What Is a Donation Tax Receipt in Canadian Charities? (Meaning, Rules & Importance)

Published on

March 2, 2026

Last updated on

March 2, 2026

A donation tax receipt is an official document that Canadian registered charities give to donors so they can claim tax credits or deductions on their income tax returns.

These receipts are regulated by the Canada Revenue Agency (CRA) and must follow strict rules.

Charities can only issue them for actual gifts, not for purchases of goods or services.

Understanding how to properly issue donation tax receipts protects both the charity and the donor.

Mistakes can lead to audits, penalties, or even loss of charitable status.

Many charities face compliance problems because they don’t fully understand the receipting requirements.

The privilege of issuing these receipts comes with legal responsibilities that every charity must take seriously.

This guide covers what makes a receipt valid under CRA rules and which donations can be receipted.

It also explains how to avoid common errors and when charities must reduce receipt amounts if they provide something in return.

Following the right practices helps charities stay compliant while supporting their donors.

What Is A Donation Tax Receipt?

A donation tax receipt is an official document that Canadian registered charities give to donors who make financial or in-kind contributions.

The Canada Revenue Agency (CRA) regulates these receipts as legal documents that donors can use to claim tax credits on their income tax returns.

These receipts must include specific information to be valid.

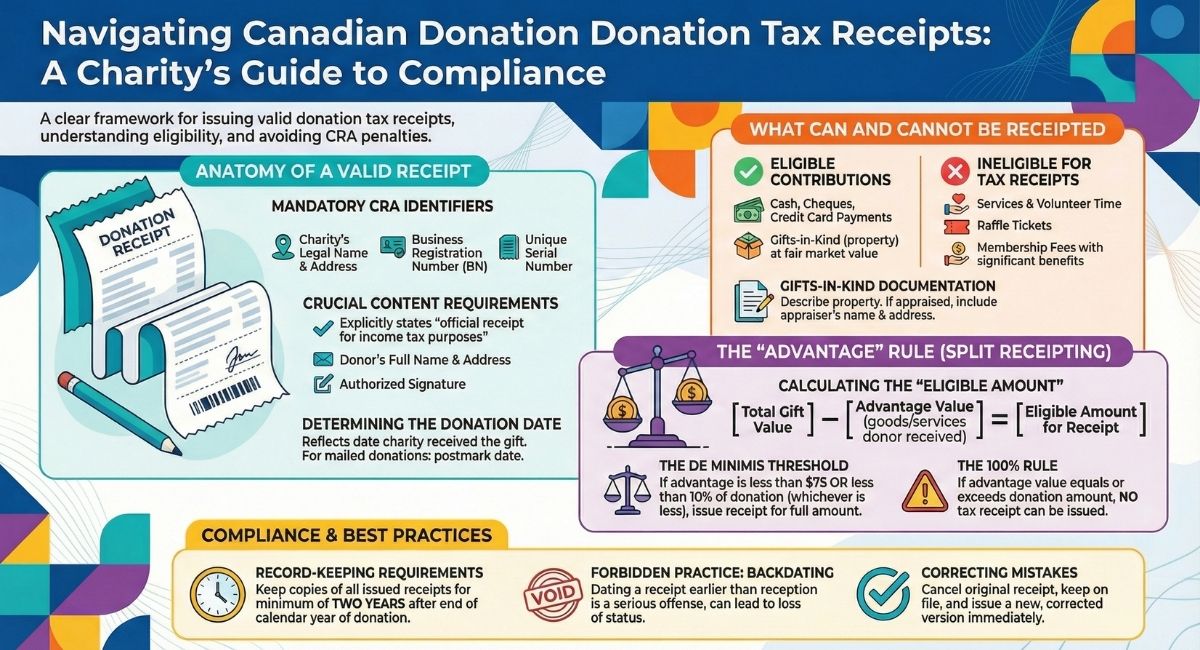

Every official donation receipt needs a statement saying it is an official receipt for income tax purposes.

It must show the charity’s registered name, address, and Business Registration Number (BN) as recorded with the CRA.

The receipt also requires a unique serial number, the donation amount or fair market value of the gift, and the date the charity received the donation.

An authorized signature from the charity must appear on the document.

Key elements of a valid donation receipt:

- Statement identifying it as an official receipt for income tax purposes

- Charity’s legal name and address registered with CRA

- Charity’s Business Registration Number

- Serial number

- Donor’s full name and address

- Date the donation was received

- Amount of cash donation or fair market value of property

- Authorized signature

Only registered charities and qualified donees can issue official donation receipts.

The charity must issue the receipt in the name of the true donor who made the gift.

They cannot issue a charitable tax receipt in someone else’s name, even if requested.

The date of donation is when the charity actually receives the gift.

For mailed donations, the postmark date on the envelope counts as the donation date.

For official CRA compliance rules on issuing receipts, see our Charitable Receipting Guidelines for Canadian Charities.

Who Can Issue Donation Tax Receipts In Canada?

Not every organization in Canada can issue official donation tax receipts.

Only qualified donees registered with the Canada Revenue Agency (CRA) have this authority.

Qualified donees include:

- Registered charities

- Registered journalism organizations

- Registered Canadian amateur athletic associations

- Registered national arts service organizations

- Canadian municipalities

- Municipal or public bodies performing government functions

- The United Nations and its agencies

- Certain universities outside Canada with Canadian students

- Certain foreign charities that Canadian charities have made gifts to

Registered charities make up the largest group of organizations that can issue these receipts.

They must maintain their registered status with the CRA to keep this privilege.

Regular nonprofits that are not registered charities cannot issue official donation tax receipts.

This is a common point of confusion for donors.

An organization might do charitable work, but without proper CRA registration, it cannot provide the tax receipts donors need to claim credits.

The CRA maintains strict oversight of who can issue receipts.

Organizations must follow specific rules about what information appears on receipts and when they can be issued.

Organizations that issue receipts improperly risk losing their charitable status.

Before donating, donors should verify that an organization is a qualified donee.

The CRA provides an online registry where anyone can search for registered charities and other qualified donees.

This helps donors confirm they will receive valid tax receipts for their contributions.

What Must A CRA-Compliant Donation Receipt Include?

The Canada Revenue Agency sets strict rules for what information must appear on an official donation receipt.

Charities that miss required details risk audits, penalties, or loss of their charitable status.

Every receipt must clearly state that it is an official donation receipt for income tax purposes.

This tells donors and the CRA that the document meets legal requirements.

The charity must include its legal name and address as registered with the CRA.

Organizations with a CRA registration number must list it on the receipt.

This includes registered charities, Canadian athletic associations, journalism organizations, and national arts service organizations.

Required donor information includes:

- Full name (first name, last name, and initial for individuals)

- Complete address

Required donation details include:

- Date the gift was received

- Date the receipt was issued

- Amount of the donation

- Eligible amount for tax purposes

- Description of any advantages received (like meals or tickets)

Each receipt needs a unique serial number.

The charity must also include an authorized signature from someone approved to sign receipts.

For non-cash gifts, the receipt must describe the property received.

If the item was appraised, the appraiser’s name and address must appear on the receipt.

The receipt should list the location where it was issued and include the Canada Revenue Agency website: canada.ca/charities-giving.

Charities can issue receipts electronically as long as they contain all required information and are stored securely.

What Types Of Donations Require A Receipt?

Canadian charities must issue official donation receipts for specific types of gifts.

Cash donations always require a receipt when the donor requests one.

This includes payments made by cheque, credit card, or electronic transfer.

Non-cash gifts also qualify for receipting when they have a fair market value.

These donations include items like stocks, bonds, or physical property.

The charity must determine the fair market value of these items at the time of the donation.

Donations that require receipts:

- Cash payments of any amount

- Cheques and money orders

- Credit card and debit card payments

- Stock and securities transfers

- Real estate and property

- Gifts-in-kind with fair market value

Donations that do not qualify for receipts:

- Donations of services or time

- Volunteer hours

- Purchase of raffle tickets

- Auction items (unless the donation amount exceeds the fair market value)

- Membership fees that provide benefits

The donation amount on the receipt must reflect the actual value given.

For gifts-in-kind, charities need to properly assess the fair market value using appropriate valuation methods.

Split receipting applies when a donor receives something in return for their gift.

Donations of services cannot be receipted under Canadian law.

When someone volunteers their time or provides professional services for free, the charity cannot issue a tax receipt for this contribution.

Only actual transfers of cash or property qualify for official donation receipts.

Advantage Rules — When The Charity Provides Something In Return

When a donor receives something in return for their donation, the Canada Revenue Agency calls this an "advantage."

This affects how much the charity can include on the tax receipt.

Split receipting allows charities to still issue a receipt even when donors receive something back.

The charity must subtract the value of what the donor received from the total donation amount.

The result is the eligible amount that goes on the official receipt.

How to calculate the eligible donation amount:

- Start with the total donation value

- Subtract the fair market value of any advantage received

- The remainder is what can be receipted

For example, if someone donates $100 to attend a charity dinner and the meal is worth $30, the eligible amount for the receipt is $70.

The CRA does provide one important exception to this rule. If the advantage the donor receives is worth less than $75 or less than 10% of the donation amount — whichever is less — the charity does not need to subtract it.

In that case, the charity may issue a receipt for the full donation amount. This is called the de minimis threshold, and it is a practical rule that simplifies receipting for small or token benefits.

An advantage can include goods, services, or benefits that the donor receives. It can also include limited-recourse debt related to the donation. The advantage might go to the donor directly or to someone connected to them.

Charities must follow these rules carefully. They need to determine the fair market value of whatever the donor receives. This value must be reasonable and accurate. If the advantage equals or exceeds the donation amount, the charity cannot issue a receipt at all.

The donor must still make a true gift for split receipting to work. There must be some portion of the payment that counts as a genuine donation after subtracting the advantage value.

Why Donation Tax Receipts Matter

Donation tax receipts serve as official legal documents that allow donors to claim tax credits on their contributions.

When a registered charity issues these receipts, donors can reduce the amount of tax they owe to both federal and provincial governments.

The financial benefit to donors is significant.

Tax credits lower a donor’s tax bill directly, making charitable giving more attractive.

Each province offers its own provincial tax credit rate, which combines with the federal credit to provide substantial savings.

For charities, donation receipts are essential fundraising tools.

Donors are more likely to give when they know they can receive tax benefits.

Without the ability to issue official receipts, charities would struggle to attract and retain supporters.

These receipts must meet strict Canada Revenue Agency requirements.

They protect both the charity and the donor by creating a clear record of the transaction.

If a charity issues incorrect receipts or fails to follow CRA rules, it risks penalties, audits, or loss of charitable status.

The receipt confirms key details:

- The donor’s name and address

- The charity’s registration number

- The date the donation was received

- The amount of the gift

Donation receipts also build trust between charities and their supporters.

They demonstrate accountability and transparency in how organizations handle contributions.

When donors receive proper documentation, they feel confident that their gifts are legitimate and properly recorded.

Common Mistakes Charities Make With Donation Receipts

Donation receipt errors are among the most frequent compliance failures for Canadian charities.

These mistakes can trigger CRA audits and lead to serious penalties.

Missing required information is a major problem.

Every receipt needs specific details like the charity’s registration number, a unique serial number, the donor’s full name and address, and the eligible amount.

Missing even one field makes the receipt non-compliant.

Backdating receipts violates the Income Tax Act.

Charities must date receipts on or after the actual date they received the donation.

Backdating to help donors claim donations in a previous tax year is a serious offence that can result in loss of charitable status.

Receipting volunteer time or services is not allowed.

Only transfers of property like cash or securities qualify as gifts.

A volunteer must invoice the charity, get paid, and then donate the money back if they want a receipt.

Issuing receipts for pledges before payment arrives breaks the rules.

The CRA only permits receipts after the charity actually receives the donation.

Reusing or skipping serial numbers creates compliance issues.

Each receipt must have its own unique number that the charity tracks carefully for audit purposes.

Failing to deduct donor advantages is another common error.

When donors receive something in return like event tickets or merchandise, charities must subtract that value from the receipt amount.

Receipting membership fees incorrectly happens often.

Members typically receive benefits equal to their fees, which means no receipt should be issued.

These mistakes put charitable status at risk and can result in penalties ranging from fines to complete revocation of registration.

Best Practices For Managing Donation Receipts

Managing donation receipts properly protects a charity's registered status. It also builds donor trust.

The Canada Revenue Agency enforces strict rules. Mistakes can lead to audits or penalties.

Use a Reliable System

Charities should use receipt management software or a secure database to track donations. The system must store receipts securely to prevent unauthorized changes.

Electronic receipts are allowed if they contain all required information. Charities must be able to reproduce these receipts on request.

Include All Required Information

Every receipt must contain specific details:

- A statement that it is an official receipt for income tax purposes

- The charity's business registration number

- The charity's registered name and address

- A unique serial number

- The date the donation was received

- The donor's full name and address

- The donation amount or fair market value of non-cash gifts

Train Staff and Volunteers

Everyone handling donations should understand CRA requirements. Regular training helps prevent errors such as issuing receipts for ineligible gifts or recording incorrect amounts.

Keep Accurate Records

Charities must keep copies of all issued receipts for a minimum of two years from the end of the calendar year in which the donations were made. They should also record who received receipts and when.

Review Receipts Regularly

Regular audits help catch errors early. Charities should check that serial numbers are in order and that all required information is present.

Correct Errors Promptly

If a charity finds an error on a receipt, it should issue a corrected version immediately. The original receipt should be cancelled and kept on file.

Conclusion

Donation tax receipts are official documents that confirm contributions to registered charities in Canada. They allow donors to claim tax credits and help charities comply with CRA regulations.

Proper receipting protects both the charity's registered status and the donor's ability to receive tax benefits. Canadian charities must follow strict rules when issuing receipts.

Receipts need specific information like the charity's registration number, donor details, and donation amounts. Keeping accurate records and understanding what can and cannot be receipted helps charities avoid audits or penalties.

B.I.G. Charity Law Group helps Canadian charities navigate donation receipting requirements. Our firm provides guidance on receipting practices, gift acceptance policies, and other charitable law matters.

Contact us at dov.goldberg@charitylawgroup.ca or call 416-488-5888 to discuss your charity's receipting policies. Schedule a free consultation or visit CharityLawGroup.ca to learn more about how legal expertise can support your organization's compliance needs.

Frequently Asked Questions

Donation tax receipts in Canada must follow rules set by the Canada Revenue Agency. Charities need to understand these requirements to issue valid receipts for donors.

How do donation tax receipts work in Canada?

Donation tax receipts let Canadian taxpayers claim charitable donation tax credits. When someone gives to a registered charity, they receive an official receipt showing the eligible amount.

The donor keeps this receipt and uses it when filing their tax return. The tax credit reduces the amount of tax owed to the government.

The receipt must come from a charity registered with the Canada Revenue Agency.

What are the legal requirements for issuing a donation tax receipt by Canadian charities?

A charity can only issue an official donation receipt to the person or organization that made the gift. The receipt must include the donor's name and address as provided.

The charity must check if the donation qualifies as a gift before issuing a receipt. They need to calculate the eligible amount by subtracting any benefit the donor received in return.

There is no legal minimum amount required to issue a tax receipt. Charities are not required to issue receipts for donations under $20.

The date on the receipt must be the date the charity received the gift. For mailed donations, the postmark date is used as the receipt date.

Why is it necessary for a charity to provide a tax receipt for donations received?

Tax receipts are legal documents that help donors claim tax credits. Without proper receipts, donors cannot prove their donations to the Canada Revenue Agency.

Issuing correct receipts is also a legal responsibility for registered charities. Mistakes can lead to audits or loss of charitable status.

What is the purpose of a donation receipt?

A donation receipt proves that someone made a charitable contribution. It certifies that the donation meets CRA regulations and qualifies for tax credits.

The receipt includes important details like the charity's registration number and the donation amount. This information helps the donor and the CRA verify the gift during tax filing.

Can a tax deduction for charitable contributions be claimed without a donation tax receipt in Canada?

Donors need to keep their tax receipts to claim charitable donation tax credits. The CRA does not keep a list of individual contributions.

Without a receipt, donors cannot prove they made the donation. The tax receipt is the only acceptable documentation for claiming these tax credits on a Canadian tax return.

How do donation tax receipts impact the tax filing process for Canadian donors?

Donors use their receipts to claim tax credits when they file their income tax returns.

They must save all receipts throughout the year. These receipts need to be submitted with their tax filing.

The receipts show the eligible amount that can be claimed for the tax credit. This amount may be less than the actual donation if the donor received something in return.

Charities do not send receipts directly to the CRA. Donors are responsible for keeping their receipts and providing them if needed during the tax filing process.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

.png)