Charity Application for Employment and Entrepreneurial Training

In 2025, with employment landscapes rapidly changing and workforce development more critical than ever, the Canada Revenue Agency (CRA) recognizes the vital role charities play in relieving unemployment and fostering economic self-sufficiency. If your organization wants to register as a charity to provide employment training or entrepreneurial development programs, understanding CRA's specific requirements is essential for successful approval.

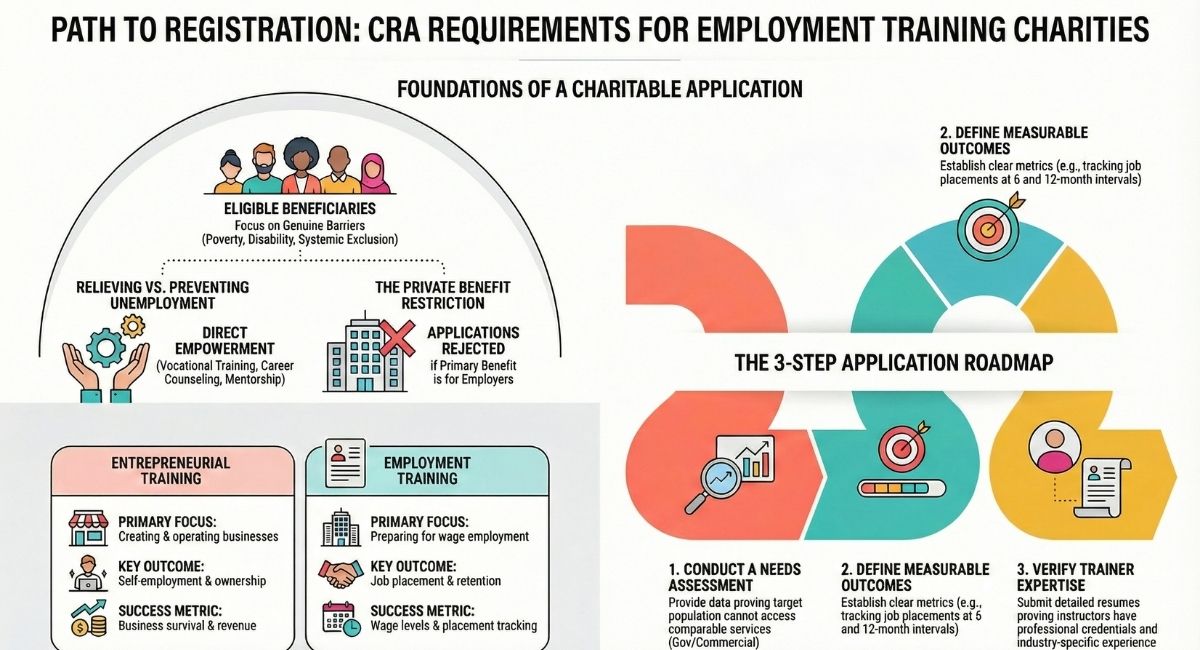

A charity applying to provide entrepreneurial and employment training can be approved by the CRA for charity registration when it demonstrates that its activities relieve unemployment, prevent poverty, or address conditions associated with disability or other disadvantages.

Why CRA Approves Employment and Entrepreneurial Training Charities

The CRA approves employment and entrepreneurial training charities because these organizations provide significant public benefit by addressing systemic economic challenges. When individuals gain meaningful employment skills or launch sustainable businesses, they reduce reliance on social assistance programs, contribute to tax revenues, and strengthen their communities economically.

These programs align with CRA's mandate to recognize charities that relieve poverty and unemployment. By helping eligible beneficiaries develop marketable skills, secure sustainable employment, or create businesses, these charities directly address one of Canada's most pressing social issues: economic exclusion.

According to Statistics Canada, unemployment and underemployment continue to affect vulnerable populations disproportionately, including newcomers, youth, persons with disabilities, and individuals facing systemic barriers. Employment training charities fill critical gaps that government programs and private sector training cannot address, particularly for those who need intensive, barrier-specific support.

What Types of Training Can Employment and Entrepreneurial Training Charities Provide?

An organization that provides entrepreneurial training can give instruction to eligible beneficiaries on various topics, such as:

- Preparing a business plan

- How to obtain financing

- Maintaining books and records

- Preparing financial statements

- Developing marketing strategies

- Understanding government regulations

- Business registration and compliance

- Market research and competitive analysis

- Customer acquisition and retention

- Digital marketing and e-commerce

Important Charitable Class Requirement: These entrepreneurial training activities are only charitable when provided to individuals who face genuine disadvantages—such as poverty, disability, or unemployment. Training provided to the general public without demonstrating beneficiary need is not charitable. CRA requires that entrepreneurial training be incidental to relieving the beneficiary's specific disadvantage (such as poverty or unemployment), not simply general business education available to anyone.

Employment training programs can include instruction on:

- Industry-specific technical skills

- Workplace communication and professionalism

- Computer literacy and digital tools

- Time management and workplace expectations

- Health and safety certification

- Trades apprenticeship preparation

- Professional certifications and licensing

Who Qualifies as an Eligible Beneficiary? Detailed Examples

Eligible beneficiaries for activities that relieve or prevent unemployment can include disabled, unemployed, or soon-to-be unemployed individuals who need assistance. However, CRA's definition of "eligible beneficiaries" extends beyond these basic categories.

Specific examples of eligible beneficiaries include:

Recent immigrants and newcomers facing credential recognition barriers, language challenges, or unfamiliarity with Canadian workplace culture and expectations.

Youth aging out of foster care or child welfare systems who lack family support networks, employment history, or workplace mentors to help them secure stable employment.

Indigenous community members seeking economic development opportunities, particularly those in remote or Northern communities with limited access to mainstream employment services.

Veterans transitioning to civilian employment who need support translating military skills to civilian job markets or addressing service-related challenges.

Individuals recovering from addiction or managing mental health challenges who face employment discrimination and need supportive, trauma-informed training environments.

Single parents returning to the workforce after extended caregiving periods who need flexible training schedules and updated skills.

Persons with disabilities requiring accommodated training environments, assistive technologies, or support workers to participate effectively.

Formerly incarcerated individuals facing significant employment barriers due to criminal records and gaps in work history.

Refugees and asylum seekers navigating complex settlement challenges while trying to achieve economic stability.

Older workers displaced by industry changes, automation, or company closures who need reskilling or career transition support.

The key requirement is demonstrating that your beneficiaries face genuine barriers to employment and that your program addresses their specific needs in a charitable manner.

Charitable Activities That Relieve Unemployment

Activities that relieve unemployment of individuals who are unemployed or facing a real prospect of imminent unemployment and are shown to need assistance may be charitable if they directly further one or more charitable purposes.

Examples of activities that relieve unemployment include:

- Providing employment-related training

- Providing career counseling

- Providing assistance with résumés or preparing for job interviews

- Establishing lists of available jobs

- Connecting beneficiaries with employment opportunities

- Offering workplace readiness programs

- Providing soft skills development

- Facilitating mentorship and job shadowing

- Offering work experience placements (when properly structured)

Helping individuals who are underemployed to get a new job can be a charitable activity when it can be shown to further a charitable purpose, such as relieving poverty or relieving conditions associated with a disability.

Important Limitation: When the emphasis is on helping employers recruit employees, this does not further a charitable purpose due to the delivery of a more than incidental private benefit to the employers. Your program must center on beneficiary needs, not employer recruitment needs.

Entrepreneurial Training vs. Employment Training: Key Differences for CRA

While both types of programs can qualify for charitable registration, CRA evaluates them differently:

Both types must demonstrate that beneficiaries genuinely need charitable assistance and couldn't access comparable training through commercial or government channels.

What CRA Looks for in Your Application

The CRA's Charities Directorate has become increasingly rigorous in evaluating employment and entrepreneurial training applications. In 2025, successful applications demonstrate not just good intentions, but concrete evidence of charitable need and structured program delivery.

CRA specifically evaluates:

Needs Assessment Documentation: You must provide evidence that your target beneficiaries face genuine barriers to employment or entrepreneurship and cannot access comparable services through existing government programs or commercial providers. This might include community surveys, labor market data, beneficiary testimonials, or partnership letters from social service agencies.

Program Outcome Measurements: CRA expects you to explain how you'll track success. Will you measure job placements? Wage levels? Business survival rates at 6 months, 12 months, 24 months? Beneficiary self-sufficiency? Having clear, measurable outcomes demonstrates accountability and charitable impact.

Follow-up and Success Tracking Methods: Describe your systems for tracking beneficiaries after program completion. How will you know if someone secured employment? Started a viable business? Maintained economic self-sufficiency? CRA wants to see long-term impact, not just program participation.

Demonstrating "Charitable Manner" Delivery: This is critical. You must show that:

- Services are genuinely free or offered at nominal cost to beneficiaries who cannot afford to pay

- Your program addresses gaps not filled by commercial or government providers

- You use qualified instructors and evidence-based curricula

- You provide wraparound supports (childcare, transportation, counseling) when needed

- You maintain confidentiality and dignity for beneficiaries

Recent CRA Guidance Updates: In recent guidance documents and Charities Directorate publications, CRA has emphasized the importance of addressing systemic barriers, trauma-informed program design, and cultural appropriateness for Indigenous beneficiaries and diverse communities. Review the latest CRA guidance on relieving unemployment available at Canada.ca.

Common Mistakes That Delay or Reject Employment Training Charity Applications

Many well-intentioned organizations submit applications that CRA cannot approve. Understanding these common errors helps you avoid delays:

1. Failing to Demonstrate Beneficiary Need

Simply stating "we help unemployed people" isn't sufficient. CRA needs evidence that your target beneficiaries cannot access comparable training elsewhere and genuinely need charitable assistance. Provide specific barriers: discrimination, disability, lack of transportation, childcare challenges, language barriers, credential recognition issues, or systemic exclusion.

2. Insufficient Trainer Qualifications Documentation

You must demonstrate that instructors have appropriate expertise. This means providing:

- Professional credentials and certifications

- Relevant work experience in the field they're teaching

- Teaching experience or pedagogical training

- Cultural competency for working with your target population

Don't just list names—provide detailed résumés or qualification summaries.

3. Vague Program Structure Descriptions

"We'll offer business training workshops" is too vague. CRA needs:

- Detailed curriculum outlines

- Session-by-session content descriptions

- Program duration and weekly schedule

- Learning outcomes for each module

- Assessment methods

- Materials and resources provided

4. Missing or Inadequate Selection Criteria

How do you determine who participates? First-come-first-served isn't a selection criterion—it's a queue. You need documented criteria showing how you identify beneficiaries who:

- Face genuine employment barriers

- Need your specific services

- Can benefit from your program

- Meet any prerequisite requirements

5. Providing Private Benefit to Employers

This is a major rejection reason. If your program's primary purpose is helping businesses recruit workers, CRA will deny registration. Red flags include:

- Employers paying for training or selecting participants

- Program curriculum designed around specific employer needs

- Guaranteed job placements with particular companies

- Training for employer-specific systems rather than transferable skills

Your focus must remain on beneficiary empowerment, not employer convenience.

6. Not Distinguishing from For-Profit Training Programs

CRA will ask: "Why should this be a charity instead of a business?" You must show:

- Your services address populations commercial training ignores

- You provide wraparound supports businesses don't offer

- You charge nothing or nominal fees versus commercial rates

- You address barriers, not just skills gaps

7. Inadequate Outcome Tracking Plans

"We hope participants find jobs" isn't an outcome tracking plan. You need:

- Specific metrics you'll collect

- How you'll collect data (surveys, interviews, follow-up calls)

- When you'll measure outcomes (immediately, 3 months, 6 months, 12 months post-program)

- How you'll use outcome data to improve programs

- Your reporting systems for the T3010 annual return

Step-by-Step: Preparing Your Employment Training Charity Application

Follow this process to prepare a comprehensive Application to Register a Charity:

Step 1: Conduct and Document Community Needs Assessment

Before designing your program, gather evidence of need:

- Review local unemployment statistics for your target population

- Survey potential beneficiaries about barriers they face

- Interview social service providers about gaps in existing services

- Analyze government and commercial training offerings to identify what's missing

- Collect letters of support from community organizations

Keep all documentation—you'll submit it with your application.

Step 2: Develop Detailed Program Curriculum and Schedule

Create comprehensive program documentation:

- Write detailed course outlines for each training module

- Develop session-by-session lesson plans

- Identify all learning materials and resources needed

- Design assessment tools to measure skill acquisition

- Create a realistic timeline showing program duration

- Plan for both group instruction and individual support

Step 3: Identify and Verify Trainer Qualifications

Recruit qualified instructors and document their expertise:

- Collect detailed résumés showing relevant credentials and experience

- Verify professional certifications and licenses

- Document teaching experience or provide training plans for new instructors

- Ensure instructors have appropriate police record checks

- Consider cultural competency training for instructors

Step 4: Create Beneficiary Selection Criteria and Intake Process

Design a fair, transparent selection system:

- Write clear eligibility criteria based on barriers and need

- Develop an intake application form

- Create an assessment process to evaluate beneficiary needs

- Plan for waitlist management if program is oversubscribed

- Document how you'll verify unemployment or underemployment status

- Design a confidential record-keeping system

Step 5: Design Outcome Measurement Tools

Build accountability into your program:

- Identify key performance indicators (job placement rates, wage levels, business survival, beneficiary satisfaction)

- Create tracking forms for collecting outcome data

- Design follow-up surveys for 3, 6, and 12 months post-program

- Plan how you'll maintain contact with program graduates

- Develop reporting templates for your board and CRA

Step 6: Prepare Budget and Sustainability Plan

Demonstrate financial viability:

- Create a detailed first-year budget showing all program costs

- Identify revenue sources (donations, grants, related business income, nominal participant fees)

- Show three-year financial projections

- Explain your fundraising strategy

- Demonstrate you can deliver programs sustainably

Important Note on Related Business: If your charity plans to generate revenue through business activities, these must qualify as a "related business" under CRA rules. A related business is one that is operated substantially by volunteers, or is linked to the charity's purposes and subordinate to those purposes. If your organization operates an unrelated business (one that doesn't meet these criteria), it must be run through a separate taxable corporation, not directly by the charity. Simply calling an activity a "social enterprise" does not automatically make it a permissible related business.

For example, if your employment training charity operates a café staffed by program participants as hands-on training, this could be a related business. However, if you operate a commercial café simply to raise funds without connection to your training programs, this would be an unrelated business requiring a separate corporate structure.

Step 7: Complete the Application to Register a Charity

Access the application through the CRA's Charities Directorate website:

- Complete all sections thoroughly and accurately

- Use clear, specific language in your purposes and activities descriptions

- Attach all required supporting documents

- Include your needs assessment documentation

- Submit comprehensive program descriptions

- Provide detailed trainer qualifications

- Include your selection criteria and intake process

- Attach budget and sustainability plans

Step 8: Submit Supporting Documentation

Ensure you include:

- Organizing documents (letters patent, articles of incorporation, trust deed)

- Detailed program curricula

- Trainer qualifications

- Needs assessment documentation

- Financial projections

- Letters of support from community partners

- Board member information

- Any additional materials that strengthen your application

Allow 6-12 months for CRA review. Respond promptly to any CRA questions or requests for additional information.

After Registration: Ongoing Compliance for Employment Training Charities

Registration is just the beginning. Maintaining your charitable status requires ongoing compliance:

Annual T3010 Return Requirements

Every registered charity must file an annual information return (Form T3010). For employment training charities, you'll report:

- Number of beneficiaries served

- Program outcomes and success rates

- Detailed description of activities

- Financial statements showing revenue and expenses

- Compensation for employees and contractors

- Fundraising activities and costs

Documentation Retention Requirements

CRA requires you to maintain complete records for seven years:

- Beneficiary intake forms and selection documentation

- Program attendance records

- Outcome tracking data

- Financial records (receipts, bank statements, invoices)

- Board meeting minutes

- Donation receipts and acknowledgments

- Employment contracts and contractor agreements

Tracking and Reporting Beneficiary Outcomes

Maintain systems to demonstrate charitable impact:

- Regular follow-up with program participants

- Database tracking employment placements and business startups

- Success stories and testimonials (with permission)

- Challenges faced and program adjustments made

- Comparison of outcomes year-over-year

When to Notify CRA of Program Changes

You must inform CRA of significant changes:

- Adding new programs or activities

- Changing your purposes

- Expanding to new geographic areas

- Altering your governance structure

- Changing your legal name

- Relocating your operations

File amended governing documents or notify the Charities Directorate in writing.

Best Practices for Maintaining Charitable Status

Protect your registration by:

- Keeping meticulous records

- Ensuring all activities align with your registered purposes

- Engaging in non-partisan public policy dialogue and development activities (PPDDAs) that further your charitable purposes

- Preventing private benefit to individuals or businesses

- Maintaining qualified board governance

- Filing your T3010 on time every year

- Responding promptly to CRA correspondence

- Conducting regular internal compliance reviews

Important Update on Political Activities: As of 2018, registered charities in Canada can engage in unlimited public policy dialogue and development activities (PPDDAs), provided these activities are non-partisan and further the charity's purposes. The previous "10% rule" limiting political activities no longer applies. Your charity can advocate for policy changes, conduct public education campaigns, and engage with government on issues related to employment and entrepreneurial training, as long as these activities support your charitable mission and remain non-partisan (not supporting or opposing political parties or candidates).

Real-World Examples of CRA-Approved Employment Training Charities

Understanding how similar organizations successfully gained approval can guide your application:

Example 1: Youth Entrepreneurship Program (Ontario)

A Toronto-based charity serves youth aged 16-24 from low-income neighborhoods, focusing on those not in education, employment, or training (NEET). Their program provides 12-week intensive training in business planning, financial management, digital marketing, and sales skills.

What made them successful:

- Detailed needs assessment showing youth unemployment rates 3x higher in target neighborhoods

- Partnership letters from youth shelters, settlement agencies, and community centers

- Comprehensive curriculum with weekly modules clearly described

- Instructor résumés showing business ownership experience plus youth work credentials

- Outcome tracking showing 68% of participants launched businesses or secured employment within 6 months

- Wraparound supports including TTC tokens, lunch, childcare referrals, and mentorship

- Clear demonstration that program served beneficiaries who couldn't afford commercial entrepreneurship courses ($3,000-$5,000) or didn't meet eligibility criteria for government youth employment programs

Example 2: Newcomer Employment Services (British Columbia)

A Vancouver charity provides employment training for immigrants and refugees with professional credentials not recognized in Canada. Programs include credential bridging, Canadian workplace culture training, and sector-specific job search skills.

What made them successful:

- Statistics showing 40% of newcomers in Metro Vancouver work in jobs below their qualification level

- Partnerships with regulatory bodies and industry associations

- Culturally appropriate program delivery in multiple languages

- Instructors with immigration experience plus professional credentials in sectors they teach (nursing, engineering, accounting, IT)

- Success tracking showing average wage increase of $18,000 annually for participants who completed program

- Documentation showing similar commercial programs cost $8,000-$15,000, making them inaccessible to target population

- Letters from settlement agencies confirming gaps in government-funded services

Example 3: Indigenous Economic Development Training (Prairie Provinces)

A Saskatchewan-based charity operates on-reserve and in Northern communities, providing entrepreneurship training tailored to Indigenous cultural contexts and remote community challenges.

What made them successful:

- Community needs assessments conducted by Indigenous researchers

- Curriculum incorporating traditional knowledge alongside business skills

- Elders and community leaders involved in program design and delivery

- Instructors with Indigenous business experience and cultural competency

- Program delivery adapted to community schedules (seasonal work, cultural events, land-based activities)

- Outcome tracking showing business creation rates and community economic impact

- Documentation showing commercial training providers don't operate in remote communities and government programs don't address cultural barriers

- Strong community support letters from band councils and Indigenous organizations

Example 4: Women's Entrepreneurship Initiative (National)

A Canada-wide charity serves women escaping domestic violence, single mothers on social assistance, and women with disabilities, providing business training and microloans.

What made them successful:

- Compelling statistics on poverty rates for single mothers and women with disabilities

- Trauma-informed program design with mental health support integrated

- Flexible delivery (online, evening, weekend options) accommodating childcare and disability needs

- Instructors with entrepreneurship experience plus training in working with trauma survivors

- Wraparound supports: childcare subsidies, transportation assistance, peer mentoring, counseling referrals

- Outcome tracking showing 73% of participants achieved economic self-sufficiency, reducing social assistance reliance

- Microloan program structured as charitable activity (below-market interest, extensive support, focus on borrower success)

- Clear demonstration that commercial lenders won't serve this population and government programs don't provide intensive, individualized support

These examples share common success factors: clear beneficiary need, qualified instructors, comprehensive curricula, measurable outcomes, and demonstration that the charitable program fills gaps commercial and government providers cannot address.

Need Help With Your Charity Application?

Preparing a comprehensive Application to Register a Charity for employment or entrepreneurial training requires detailed documentation and thorough understanding of CRA's requirements. The charity lawyers at B.I.G. Charity Law Group have extensive experience helping organizations successfully navigate the registration process.

Book a Free Consultation to discuss your employment training charity application and ensure you meet all CRA requirements for approval.

Frequently Asked Questions

1. Can we charge fees for our employment training programs?

Yes, but fees must be nominal and not create barriers for your target beneficiaries. If your purpose is relieving poverty or unemployment, charging market-rate fees contradicts your charitable purpose. Many successful charities use a sliding scale, offer subsidies, or charge nothing. If you charge fees, explain in your application why they're necessary and how you ensure they don't exclude those in need.

2. Do we need professional trainers or can we use volunteers?

Both are acceptable, but you must demonstrate that instructors—whether paid staff or volunteers—have appropriate qualifications. For employment training, this means relevant work experience in the field being taught. For entrepreneurial training, this means business ownership or management experience. Teaching skills or training in adult education strengthens applications. Provide detailed qualifications for all instructors.

3. How do we prove someone is "unemployed" or "underemployed"?

Develop an intake process that collects documentation such as: termination letters, Record of Employment (ROE), EI statements, pay stubs showing wages below poverty line for their household size, or professional credential documents showing overqualification for current employment. Self-declaration can be sufficient if you have a verification process and document beneficiary circumstances in your files.

4. Can we partner with employers to place graduates?

Yes, job placement partnerships are excellent—but structure them carefully. The employer cannot pay you for recruitment services, select participants, or control curriculum. Your focus must be beneficiary empowerment, not employer convenience. Best practice: develop general job placement relationships with multiple employers, ensure placements match beneficiary interests and skills, and never guarantee specific placements to employers.

5. What's the difference between job placement and relieving unemployment?

Relieving unemployment focuses on empowering beneficiaries with skills, confidence, and resources to secure employment. Job placement is a potential outcome but not the primary activity. If your main activity is matching people to jobs (employment agency function), this isn't charitable. If your main activity is training, counseling, and supporting beneficiaries to overcome employment barriers, with job placement as one component, this can be charitable.

Legal Sources & References

- Income Tax Act, R.S.C. 1985, c. 1 (5th Supp.) s. 118.1

- Succession Law Reform Act, R.S.O. 1990, c. S.26

- CRA Policy Statement CPS-019, What is a related business?

- CRA Guidance CG-027, Public policy dialogue and development activities by registered charities

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

.png)