What Is an Endowment Fund? A Guide for Canadian Charities and Donors

Published on

March 23, 2026

Last updated on

July 26, 2026

What Does "Endowment" Mean for a Canadian Charity?

For Canadian charities and donors alike, understanding what an endowment fund is can open the door to smarter, more sustainable giving. This section breaks down the core concept in plain language before getting into the details.

An endowment fund is one of the most powerful tools available for building long-term charitable impact. Rather than spending a donation immediately on programs or operations, the charity invests the gift and uses only the earnings to fund its work — year after year, sometimes indefinitely.

A useful way to think about it: an endowment is a "savings account for a cause." The original gift stays intact. The interest, dividends, or investment returns it generates are what the charity actually spends.

The word "endowment" does not have a strict legal definition under Canadian statute. However, it is a well-established practice governed by trust law and CRA regulations, and it appears frequently in the governance documents of universities, hospitals, community foundations, and registered charities of all sizes.

This guide is written for:

- Donors considering a legacy gift or planned giving strategy

- Charity board members evaluating long-term financial planning

- Charity and NPO administrators who want to understand how endowments interact with CRA compliance

Note: Only Registered Charities can issue official donation tax receipts and hold charitable endowments in the manner described in this guide. Non-profit organizations (NPOs) operating under s. 149(1)(l) of the Income Tax Act are not registered charities and cannot issue donation receipts for the tax credits described below.

How Does a Charity Endowment Fund Work?

Before exploring the different types of endowments, it helps to understand the three core mechanics that apply to almost every endowment arrangement in Canada: the principal, the payout, and the disbursement quota.

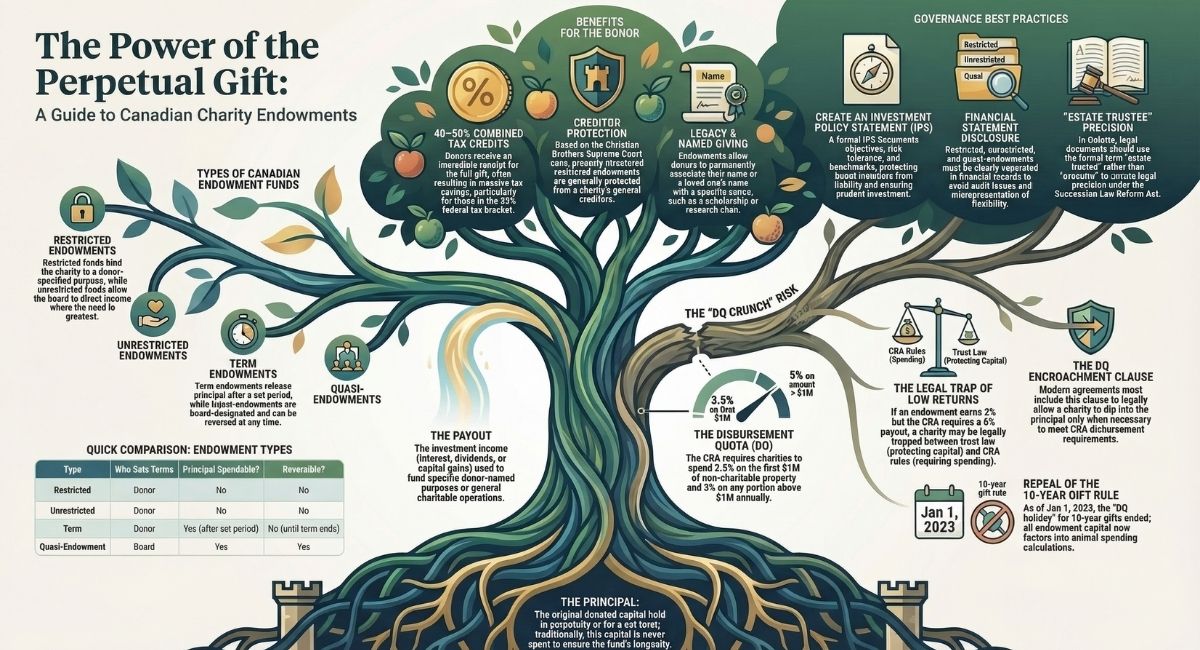

The Principal

The principal is the original donated capital — the amount the donor contributes to establish the fund. In a traditional endowment, the principal is held in perpetuity, meaning it is never spent. Only the investment income it generates is available for the charity to use.

Some modern agreements allow for what is called a "term endowment," where the principal is held for a defined number of years before it can be spent. The donor's stated intent and the legal agreement between the donor and the charity govern how the principal is treated.

This distinction matters because it affects the charity's long-term financial planning, its obligations under trust law, and how the fund is reported on financial statements.

The Payout

The payout refers to the investment income — interest, dividends, or capital gains — that the charity draws on to fund its mission. Depending on the terms of the endowment agreement, that income may be:

- Directed toward a specific purpose the donor has named (such as cancer research or youth scholarships)

- Left to the board's discretion to direct where the need is greatest

- Partially reinvested to grow the fund over time before distributions begin

The payout structure is one of the most important elements of any endowment agreement and should be drafted carefully to reflect both the donor's goals and the charity's operational realities.

The Disbursement Quota (DQ)

The CRA requires all registered charities to spend a minimum amount each year on charitable activities and gifts to qualified donees. This is called the disbursement quota (DQ).

The DQ applies differently depending on the type of registered charity:

- Charitable organizations must meet the DQ if the average value of property not used directly in charitable activities or administration exceeds $100,000.

- Public and private foundations must meet the DQ if that property exceeds $25,000.

When the DQ applies, the rates are:

- 3.5% on the first $1 million of property not used directly in charitable activities or administration

- 5% on any portion of that property above $1 million

Investment income and assets held in an endowment fund count as charitable property. This means charities managing large endowments must plan their distributions carefully to ensure they meet or exceed the DQ threshold each year — or they risk CRA non-compliance.

Warning: The "DQ Crunch" and Why Every Endowment Agreement Needs a Capital Encroachment Clause

There is a legal trap that many charities do not discover until it is too late — and the abolition of the 10-year gift exemption has made it significantly more dangerous.

Here is the problem: A traditional restricted endowment agreement forbids the charity from spending the principal. But the CRA can require a payout of up to 5% of charitable property annually under the disbursement quota. If markets perform poorly and the endowment only earns 2% in a given year, the charity faces an impossible conflict — the CRA demands a 5% distribution, but the trust agreement legally prohibits touching the capital.

This is known as a "DQ crunch," and it can put a charity in breach of its trust obligations, its donor agreement, or its CRA compliance requirements — sometimes all three at once.

The solution: A DQ Encroachment Clause

All new endowment agreements should include a DQ Encroachment Clause. This is a specific provision that legally permits the charity to dip into the principal — but only to the extent necessary to meet its annual CRA disbursement quota obligations. The clause is carefully limited so it cannot be used as a general licence to spend down the endowment; it applies only when investment income falls short of the required DQ threshold.

Including this clause protects the charity from being trapped between two conflicting legal obligations and gives the board a clear, documented basis for any principal encroachment without breaching the donor's intent.

Any charity accepting a restricted endowment gift should have this clause reviewed and confirmed by a charity law lawyer before the agreement is signed.

Types of Charity Endowment Funds in Canada

The type of endowment a charity holds determines who controls the funds, how the income must be used, and whether the principal can ever be accessed. There are four main types, each with distinct legal and governance implications.

The table below provides a quick comparison before each type is explored in detail.

Restricted Endowments

A restricted endowment is the most common type established by external donors. The donor specifies — in writing, in the endowment agreement — exactly how the income from the fund must be used. The charity is legally bound to honour those terms under trust law, and that obligation does not expire.

Common examples of restricted endowments include:

- A named scholarship at a college or university (e.g., "The [Family Name] Award for Excellence in Engineering")

- A research chair at a teaching hospital, funded specifically for cancer or cardiac research

- An environmental conservation fund that can only support land acquisition or habitat restoration

- A faith-based fund restricted to supporting youth programming at a specific institution

Why it matters legally: Once a restricted endowment is established, the charity cannot redirect the income — even if the original purpose becomes difficult to fulfill. If circumstances change significantly (for example, the named program no longer exists), the charity may need to apply to a court or the provincial Attorney General's office to vary the terms. In Ontario, this process falls under the Charities Accounting Act and cy-près doctrine.

Why donors choose it: Restricted endowments give donors the highest level of confidence that their gift will be used exactly as they intended — not just now, but permanently. For donors making significant planned gifts or memorial contributions, that certainty is often essential.

Unrestricted Endowments

An unrestricted endowment is established by a donor who wants the principal preserved permanently but is comfortable giving the charity's board full discretion over how the income is used each year. There are no donor-imposed conditions on the income.

This flexibility is particularly valuable for charities whose needs shift over time. A social services organization, for example, may find that the most pressing need changes from year to year — from emergency housing one year to mental health programming the next. An unrestricted endowment allows the board to respond without being constrained by terms set decades earlier.

Key points about unrestricted endowments:

- The board still has fiduciary obligations and cannot use the income frivolously

- Investment decisions must comply with the prudent investor standard

- The fund should be disclosed clearly in financial statements as an endowment, separate from general reserves

- Donors receive the same tax receipt and benefits as with a restricted endowment

Unrestricted endowments are a strong option for donors who trust the organization's leadership and want their gift to serve the charity's evolving mission rather than a fixed purpose.

Term Endowments

A term endowment differs from a traditional endowment in one key way: the principal is not held forever. Instead, the donor and charity agree that the principal will be preserved for a specific period — for example, 10, 20, or 25 years — or until a defined event occurs (such as the completion of a building campaign or the passing of a named individual). After that point, the charity can spend both the income and the principal.

Term endowments are commonly used in:

- Estate planning: A donor may want their gift to generate income for a cause during the remaining life of a surviving spouse, with the principal released to the charity afterward.

- Capital campaigns: An organization might accept a term endowment to build financial reserves before a major facility expansion.

- Planned giving: Donors who want to make a significant future impact but also want the assurance that the full gift will eventually be deployed may prefer a term structure.

From the charity's perspective, a term endowment requires careful record-keeping and communication with successors on the board who may not have been present when the agreement was signed. The terms should be clearly documented and reviewed regularly as part of good governance practice.

Note on terminology: In Ontario, the correct legal term for the person who administers an estate is "estate trustee," as established under the Succession Law Reform Act. The term "executor" is widely understood but is not the formal Ontario designation. All endowment or planned gift agreements referencing estate administration in Ontario should use "estate trustee" to ensure legal precision.

Quasi-Endowments (Board-Designated Funds)

A quasi-endowment — sometimes called a board-designated endowment — is created not by a donor, but by the charity's own board of directors. The board sets aside a portion of the charity's unrestricted funds and resolves to treat them like an endowment, investing them for long-term income generation.

Because no donor restrictions are involved, the board can reverse this decision at any time by passing a new resolution. This makes quasi-endowments significantly more flexible than true endowments — but also less permanent.

Important characteristics of quasi-endowments:

- They are fully controlled by the board — no trust law restrictions apply from a donor perspective

- They can be unwound if the charity faces a financial crisis or strategic shift

- They must be clearly distinguished from donor-restricted endowments on financial statements

- They are a sign of strong financial governance — charities that build quasi-endowments are planning proactively for long-term stability

Quasi-endowments are often a practical starting point for smaller charities that want to build an endowment culture before launching a formal donor-facing endowment program.

Benefits of Contributing to a Charity Endowment Fund in Canada

Endowments are not just good for charities — they offer significant advantages for donors as well. From tax planning to legacy building, here is why many Canadians choose endowments as part of their charitable giving strategy.

Immediate Tax Credits

One of the most important advantages for donors is the timing of the tax receipt. A donor receives a charitable donation receipt for the full amount of the gift in the year it is made — even if the principal will not be spent by the charity for decades.

For individual Canadians, this translates into:

- A federal charitable donation tax credit of 29% on amounts over $200 — or 33% for individuals whose taxable income exceeds the highest federal tax bracket (over $246,752 in 2025)

- A provincial charitable donation tax credit (varies by province)

- Combined federal-provincial credits that can return 40–50 cents on the dollar, depending on the province and income level

The 33% federal credit tier is particularly relevant for endowment giving, which often attracts high-net-worth donors making significant planned or legacy gifts.

For corporations, the donation is treated as a deductible expense, reducing taxable income in the year the gift is made.

This front-loaded tax benefit makes endowments especially attractive in years when a donor has unusually high income — such as the year of a business sale, a large capital gain, or a significant inheritance.

Important: The Alternative Minimum Tax (AMT) and Large Endowment Gifts

High-net-worth donors planning significant endowment contributions — particularly those donating publicly listed securities — should be aware of changes to the federal Alternative Minimum Tax (AMT) that took effect in 2024.

The 2024 AMT reforms expanded the scope of the tax for high-income earners and placed new limitations on the amount of charitable donation tax credits that can be used to reduce AMT liability in a given year. For donors making very large endowment gifts, this could affect the timing of the contribution, the vehicle used to fund the endowment, or the overall tax outcome — even when the gift appears straightforward on paper.

This does not mean donors should avoid large endowment gifts. It means the timing and structure of the gift requires careful planning in advance.

Before making a significant endowment contribution, high-net-worth donors should consult both a qualified tax accountant and a charity law lawyer to model the full tax impact under current AMT rules and identify the most advantageous approach.

Legacy and Named Giving

Endowments give donors the opportunity to permanently associate their name — or the name of a loved one — with a cause they care about. This is a defining feature of endowment giving that separates it from most other forms of charitable contribution.

Named endowment funds are common in:

- Memorial giving (honouring a deceased family member)

- Estate planning (ensuring a name lives on through a charitable purpose)

- Institutional philanthropy at universities, hospitals, and arts organizations

- Faith communities establishing legacy funds within their institutions

For many donors, the permanence of a named endowment is more meaningful than the tax benefit. It is a way of ensuring that their values outlast their lifetime.

Creditor Protection: A Critical Benefit for Major Donors

One of the most compelling but least discussed benefits of a properly structured restricted endowment is the protection it can offer against a charity's future creditors.

Under Canadian trust law, a restricted endowment is held as a special purpose trust — meaning those funds exist for a defined charitable purpose and are legally separate from the charity's general operating assets. In the landmark Supreme Court of Canada decision Christian Brothers of Ireland in Canada (Re), 2000 SCC 21, the Court affirmed that trust assets held for a specific purpose are generally not available to satisfy the claims of an organization's general creditors in the event of insolvency or bankruptcy.

For high-net-worth donors making major endowment gifts, this is a significant assurance. If a charity faces a catastrophic lawsuit, financial collapse, or insolvency years after the gift is made, a properly drafted restricted endowment can remain protected and continue to serve its intended charitable purpose — rather than being swept into a general creditor pool.

This protection is not automatic. It depends on the endowment being:

- Properly documented as a restricted trust in the gift agreement

- Clearly segregated in the charity's financial records

- Managed consistently with the terms of the trust

Donors who are motivated by permanence — particularly those making legacy or planned gifts — should ensure their endowment agreement is drafted with these protections explicitly in place. A charity law lawyer can confirm whether the proposed agreement structure would qualify for this level of protection under applicable trust law.

Strategic Giving Through Donor-Advised Funds (DAFs)

Not every donor who wants to establish an endowment-style fund wants to go through the process of creating a private foundation or negotiating a formal agreement with a charity. Donor-Advised Funds (DAFs) offered through community foundations provide a simpler, more flexible alternative.

With a DAF, a donor:

- Contributes a lump sum to the community foundation and receives an immediate tax receipt

- Recommends how those funds are invested and granted out over time

- Can direct grants to any registered Canadian charity — including existing endowment programs

- Avoids the administrative, legal, and reporting burden of running a private foundation

DAFs are especially useful for donors who want to take a strategic, multi-year approach to giving without locking into a single cause or organization at the time of the initial contribution.

What Is the 10-Year Gift Rule for Canadian Charity Endowments?

The "10-year gift rule" is a term that still surfaces in endowment discussions, and it is worth clarifying — particularly because outdated information about it continues to circulate online.

Historically, CRA rules allowed donors to designate a gift to be held for at least 10 years, which exempted the receiving charity from including that capital in its disbursement quota calculation.

This was designed to give charities time to build endowment assets without immediately triggering spending obligations — a period sometimes called a "DQ holiday."

This exemption was effectively repealed for tax years beginning on or after January 1, 2023. Under the current Income Tax Act framework, all property — including amounts previously designated as 10-year gifts — is now included in the average value of property used to calculate the annual DQ.

A donor can still direct a 10-year hold on the principal as a matter of trust law, but that arrangement no longer shields the charity from its DQ obligations on that capital under the ITA.

In practical terms, this means charities accepting large endowment gifts should no longer rely on 10-year gift designations as a tool for managing their DQ exposure.

Proper financial planning, including annual DQ projections, is now essential from the moment the gift is received.

That said, most well-drafted endowment agreements still include capital preservation language as a best practice — not for DQ purposes, but because:

- It protects the donor's intent from being undermined by future board decisions

- It helps the charity demonstrate to CRA that the fund is genuinely endowed, not simply a restricted operating reserve

- It reduces the risk of governance disputes between the board and donor families

Both donors and charities are strongly advised to have endowment agreements reviewed by a charity law lawyer to ensure the language reflects current CRA rules and properly protects all parties.

Legal and Governance Considerations for Canadian Charities Managing Endowments

Managing an endowment fund is not just a financial responsibility — it is a legal one. Charities that accept endowment contributions take on obligations that may persist for decades or longer.

Here are the key legal and governance considerations every charity should understand before establishing or accepting an endowment:

- Trust law obligations: Once a restricted endowment is established, the charity holds those assets in trust for the stated purpose. This is a binding obligation. Courts and provincial Attorneys General have authority to intervene if a charity misuses restricted funds or fails to honour the donor's intent.

- Prudent investor standard: The board has a fiduciary duty to invest endowment assets responsibly. Most charities with significant endowments develop a formal Investment Policy Statement (IPS) that documents the investment objectives, risk tolerance, asset allocation, and benchmarks for the fund.

- Investment Policy Statements (IPS): An IPS is considered best practice for any charity managing an endowment. It provides a clear framework for investment decisions, protects board members from personal liability, and demonstrates good governance to CRA, auditors, and donors.

- Provincial variation: Endowment governance is not uniform across Canada. In Ontario, the Charities Accounting Act and related case law govern how charities hold and manage charitable property. Other provinces have their own frameworks, and charities operating nationally should understand the rules in each relevant jurisdiction.

- CRA compliance: Endowment income factors into the annual disbursement quota calculation. Charities that consistently fall short of their DQ — even due to strong investment performance — may attract CRA scrutiny or face compliance requirements.

- Financial reporting: Restricted endowments, unrestricted endowments, term endowments, and quasi-endowments must each be disclosed appropriately on financial statements, typically as separate net asset categories. Mixing these categories can create audit issues and misrepresent the charity's actual financial flexibility.

Charities managing significant endowments should work closely with both a charity law lawyer and a qualified charity accountant to establish proper systems from the outset.

Get Legal Advice On Charity Endowment Agreements

Setting up an endowment requires careful legal planning. A charity should work with qualified legal counsel before accepting or creating any endowment agreement.

Why Legal Advice Matters

Endowment agreements are binding legal contracts. These documents outline how a donor's gift will be managed and spent over time.

Without proper legal review, a charity might agree to terms it cannot fulfill or face unexpected restrictions. The words used in a gift agreement must reflect what the donor actually wants.

Poor wording can create a permanent endowment when neither party intended that outcome. It can also create confusion about spending rules or charitable purposes.

Key Areas That Need Review

Legal counsel should review several important aspects:

- How and when the charity can spend the gift

- What restrictions apply to the use of funds

- Whether the endowment is permanent or temporary

- Reporting requirements to donors

- Investment and management obligations

Both the charity and donor benefit from getting legal advice early in the process. The charity needs to ensure it can carry out any restrictions or reporting specified in the agreement.

The donor needs to know their wishes will be honoured as intended.

Who Should Provide Legal Advice

Each charity should have their legal counsel review any endowment agreement before board approval. Tax advisors may also need to provide input on the tax treatment of the gift.

Clear legal documentation protects everyone involved. It ensures the endowment serves its intended charitable purpose for years to come.

Conclusion

Endowment funds offer Canadian charities a reliable way to secure their financial future. These funds provide steady income by investing the principal and using only a portion of the returns for charitable work.

Whether a charity chooses an unrestricted, restricted, or quasi-endowment structure depends on its needs and donor preferences. Setting up an endowment requires careful planning and proper legal documentation.

Charities must understand the rules around endowment management, including spending policies, investment strategies, and reporting obligations. Donors benefit from tax advantages while supporting causes they care about for generations to come.

At B.I.G. Charity Law Group, we help Canadian charities and donors navigate the legal aspects of endowment funds. We provide guidance on fund structures, gift agreements, compliance requirements, and tax planning strategies.

If you are a charity or donor looking to explore your options, we invite you to contact us at dov.goldberg@charitylawgroup.ca or call 416-488-5888 to discuss your endowment needs. ‘

You can also visit our website for more information or schedule a free consultation to explore how an endowment fund might work for your situation.

Frequently Asked Questions About Charity Endowments in Canada

How does an endowment fund benefit a Canadian charity?

An endowment fund provides a charity with a steady source of income year after year. The charity invests the donated money and uses only a portion each year for programs and operations.

The rest stays invested to grow over time. This structure helps charities plan for the future with more confidence.

They can count on regular funding rather than relying only on annual donations. The investment income supports programs without requiring the charity to spend down the original gift.

Endowments also help small charities access better investment opportunities. Many place their endowment funds within community foundations to benefit from professional management and diversification.

Is an endowment fund the same as a reserve fund?

No. A reserve fund is board-controlled and can be accessed at the board's discretion for any approved purpose. A restricted endowment is governed by donor-imposed terms that are enforceable under trust law — the board cannot redirect the income without legal authority to do so.

Can a Canadian charity spend the principal of an endowment?

It depends entirely on the terms of the agreement. A traditional restricted or unrestricted endowment preserves the principal in perpetuity. A term endowment allows the principal to be spent after a defined period or event. A quasi-endowment can be unwound by the board at any time through a board resolution.

Do endowment funds count toward the disbursement quota?

Yes. Investment income earned by endowment assets is treated as property of the charity and factors into the annual DQ calculation. Charities with large endowments generating significant income need to plan carefully to ensure they distribute enough each year to remain compliant.

What is the minimum size for a charity endowment fund in Canada?

There is no legal minimum under CRA rules. However, many community foundations set practical minimums for named endowment funds — typically in the range of $10,000 to $25,000 — to ensure the fund is large enough to generate meaningful income after investment management costs.

Do I need a lawyer to set up a charity endowment?

It is not a legal requirement, but it is strongly recommended. Endowment agreements are binding legal documents with long-term obligations. A poorly drafted agreement can create compliance problems for the charity, fail to protect the donor's intent, or generate costly disputes years down the road.

Can a charity refuse an endowment gift?

Yes. Charities are not obligated to accept every gift offered. Some endowments come with terms that are impractical for the charity to honour — for example, a restriction tied to a program the charity has since discontinued. Charities have the right to negotiate terms or decline gifts that create more burden than benefit.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)