Donor Advised Funds: How They Work and What Canadian Charities Need to Know

Published on

March 2, 2026

Last updated on

March 2, 2026

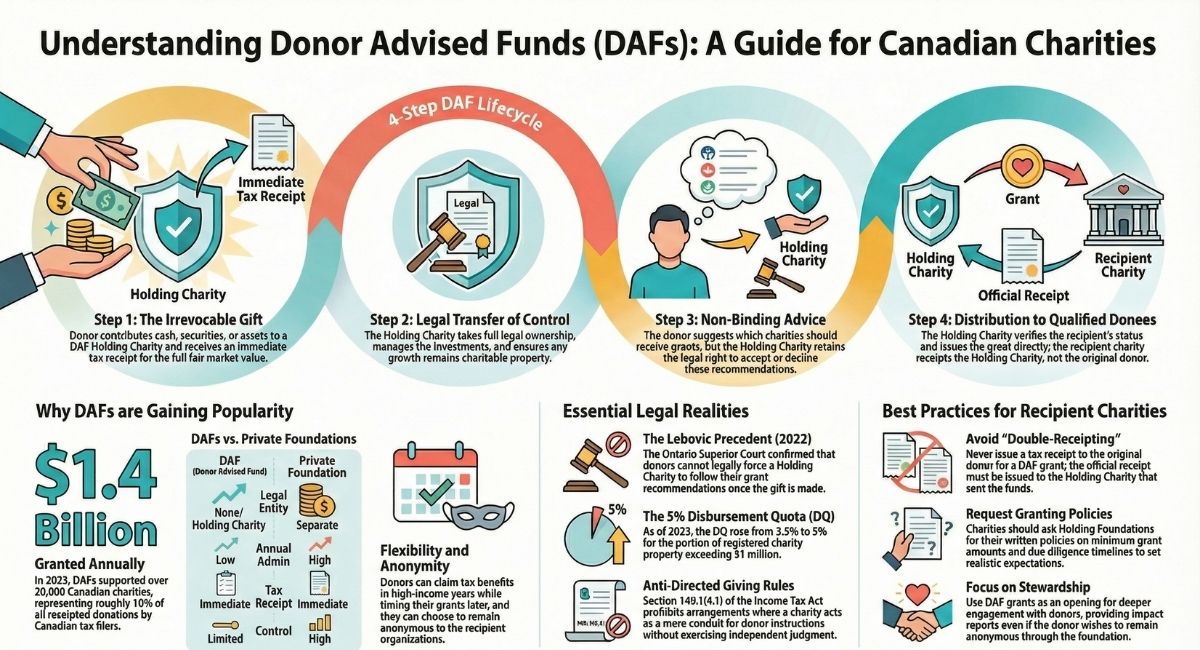

Donor-advised funds granted over $1.4 billion to more than 20,000 Canadian charities in 2023. Many organizations still don't fully understand how they work or how to engage with DAF donors effectively.

These funds have become one of the fastest-growing vehicles for charitable giving in Canada over the past two decades. Despite their popularity, confusion remains about the legal structure, governance, and practical implications for charities that receive DAF grants.

Understanding how donor-advised funds operate and the legal framework that governs them helps charities build stronger relationships with donors. The Canadian DAF landscape differs from the American model in important ways, with unique legal considerations that charities must address.

From the landmark Lebovic court decision to ongoing regulatory questions, Canadian organizations need clear guidance on managing these funds.

This article explains what donor-advised funds are and how they function within Canada's charitable sector. It also covers legal and practical issues charities should consider.

The article examines key court rulings and provides guidance for organizations that administer DAFs or receive grants from them.

What Is a Donor Advised Fund (DAF)?

A donor-advised fund is a charitable giving account that allows donors to contribute money or assets and receive an immediate tax receipt. Donors can then recommend grants to Canadian registered charities over time.

The fund is held and managed by a DAF Holding Charity, which legally owns the assets once the donor makes the contribution.

The CRA's Definition of a DAF

The Canada Revenue Agency defines a donor-advised fund as an arrangement where a donor makes an irrevocable contribution to a qualified donee. The donor retains advisory privileges over how the funds are distributed.

The donor can recommend which charities receive grants, but the DAF Holding Charity holds the legal authority to approve or decline those recommendations.

This structure means the donation is final once made. The donor cannot take the money back or use it for personal benefit.

The DAF Holding Charity must be a registered charity or public foundation under Canadian law. The CRA requires that the DAF Holding Charity maintains control over the funds and ensures all grants go to qualified donees.

This distinguishes a DAF from a simple gift where the charity has full discretion.

How a DAF Differs from a Private Foundation

Private foundations and donor-advised funds both enable structured charitable giving, but they operate differently. A private foundation is a separate legal entity that requires its own charitable registration, board of directors, and annual tax filings with the CRA.

Setting up a private foundation involves legal fees, accounting costs, and ongoing administrative work. A DAF offers similar benefits without the complexity.

The DAF Holding Charity handles all administrative tasks, compliance requirements, and tax filings. Donors can open a DAF quickly without establishing a separate legal structure.

Private foundations face a disbursement quota and must grant a minimum percentage of their assets annually. DAFs typically don't have the same strict requirements, though many DAF Holding Charity encourage regular granting.

Who Can Open a DAF?

Individuals, families, and businesses can all open donor-advised funds in Canada. Some DAF Holding Charity set minimum initial contribution amounts, which can range from $10,000 to $25,000 depending on the institution.

Other organizations accept lower amounts to make DAFs accessible to more donors. Community foundations, public foundations, and financial institutions offer DAF programs.

Each DAF Holding Charity sets its own eligibility requirements, fees, and investment options. Multiple people can be named as advisors on a single DAF account.

This allows families to involve children in charitable decisions or enables business partners to collaborate on corporate giving strategies.

How Does a Donor-Advised Fund Work in Canada?

A donor-advised fund operates through four steps involving the donor, the DAF Holding Charity, and the recipient charities. The process begins when someone makes an irrevocable donation and ends when grants flow to Canadian charities and other qualified donees.

Step 1 — The Donor Makes an Irrevocable Gift

The donor contributes cash, securities, or other assets to a DAF holding charity such as the Aqueduct Foundation, Benefaction Foundation, or TD Private Giving Foundation. This contribution is permanent and cannot be reversed.

The donor receives an immediate tax receipt for the full value of the gift. They can claim the charitable donation tax credit in the year they make the contribution, even if they haven't decided which charities to support yet.

Many community foundations and other DAF Holding Charities accept a wide range of assets, including publicly traded securities, real estate, or business interests. The foundation handles the administrative work of processing and managing these assets.

Step 2 — The DAF Holding Charity Takes Full Control

Once the donation is complete, the DAF Holding Charity owns and controls the funds legally. The donor no longer has any legal ownership over the contributed assets.

The foundation invests the funds according to its investment policies. Any growth in the fund's value remains charitable property and can be used for future grants to Canadian charities.

These foundations are registered charities that must follow Canada Revenue Agency rules and conduct their own charitable activities.

Step 3 — The Donor Provides Non-Binding Advice

The donor can recommend which charities should receive grants from their fund. They submit these recommendations to the DAF Holding Charity for review.

These recommendations are advisory only. The foundation has the legal authority to accept or reject any suggested grant.

In practice, most foundations approve donor recommendations unless they raise compliance concerns. Donors can involve family members in the recommendation process.

This allows multiple generations to participate in philanthropic decisions while the fund remains under the foundation's control.

Step 4 — Grants Are Made to Qualified Donees or Grantee Organizations

The DAF Holding Charity reviews each grant recommendation to ensure the recipient is a qualified donee under Canadian tax law. Qualified donees include registered charities, municipalities, and certain other organizations approved by the Canada Revenue Agency.

DAF grants totalled over $1.4 billion annually and supported more than 20,000 Canadian charities in recent years. Community foundations and other DAF Holding Charities distribute these funds to support charitable activities across the non-profit sector.

The foundation issues the grant cheque directly to the recipient charity. The charity receives the funds from the DAF Holding Charity, not from the original donor.

Many foundations will share the donor's name if requested.

What Is a DAF at Law?

A donor-advised fund operates under specific legal rules in Canada. The Canada Revenue Agency (CRA) views a DAF as a fund owned and controlled by a registered charity, not by the donor who creates it.

A DAF Is a Charitable Gift

When a donor establishes a DAF, they make an irrevocable charitable contribution to a registered charity. The donor cannot get the money back once they transfer it to the fund.

This is a complete gift, not a loan or deposit. The charity that holds the DAF becomes the legal owner of the donated funds.

The donor loses legal control over the money. They can only make recommendations about which qualified donees should receive grants from their fund.

The charity holding the fund must make all final decisions about distributions. They are not legally required to follow the donor's recommendations, though most charities typically do.

Restricted vs. Unrestricted DAF Gifts

Donors can place certain restrictions on their DAF gifts. Common restrictions include which types of charities can receive grants or what charitable purposes the funds should support.

The CRA allows these restrictions as long as they stay within legal limits. Some donors try to maintain too much control through restrictions.

The CRA may refuse to recognize a gift as charitable if the donor keeps excessive control. The charity must have real authority to direct how the funds are used.

Unrestricted gifts give the charity full discretion to distribute funds to any qualified donee. These gifts provide the most flexibility but give donors less influence over how their money is used.

The Gift Must Qualify for a Donation Receipt Under the Income Tax Act

For a donor to receive a charitable tax receipt, the gift must meet Income Tax Act requirements. The gift must be voluntary, made without expectation of return benefit, and transferred to a qualified donee.

The CRA issues the tax receipt at the time the donor transfers funds into the DAF. The donor receives the full tax benefit immediately, even though the charity may distribute the funds to other charities over many years.

The tax receipt amount equals the fair market value of the property donated.

Why Are Donor Advised Funds So Popular in Canada?

Donor-advised funds have become one of the fastest-growing segments of Canadian philanthropy because they cost less than private foundations and give donors more control over their giving timeline. In 2021, DAFs granted nearly $1 billion to Canadian charities and accounted for almost 10% of all receipted donations by Canadian tax filers.

Lower Cost Than a Private Foundation

Private foundations require significant resources to establish and maintain. Legal fees, accounting costs, and ongoing administrative expenses can easily exceed $10,000 per year.

DAF Holding Charities handles all administrative work, including tax receipts, record keeping, and regulatory compliance. Management fees for donor-advised funds typically range from 0.5% to 2% of assets annually.

This is considerably less than what most private foundations spend on operations. Donors also avoid the legal complexity of setting up a separate charitable entity.

There are no incorporation costs, no separate tax filings, and no board meeting requirements. Many community foundations and giving funds offer DAFs with low or no minimum balance requirements.

This makes structured philanthropy accessible to donors who might not have the wealth needed for a private foundation.

Flexibility and Anonymity for Donors

DAFs give donors immediate tax benefits while allowing time to decide which charities to support. A donor can contribute assets during a high-income year, claim the tax deduction right away, and recommend grants to charities over several years.

The funds grow tax-free while sitting in the donor-advised fund. Donors can contribute cash, securities, or other assets to their DAF.

Many donors transfer appreciated stocks or mutual funds to avoid capital gains tax. The full fair market value becomes eligible for a donation receipt.

The DAF ecosystem in Canada also supports anonymous giving. Donors can recommend grants without their names appearing on the charity's records.

This privacy appeals to individuals who want to support causes without public recognition or solicitation from other organizations.

DAF Growth Trends in Canada

Canadian DAFs have experienced strong growth over the past decade. The sector has expanded far beyond its early adopters among high-net-worth individuals.

More Canadians now use donor-advised funds as their primary vehicle for charitable giving. Community foundations across Canada have added DAF programs to serve local donors.

National firms also offer DAF options that allow donors to support charities anywhere in the country. This competition has improved services and reduced fees.

The growth mirrors trends seen in other countries, particularly the United States where DAFs have been popular for decades. Canadian donors and their advisors increasingly understand how donor-advised funds can maximize tax efficiency while simplifying the giving process.

Key Legal Issues Canadian Charities Must Understand

Canadian charities working with donor-advised funds face specific legal requirements under the Income Tax Act and Canada Revenue Agency regulations. These rules affect how DAF Holding Charities operate and how they distribute funds.

Recipient charities must also report and manage grants from DAF accounts.

Disbursement Quota Requirements

All registered charities in Canada must meet a disbursement quota (DQ) each year. The DQ is the minimum amount that a charity must spend on its own charitable activities or gifts to qualified donees.

For DAF Holding Charities, this requirement applies to the total assets they hold across all DAF accounts combined — not to each individual account separately. The Canada Revenue Agency calculates the DQ based on property a charity owns that it does not use in charitable activities or administration.

For most foundations, this includes investment portfolios and cash held in DAF accounts. Foundations must spend at least 3.5% of the average value of these assets over the previous 24 months.

A critical practical point: because the DQ is calculated at the organizational level, a foundation can technically satisfy its overall quota by distributing heavily from some DAF accounts while other individual accounts remain largely idle. A donor might see little movement in their particular fund even as the foundation meets its legal obligations overall. This is a significant area of ongoing scrutiny by the CRA, which is reviewing whether the current DQ framework adequately ensures that funds flow to active charities rather than accumulate within individual accounts indefinitely.

Charities that fail to meet their overall DQ face penalties, including potential loss of charitable status.

The 2023 Disbursement Quota Increase

In 2023, the federal government increased the disbursement quota for registered charities. The quota rose from 3.5% to 5% for the portion of property that exceeds $1 million.

This change significantly affects foundations that manage large DAF portfolios.

A foundation with $10 million in assets now calculates its quota differently. The first $1 million requires a 3.5% disbursement ($35,000).

The remaining $9 million requires a 5% disbursement ($450,000). The total disbursement quota is now $485,000 instead of the previous $350,000.

This increase creates pressure on DAF Holding Charities to move more money out to working charities across their entire portfolio.

However, because the DQ applies at the organizational level, donors should not assume their individual fund will automatically be subject to faster payouts.

Donors who expected their funds to grow over many years may still need to adjust their giving timelines, and foundations must communicate these requirements clearly to fund advisors to avoid quota shortfalls at the organizational level.

Changes to the T3010 Annual Charity Information Return

The Canada Revenue Agency updated Form T3010 to require more detailed reporting about donor-advised funds. DAF Holding Charities must now disclose specific information about their DAF operations in their annual filings.

This increased transparency helps the CRA monitor how DAFs operate across Canada.

The form asks foundations to report:

- The number of DAF accounts they manage

- The total value of assets held in all DAF accounts

- The amount granted out from DAFs during the fiscal year

- Administrative fees charged to DAF accounts

This reporting helps distinguish between foundations that actively distribute DAF assets and those that allow funds to accumulate. Charities receiving grants from DAFs do not face special reporting requirements.

However, they should keep records showing the source of funding for their own tracking purposes.

Qualifying Disbursements — Gifts to Grantee Organizations

Grants from DAF Holding Charities to other registered charities count as qualifying disbursements toward the foundation's quota. These grants must meet specific legal requirements to qualify.

The receiving charity must be a qualified donee under the Income Tax Act. The DAF Holding Charity must maintain direction and control over how grants are used.

This means the foundation, not the donor, makes the final decision about all grants. The donor can recommend grants to specific charities, but these recommendations are non-binding.

The foundation must conduct due diligence on recipient charities. This includes verifying charitable registration status and ensuring the grantee can use funds for charitable purposes.

Foundations cannot simply act as a pass-through for donor instructions. They must exercise independent judgment about each grant.

When a grant moves from a DAF Holding Charity to a working charity, the working charity does not issue a tax receipt. The donor already received a receipt when they initially contributed to the DAF.

This prevents double-receipting of the same funds.

The Anti-Directed Giving Provision Under the Income Tax Act

Section 149.1(4.1) of the Income Tax Act prohibits directed giving arrangements. This provision prevents donors from using charities as conduits to direct benefits to specific individuals or organizations for non-charitable purposes.

The rule applies directly to how DAFs operate. A directed giving arrangement exists when a charity accepts a gift on the condition that it transfer funds to a particular person or organization specified by the donor.

These arrangements can result in loss of charitable status. The CRA distinguishes between legitimate donor recommendations and improper direction.

DAF Holding Charities must ensure that donors understand they cannot control how funds are used after donation. The foundation must have the legal authority and practical ability to refuse donor recommendations.

Written policies should clarify that donor suggestions are advisory only. Some foundations implement waiting periods or require board approval for large grants to demonstrate independence from donor control.

These practices help protect against challenges that a directed giving arrangement exists.

A note on the Alternative Minimum Tax (AMT): While DAFs offer significant tax advantages, high-net-worth donors who transfer large amounts of assets to a DAF in 2024 and beyond should consult their accountants about the revised Alternative Minimum Tax rules.

Changes introduced by the federal government limit the extent to which certain donation tax credits can reduce AMT liability for high earners. The tax benefit of a large DAF contribution remains substantial, but the interaction between DAF giving and the revised AMT rules requires careful planning for affected donors.

Granting Policies: Why They Matter

Clear granting policies protect both DAF Holding Charities and the charities they support. These policies establish how the foundation evaluates grant recommendations and conducts due diligence.

Written policies demonstrate that the foundation exercises proper direction and control. A comprehensive granting policy typically covers:

- Minimum and maximum grant amounts

- Types of qualified donees eligible for grants

- Due diligence procedures for vetting recipient charities

- Timelines for processing grant requests

- Circumstances under which the foundation may decline a recommendation

- How the foundation handles grants to controversial organizations

Charities receiving grants from DAFs should ask about the foundation's granting policies. Understanding these policies helps charities set realistic expectations for funding timelines and requirements.

Some foundations grant funds quickly, while others have quarterly or annual review processes.

Successor Fund Advisors

Many DAF agreements allow donors to name successor advisors who can recommend grants after the original donor dies or becomes incapacitated. This feature helps families continue philanthropic traditions across generations.

However, successor advisors create legal considerations for foundations. The foundation must clearly document the succession arrangement in writing.

The agreement should specify who becomes successor advisor, under what conditions, and what authority they have. Some foundations limit the number of successor generations to prevent DAF accounts from existing indefinitely.

Foundations should require successor advisors to formally accept their role and acknowledge that their recommendations are non-binding. This protects against future disputes about control over the funds.

The foundation retains ultimate authority regardless of succession arrangements. Tax implications also matter.

When a donor names successors, the DAF does not form part of the donor's estate for probate purposes because the charity owns the funds. However, the donor cannot receive any material benefit from establishing the succession arrangement.

The Impact of Anonymous DAF Donations

The Lebovic Case — Canada's First Court Decision on DAFs

In 2022, the Ontario Superior Court of Justice delivered its first ruling on donor advised funds in The Joseph Lebovic Charitable Foundation v. Jewish Foundation of Greater Toronto. The court confirmed that donors give up control when they contribute to a DAF and cannot force the holding charity to follow their recommendations.

Key Facts

Joseph Lebovic founded the Joseph Lebovic Charitable Foundation (JLCF), a private foundation. Between 2011 and 2016, he donated $19,350,000 through JLCF to the Jewish Foundation of Greater Toronto.

The Jewish Foundation held these donations in a donor advised fund called the Lebovic Fund and made grants according to Joseph's recommendations. After Joseph died in 2021, his brother Wolf Lebovic took over as executor of the estate and president of JLCF.

Wolf demanded that the Jewish Foundation make specific grants from the Lebovic Fund as he directed. The Jewish Foundation refused to comply.

Wolf brought legal action seeking an injunction to force the Jewish Foundation to distribute funds as JLCF instructed and to stop the foundation from making any other distributions from the Lebovic Fund.

What the Court Decided

The court rejected Wolf Lebovic's claims and refused to grant the injunction. The judge found no serious legal issue to consider at trial.

The court ruled there was no enforceable agreement requiring the Jewish Foundation to follow JLCF's recommendations. The judge emphasized that "in order for charitable gifts to be valid, donors must divest themselves of all power and control over the property and transfer such control to the donee."

Any agreement giving the donor control over donated property would be invalid and unenforceable. The court also refused to order the Jewish Foundation to consider JLCF's recommendations in good faith.

Such a direction would effectively give the donor control over the donated property, which contradicts the basic legal requirement for valid charitable gifts. The court determined it was unnecessary to decide whether Wolf Lebovic could succeed Joseph as the fund's adviser.

Since JLCF had no legal right to require specific donations regardless of adviser status, this question was irrelevant to the case outcome.

Why This Case Matters for DAF Holding Charities

This decision was the first time a Canadian court examined donor advised funds in detail. It clearly established that DAF holding charities maintain full legal control over donated funds, even when donors make recommendations.

Charities operating DAFs can rely on this precedent to defend their decision-making authority. Donors who disagree with how their DAF makes grants have no legal recourse to force compliance with their wishes.

The donated funds belong to the charity, not the donor. The case also highlighted the importance of succession planning for fund advisers.

Joseph Lebovic did not create a formal succession plan during his lifetime. The Jewish Foundation argued this meant the Lebovic Fund became part of their unrestricted funds.

Charities should establish clear policies about appointing successor advisers and what happens when donors fail to designate successors.

DAFs in Canada vs. the United States

While donor-advised funds share the same basic concept in both countries, Canada operates under a distinct legal framework. This framework shapes how these funds work and what donors can expect.

Different Legal Frameworks

In Canada, a DAF is a fund held within a registered charity or foundation. The fund belongs entirely to that charity.

When a donor contributes money, they receive a charitable tax receipt for the full amount. The donation becomes the property of the foundation.

The United States treats DAFs differently under its tax code. American law divides charities into public charities and private foundations, with different rules for each type.

Canada uses three categories: charitable organizations, public foundations, and private foundations.

Key structural differences include:

- Canadian DAFs must always be part of an existing charity

- U.S. DAFs can be held by specialized 501(c)(3) organizations

- Canadian law requires charities to maintain "direction and control" over all funds

- American donors receive more explicit advisory rights

Canada does not have a standalone legal definition for donor-advised funds in its tax legislation. The term describes how certain funds operate within charities, not a separate legal entity.

Why Canadian DAF Rules Are Stricter

Canadian charities that operate as DAF Holding Charities must exercise complete direction and control over the funds. This means the charity makes final decisions about all grants, even when donors provide recommendations.

The Canada Revenue Agency enforces this requirement strictly. Charities cannot simply rubber-stamp donor requests.

They must independently verify that each grant goes to a qualified recipient and serves charitable purposes.

Canadian requirements include:

- All DAF assets count toward the charity's disbursement quota

- Charities must spend a minimum percentage of assets annually

- Donors cannot legally enforce their recommendations

- The DAF Holding Charity bears full legal responsibility

American regulations allow donors more influence over their DAF accounts. While recommendations are technically non-binding in both countries, U.S. sponsors often process donor requests with minimal oversight.

Canadian charities face stronger regulatory scrutiny about maintaining actual control.

What "Languishing Assets" Concerns Really Mean in the Canadian Context

The debate about DAF assets sitting idle affects Canada differently than the United States. Canadian charities already face disbursement quota requirements that apply to all their assets, including DAF holdings.

Public and private foundations in Canada must spend 3.5% of their average asset value each year on charitable activities. This rule covers DAF assets held by these foundations.

However, because the DQ applies to the foundation's overall asset base — not to individual accounts — some DAF funds can still sit idle while the organization technically meets its obligations through other accounts. A donor who opens a DAF and contributes $100,000 may find that their specific fund distributes little or nothing in a given year, even if the foundation as a whole meets its quota requirements.

The CRA is aware of this gap and is actively reviewing how the DQ framework addresses the issue of individual DAF accounts that accumulate without distributing to active charities. Both donors and DAF Holding Charities should monitor any regulatory changes in this area.

Practical Guidance for Charities Administering DAFs

Charities that create and manage donor-advised funds need strong policies and clear procedures to protect their charitable mission. Proper governance ensures compliance with tax rules while building trust with donors and professional advisors.

Conduct Proper Due Diligence

Charities must verify that potential DAF donors and their assets meet legal and ethical standards before accepting contributions. This process protects the organization from reputational harm and legal issues.

The due diligence process should screen for the source of funds to ensure they come from legitimate sources. Charities need to confirm that accepting certain assets won't create conflicts with their mission or values.

Background checks become especially important for large gifts or complex assets like private company shares or real estate. The charity should document all due diligence steps taken.

Professional advisors often help donors structure significant contributions. The charity should request information about the nature of these relationships to understand any potential conflicts of interest.

Develop Written Gift Acceptance and Granting Policies

Clear written policies help staff and board members make consistent decisions about DAF administration. These policies protect the charity's interests and support donor goals.

The gift acceptance policy should specify which types of assets the charity will accept into DAFs. Common categories include cash, publicly traded securities, private business interests, and real property.

Each asset type requires different handling procedures and cost considerations.

Granting policies outline how the charity reviews and approves grant recommendations from DAF donors. The policy must state that the charity's board holds final authority over all grants.

This includes minimum and maximum grant amounts, eligible recipients, and timelines for processing requests.

Policies should address administrative fees charged to cover the costs of managing DAFs. Typical fees range from 0.5% to 2% of fund assets annually.

The policy needs to explain how these fees are calculated and applied.

Prepare Template DAF Agreements

A well-drafted DAF agreement protects both the charity and the donor by setting clear expectations from the start. The template should be reviewed by legal counsel familiar with Canadian charity law.

The agreement must state that all contributions become the charity's property immediately upon receipt. Donors receive a tax receipt because they give up legal ownership and control of the funds.

Template agreements should outline the donor's ability to make grant recommendations. The document needs to specify any restrictions the charity will accept on grants.

Include provisions about what happens if the donor dies or becomes incapacitated. Many agreements allow donors to name successor advisors who can continue making recommendations.

The agreement should address how the fund will be handled if it becomes too small to administer cost-effectively.

Your Charity Must Control the Process — Not the Donor

Canadian tax law requires that charities maintain full legal control over DAF assets and granting decisions. The charity cannot act as a conduit for donor instructions.

Staff and board members need training to recognize when donor involvement crosses into improper control. Red flags include donors who demand immediate processing of grants or who try to receive personal benefits through their recommendations.

The charity should establish a review process for all grant recommendations. This might involve staff review for routine grants and board approval for larger or unusual requests.

The process demonstrates that the charity exercises independent judgment.

The charity should keep records showing that it evaluated each grant recommendation against its charitable purposes and policies. These records prove the charity's control if questioned by tax authorities.

Avoid Language That Implies Donor Ownership

The words used in agreements, receipts, and communications must reflect the charity's ownership of DAF assets. Incorrect language can jeopardize the tax benefits donors receive.

Never refer to funds as belonging to the donor or use phrases like "your account" or "your fund balance." Instead, use neutral terms like "the fund you established" or "the fund from which you may recommend grants."

Marketing materials and DAF resources should explain that donors make recommendations rather than directions. Impact reports should thank donors for their role in facilitating grants while acknowledging the charity's decision-making authority.

Staff members who communicate with donors need guidance on appropriate language. A simple phrase guide helps everyone use consistent, legally sound terminology.

Use DAFs as a Donor Engagement Opportunity

DAF donors often maintain giving relationships with charities for many years. This creates opportunities for deeper engagement and strategic giving discussions.

Regular communication keeps donors informed about the impact of grants they recommended. Quarterly or annual impact reports show how their activities support the charity's mission.

These reports might highlight specific programs funded or broader community outcomes achieved.

Charities can offer educational events about effective giving strategies for DAF holders. Topics might include multi-year granting approaches, supporting endowments, or involving family members in philanthropic decisions.

Personal meetings with significant DAF donors allow charity staff to discuss emerging needs and opportunities. These conversations often lead to larger or more strategic grants.

The charity should track donor interests and motivations to suggest relevant giving opportunities.

Some charities create advisory committees that include DAF donors. This involvement builds loyalty while respecting the legal boundaries around fund control.

Conclusion

Donor-advised funds now grant over $1.4 billion each year to more than 20,000 Canadian charities. These funds have become a major part of how Canadians give to charity.

Understanding how DAFs work helps charities build better relationships with donors and secure more funding. Charities that learn about DAFs can create stronger fundraising strategies.

They can also improve how they communicate with DAF donors and the foundations that hold these funds. The growth of DAFs means more opportunities for charities to receive grants, but only if they know how to engage with this giving model.

B.I.G. Charity Law Group helps Canadian charities navigate donor-advised funds and other legal matters. Contact us at 416-488-5888 or dov.goldberg@charitylawgroup.ca for guidance on working with DAF donors.

Visit CharityLawGroup.ca to learn more about charity law services. Or schedule a FREE consultation to discuss your organization's specific needs.

Frequently Asked Questions

Donor-advised funds involve specific rules about tax deductions, eligibility, anonymity, and regulatory requirements that affect both donors and Canadian charities. Understanding the grant recommendation process and possible drawbacks helps all parties navigate DAF relationships effectively.

What are the disadvantages of a donor-advised fund?

Donor-advised funds require donors to give up legal control of their contributions once they make them. The funds become the property of the DAF Holding Charity, which means donors cannot get their money back.

DAF Holding Charity charges administrative fees to manage the accounts. These fees typically cover investment management and grant processing, which reduces the total amount available for charitable giving over time.

Some critics point out that funds can sit in DAF accounts for years without being distributed to charities. While the donor receives an immediate tax receipt, the actual charity may not see those funds right away.

DAF Holding Charity has the legal authority to refuse grant recommendations. Although foundations rarely reject recommendations, donors must understand they are making suggestions rather than directing payments.

Are donations 100% tax deductible in Canada?

Donations to donor-advised funds qualify for the same tax treatment as direct donations to registered charities. Donors can claim up to 75% of their net income in charitable tax credits in most years.

The donation tax credit provides a 15% federal credit on the first $200 donated and 29% on amounts above that. Provincial credits add to this benefit, making the combined rate range from 40% to 54% depending on the province.

Donors can carry forward unused donation credits for up to five years if they cannot use them in the current tax year. This flexibility helps donors manage their tax planning across multiple years.

High-net-worth donors making large contributions should also be aware of the revised Alternative Minimum Tax (AMT) rules. Changes introduced by the federal government limit how much certain donation tax credits can reduce AMT liability for high earners. Consulting an accountant before making a significant DAF contribution is advisable.

Who is eligible for donor-advised funds?

Any individual or family can open a donor-advised fund, though different foundations set their own minimum contribution requirements. Some foundations require as little as $5,000 to start, while others may require $25,000 or more.

Corporations and other organizations can also establish donor-advised funds. This option allows businesses to manage their charitable giving through a structured vehicle.

Financial capacity is the main eligibility factor. Donors need enough assets to meet the minimum requirements and cover ongoing administrative fees.

Are there any regulations that Canadian charities should be aware of when receiving funds from a Donor Advised Fund?

The Canada Revenue Agency regulates DAF Holding Charities as registered charities, which means they must follow the same rules as other charitable organizations. These foundations must ensure grants only go to qualified donees under the Income Tax Act.

Canadian charity law requires DAF Holding Charities to maintain direction and control over all grants. The CAGP Foundation emphasizes that Canada's regulatory framework addresses many concerns about accountability that exist in other countries.

Charities receiving DAF grants face the same reporting requirements as they do for any other donation. They must issue receipts to the DAF Holding Charity, not to the original donor, and track the funds according to standard accounting practices.

How does the grant recommendation process work for Donors using Advised Funds?

Donors submit grant recommendations to their DAF Holding Charity through an online portal, phone call, or written request. The recommendation includes the charity name, amount, and any special instructions about the gift.

The DAF Holding Charity reviews each recommendation to verify the recipient is a qualified donee. This verification process typically takes a few days to a few weeks, depending on the foundation's procedures.

Once approved, the foundation issues a cheque or electronic transfer to the charity. The foundation handles all administrative work, including tax receipts and record-keeping.

Donors can recommend grants at any time and in any amount, as long as they have sufficient funds in their account. The Canadian Association of Gift Planners notes this flexibility allows donors to respond quickly to community needs or time their giving strategically.

Can donors retain a level of anonymity with Donor Advised Funds when contributing to Canadian charities?

Donor-advised funds allow donors to make anonymous grants to charities. The grant comes from the DAF Holding Charity rather than directly from the donor.

This means the charity only sees the foundation's name unless the donor chooses otherwise. Donors can instruct their DAF Holding Charity to include or exclude their identity when making grants.

Some donors prefer full anonymity. Others want charities to know who supports them.

Anonymity can complicate donor stewardship efforts for charities. Organizations may struggle to thank donors and build relationships when they don't know who contributed through a DAF.

Charities can ask DAF Holding Charities to share donor contact information. However, the foundation must get the donor's permission first.

This arrangement protects donor privacy. It also allows those who want recognition to receive it.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

.png)