revenue Agency.

Community services would suffer most. Many Canadians rely on faith-based food banks and homeless shelters regardless of their beliefs.

These services often operate more efficiently than government alternatives due to volunteer support and donated facilities.

Broader Cultural and Political Implications

This policy shift signals a major change in how government views religious institutions in Canadian society. We risk creating a two-tiered system where secular causes get more support than faith-based initiatives.

Key political risks include:

- Increased polarization between religious and secular communities

- Government appearing to favour certain worldviews over others

- Constitutional challenges under Charter protections

The House of Commons recommendation could influence future Senate decisions and provincial policies. Other jurisdictions might follow, creating inconsistent charitable frameworks across Canada.

We also risk politicizing charitable giving. When government officials judge the "worthiness" of religious purposes, personal biases can affect decisions.

This undermines the traditional neutrality that helped our charitable sector succeed. Faith communities represent diverse viewpoints and cultural backgrounds.

Alienating these groups could reduce civic engagement and charitable participation in Canadian society.

Conclusion

Parliament may be prorogued, but this issue could return in future sessions. Religious organizations need to understand their rights and prepare for possible changes to charitable status laws.

The advancement of religion has been a cornerstone of Canadian charity law for decades. Removing it would create legal uncertainty for thousands of faith-based organizations across the country.

Religious charities should review their operations and documentation now. Proactive legal planning can help protect your organization's charitable status and mission, no matter what changes come.

Contact B.I.G. Charity Law Group for expert guidance on protecting your religious organization's charitable status. We understand Canadian charity law and can help you navigate these challenges.

Our team at CharityLawGroup.ca has experience helping religious charities maintain compliance and protect their interests. Email us at dov.goldberg@charitylawgroup.ca or call (416) 488-5888 to discuss your organization's needs.

Don't wait for legislation to change. Schedule a FREE consultation today to ensure your religious charity is prepared for the future.

Frequently Asked Questions

Many Canadians have questions about how changes to charitable status would affect religious organizations. The possible removal of "advancement of religion" as a charitable purpose raises concerns about taxes, community services, and the future of faith-based organizations.

Is it possible that the religious organisations, such as the churches or mosques, can no longer be tax exempt?

Yes, if Recommendation 430 becomes law. Religious organizations would need to qualify through other means like poverty relief or education, facing more complex applications and compliance requirements. The proposal is currently stalled due to Parliament being prorogued.

What would removal of charitable status for religious charities (other than churches) mean for Canada?

Faith-based organizations representing 40% of Canadian charities could lose funding and reduce services. Donors would lose tax deductions, decreasing charitable giving and creating gaps in Canada's social safety net for vulnerable populations.

What's the point of tax exemptions for religious groups?

Tax exemptions recognize that religious organizations provide valuable community services, encourage charitable giving through tax deductions, support religious freedom, and help organizations expand their charitable work.

What does charitable status mean for churches and mosques?

Charitable status allows organizations to issue tax receipts, exempts them from income tax, reduces other taxes and fees, and provides public credibility while requiring annual CRA reporting.

Reason, religion and tax: should churches still be considered charities?

Religious organizations provide community benefits including spiritual guidance, social services, and programs like food banks. The debate centers on whether purely religious activities provide measurable public benefit or if spiritual guidance is inherently charitable.

What would happen if churches and mosques lost charitable status?

Organizations would pay income tax reducing program funds, donors would lose tax deductions decreasing donations, operating costs would increase potentially forcing smaller organizations to close, and community services for vulnerable populations would be reduced.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)