CRA Charities Directorate Books and Records Guide Overview

Running a registered charity in Canada comes with many responsibilities. One of the most critical is maintaining proper books and records.

The Canada Revenue Agency requires all registered charities to keep adequate books and records that demonstrate how donations are used and prove that activities remain charitable. Many charities have faced serious consequences, including loss of registered status, because their record-keeping practices didn't meet CRA standards.

The Charities Directorate has been paying closer attention to how charities manage their documentation. Recent enforcement actions show that inadequate books and records can lead to penalties, suspended receipting privileges, or even revocation.

Understanding what the Canada Revenue Agency expects is essential for protecting your charity's status and maintaining public trust. This guide covers everything your charity needs to know about CRA books and records requirements.

You'll learn what documents to keep, how long to retain them, what counts as proper record-keeping, and how to avoid mistakes that trigger CRA concerns. Whether your charity is new to these requirements or looking to improve current practices, this article provides practical steps to ensure compliance.

Why CRA Is Focusing on Books and Records Right Now

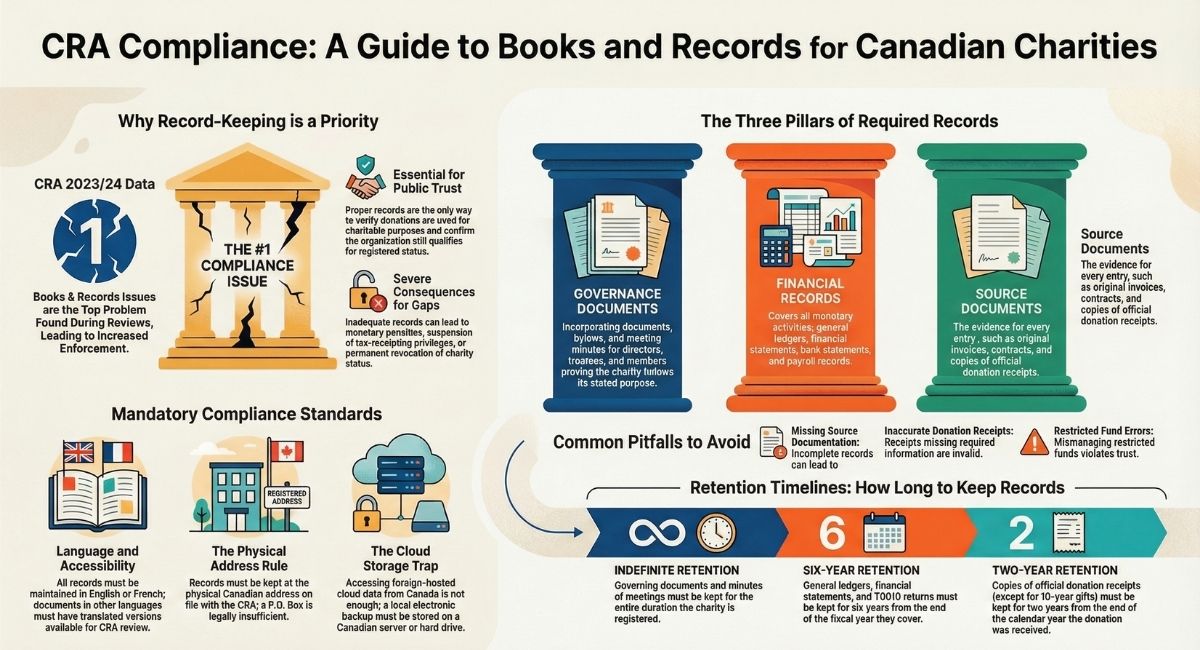

The CRA Charities Directorate has made books and records a top compliance priority in recent years. Poor record-keeping has become one of the most common reasons charities face sanctions or lose their registered status.

The 2023/24 compliance data shows books and records issues topped the list of problems the CRA found during reviews. Many charities made minor errors like missing travel logs or failing to keep current governing documents on file.

Others had more serious gaps that prevented the CRA from verifying how donations were used. The CRA is focusing on this area because proper records are the only way to:

- Verify that donations are being used for charitable purposes

- Confirm activities match the charity's registered purposes

- Ensure the organization still qualifies for registered status

- Complete accurate T3010 returns each year

Recent revocations have sent a clear message to the sector. The CRA will not overlook inadequate record-keeping, even from well-intentioned organizations.

This enforcement approach aims to protect donors and maintain public trust in the charitable sector. The shift also reflects the CRA's broader modernization efforts.

As more charities move to digital systems and cloud storage, the agency has updated its guidance on electronic records. Cloud storage is acceptable as long as records remain accessible from Canada in a usable format.

Charities that treat record-keeping as an ongoing priority will find compliance much easier to manage.

What the Income Tax Act Requires for Charity Record Keeping

The Income Tax Act sets out specific requirements for registered charities to maintain their tax-exempt status. These rules apply to all charities operating in Canada, regardless of their size or activities.

Charities must keep books and records that allow the CRA to verify several key items. The records need to show all revenue, including donations received.

They must prove that resources are spent on allowable activities. The documents also need to confirm that the charity's purposes remain charitable and that it continues to meet registration requirements.

Required record-keeping practices include:

- Maintaining all books and records in English or French

- Keeping records at the registered Canadian address on file with the CRA — this must be a physical, geographical location, not a P.O. Box

A P.O. Box does not meet this requirement. The registered address must be a physical location where CRA auditors can visit and inspect the records during regular business hours.

- Making records available for CRA inspection and audit

- Storing documents related to both Canadian and international activities

The Act gives CRA officials the authority to inspect, audit, copy, or examine a charity's records. This power is outlined in section 231.1 of the Tax Act.

Charities cannot refuse access to these documents. Records can be kept in paper format or electronically.

A backup copy should be stored in a separate location. If a charity hires an accountant or bookkeeper to handle records, the charity remains responsible for meeting all CRA requirements.

The Income Tax Act does not list every specific record a charity must keep. If the CRA finds inadequate record-keeping, the Minister of National Revenue can specify what records and books of account the charity must maintain going forward.

What Counts as "Books and Records" for a Registered Charity

The CRA requires registered charities to maintain three main categories of documents: governance documents, financial records, and source documents.

Governance documents include the charity's incorporating documents, bylaws, and governing documents that establish how the organization operates. Minutes of meetings for directors, trustees, members, and staff also fall into this category.

These records prove the charity is running according to its stated purposes. Financial records cover all monetary activities of the organization.

This includes financial statements, ledgers, bank statements, and statement of financial position. Bank reconciliation documents and payroll records are also required.

The general ledger or other books of final entry must show year-to-year transactions. Source documents provide evidence for all financial entries.

These include original receipts, invoices, and contracts. Official donation receipts and copies of all donation receipts issued to donors are critical source documents.

Records of in-kind donations must also be maintained with proper documentation of their value. All books and records must be kept in English or French.

If documents were created in another language, a translated version must be available for CRA review. The charity remains responsible for maintaining these records even if it hires a third party to manage them.

Each type of record serves a specific purpose in demonstrating that the charity is using its resources for charitable purposes and meeting all legal requirements.

How Long Must Charities Keep Their Records?

The CRA has specific requirements for how long charities must keep different types of records. The retention period depends on the type of document.

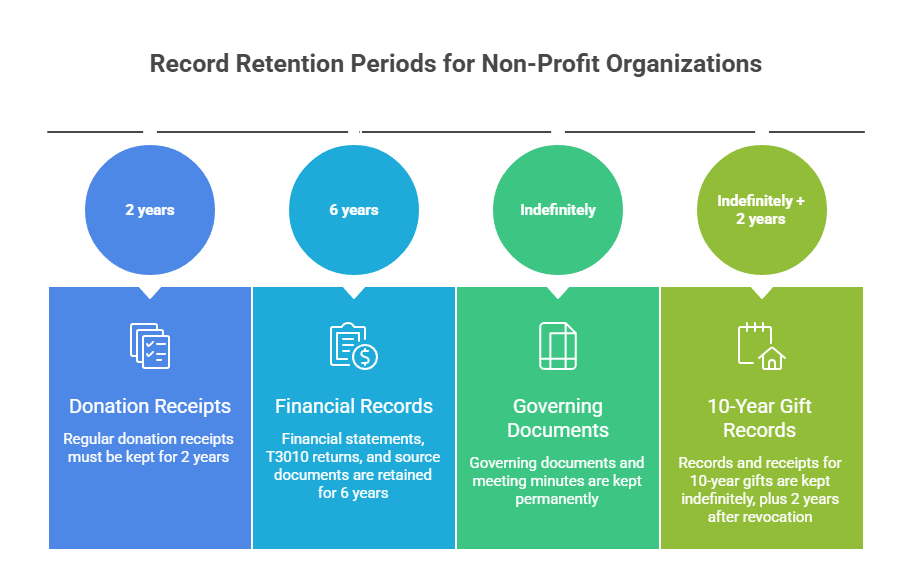

Donation receipts must be kept for two years from the end of the calendar year in which the charity received the donations. If a charity cancels or reissues receipts, those records must be kept for two years after the end of the calendar year in which they were cancelled or reissued.

Financial and operational records require six years of retention from the end of the fiscal year they cover. This includes general ledgers, financial statements, source documents, promotional materials, and T3010 returns.

If a charity files its T3010 late, it must keep these records for six years from the late-filing date. When a charity loses its registered status, these records only need to be kept for two years after revocation.

Governing documents must be kept indefinitely while the charity is registered. This includes meeting minutes of directors, trustees, members, and staff, along with governing documents and bylaws.

If the charity is revoked, these records must be kept for two years after the revocation date.

An important exception applies to 10-year gifts, also called enduring property. Unlike regular official donation receipts, which only require two years of retention, records and receipts related to 10-year gifts must be kept indefinitely for as long as the charity is registered, plus two years after the date of revocation.

This distinction matters because 10-year gifts carry ongoing obligations that extend well beyond the initial donation, and the CRA expects a complete record of these arrangements to remain on file throughout.

Charities that want to destroy records before the required period ends must get written permission from the Minister of National Revenue by submitting Form T137.

Common Books and Records Failures CRA Has Identified

The CRA has documented several recurring compliance issues during charity audits. These problems often stem from unintentional errors rather than deliberate violations.

Incomplete or inaccurate donation receipts are one of the most frequent failures. Charities sometimes miss required information on official donation receipts or fail to keep copies for the mandatory two-year period.

Inadequate financial documentation causes significant compliance concerns. Many charities struggle to maintain proper records that verify their disbursement quota calculations or demonstrate how resources were spent on charitable programs.

Without clear financial trails, the CRA cannot confirm that funds were used appropriately. The following issues appear regularly in CRA compliance reports:

- Non-material errors or omissions in books and records

- Missing travel logs to support expense claims

- Failure to maintain current governing documents

- Incomplete or incorrect T3010 returns

- Records not kept at the registered Canadian address

Missing source documents create verification challenges. Charities sometimes lack receipts, invoices, or other supporting documentation for expenses and income.

This makes it impossible for the CRA to verify financial activities. Governance record gaps also rank among common failures.

Organizations may not keep meeting minutes indefinitely as required, or they fail to update their bylaws and governing documents on file. Minor errors often result in educational interventions from the CRA.

Repeated failures or more serious violations can lead to monetary penalties, suspension of tax-receipting privileges, or even revocation of charitable status.

Electronic Records — What CRA Accepts

The CRA allows registered charities to keep their books and records in electronic format. This includes financial statements, receipts, source documents, and meeting minutes stored digitally.

Key Requirements for Electronic Records

Electronic records must remain in an electronically readable format. The information must be supported by a system that can produce an accessible and usable copy for auditors to review.

A charity cannot simply print electronic records and dispose of the digital versions. If records were created and maintained electronically, they must stay in electronic format even if paper copies exist.

Cloud Storage — A Common Compliance Trap

Many charities assume that using cloud-based software automatically meets CRA requirements as long as they can log in from Canada. This assumption is legally incorrect and has led to serious compliance failures.

Under the Income Tax Act, the ability to access records electronically from Canada does not mean the records are legally "kept in Canada." The CRA is statutorily prohibited from granting charities permission to store their primary records outside the country. This means that if your charity uses foreign-hosted cloud software — such as QuickBooks Online, Google Workspace, Dropbox, or any service operating on U.S.-based or other international servers — simply logging in from your Canadian office is not sufficient.

To comply with the law, charities using foreign-hosted cloud platforms must routinely download and store a local electronic backup at their registered Canadian address. This backup should be saved on a local hard drive or a Canadian physical server and updated on a regular basis. The backup copy must be accessible and readable by CRA auditors upon request.

Relying on remote access alone — even if the service is widely used and reputable — is an audit risk that the CRA has flagged in its guidance on records kept outside of Canada.

Access and Inspection

CRA officials have the authority to inspect, audit, copy, or examine electronic records. Charities must make these records available to authorized officials upon request.

The system used to store electronic records needs to allow auditors to process and analyze the information properly. Language Requirements

Electronic records must be kept in English or French. If records were originally created in a different language, a translated version must be available for CRA review.

Location Standards

Electronic records must be physically accessible from the Canadian address registered with the CRA. The storage system must allow the charity to retrieve and display the records from this registered location.

What Happens If Your Charity's Books and Records Are Inadequate

The Canada Revenue Agency takes inadequate record-keeping seriously. Charities that fail to maintain proper books and records face significant consequences that can affect their operations and status.

Potential Sanctions Include:

- Monetary penalties and fines

- Suspension of tax-receipting privileges

- Loss of registered charity status (revocation)

When a charity loses its ability to issue official donation receipts, it becomes much harder to raise funds. Donors cannot claim tax credits for their contributions, which often leads to reduced donations.

Revocation of registered status is the most severe penalty. Once revoked, an organization can no longer operate as a registered charity.

It loses all the benefits that come with charitable registration, including tax exemptions. The CRA has authority to inspect, audit, copy, or examine any charity's records.

Officials can access both paper and electronic records during these reviews. Charities must make their books and records available when requested.

Common Record-Keeping Issues:

- Missing or incomplete financial records

- Donation receipts not properly stored

- Records kept outside of Canada

- Documents in languages other than English or French without translations

- Failure to retain records for the required time periods

Charities cannot claim ignorance as a defence. Even if a third party like an accountant maintains the records, the charity remains responsible for meeting all requirements.

The organization's directors and officers bear the ultimate responsibility for adequate record-keeping.

Key Takeaways from the CRA Charities Directorate Webinar Presentations

The CRA Charities Directorate offers free webinars throughout the year. These sessions help registered charities understand their compliance obligations.

The webinars cover essential topics that affect day-to-day charity operations.

Books and records are a frequent topic in CRA presentations. The agency has revoked some charities for failing to maintain proper documentation.

Adequate books and records let the CRA verify donations. They also ensure charities use their resources correctly.

The webinars highlight several important areas:

- How to properly maintain financial records and documentation

- Common compliance issues across the charitable sector

- Updates on the shift toward online filing systems

- Gifting and receipting requirements

The T3010 Registered Charity Information Return receives significant attention. All registered charities must file this annual information return.

The T3010 form requires complete and accurate financial information. It also asks for details about charitable activities.

CRA presentations explain that inadequate records can range from minor mistakes to serious infractions. Deliberately altering, destroying, or hiding records can lead to severe consequences, including revocation of registered status.

The Charities Directorate uses these webinars to promote voluntary compliance through education. Charities can access educational tools and resources directly from the CRA.

Registration for these free sessions opens throughout the year. Organizations have multiple opportunities to learn about their filing obligations and requirements.

Charities should attend these webinars to stay current on regulatory changes. They also help organizations understand what the CRA expects when reviewing the T3010 return and supporting documentation.

How to Strengthen Your Charity's Books and Records Practices Today

Charities can improve their record-keeping by creating a clear system from the start. This means setting up proper fund accounting practices that separate restricted funds from unrestricted funds.

When donors give money with specific conditions, those restricted funds need their own tracking system.

A central filing location makes accessing records much easier. Whether the charity keeps paper files or electronic records, everything should be organized in one main area.

A backup copy stored in a different location protects against loss or damage.

Regular staff training helps prevent mistakes before they happen. Everyone who handles financial records needs to understand basic requirements.

This includes knowing how to track donations properly and maintain source documents.

Strong practices for fundraising materials matter too. Charities should keep copies of all appeals, campaigns, and donor communications.

These documents prove the charity used resources for charitable purposes.

Setting up a record retention schedule prevents confusion later. Staff members need to know which documents to keep for two years, six years, or indefinitely.

A simple chart posted in the office can serve as a quick reference guide.

Third-party bookkeepers can help maintain records, but the charity remains responsible. Regular internal reviews catch errors early.

Board members should ask to see financial reports at each meeting.

Electronic systems work well when they allow easy access from the registered Canadian address. Cloud storage is acceptable as long as the information remains accessible in Canada.

Records must always be available in English or French for potential audits.

Conclusion

Keeping proper books and records is not optional for registered charities in Canada. The CRA requires these documents to verify that your charity uses its resources for charitable purposes and meets all legal requirements.

Missing or incomplete records can lead to serious consequences, including penalties, loss of tax-receipting privileges, or even revocation of registered status.

Your charity must maintain records in English or French at a Canadian address on file with the CRA. Donation receipts must be kept for two years, while financial statements and source documents require six years of retention.

Governing documents and meeting minutes need to be kept indefinitely while your charity remains registered. These requirements apply whether records are kept on paper or electronically.

At B.I.G. Charity Law Group, we help charities understand CRA requirements and set up proper record-keeping systems that hold up to scrutiny. Our team brings deep expertise in charity compliance so your organization can meet all CRA standards with confidence.

Contact us at 416-488-5888 or dov.goldberg@charitylawgroup.ca to discuss your specific needs. You can also schedule a FREE consultation or visit CharityLawGroup.ca to learn more about how we can help.

Frequently Asked Questions

Registered charities in Canada must follow specific rules about keeping books and records. The CRA sets clear standards for what records to keep, how long to store them, and where they must be located.

What are the record-keeping requirements for registered charities under the Canada Revenue Agency?

Registered charities must keep adequate books and records that allow the CRA to verify all revenue and ensure resources are used for charitable purposes. These records must be stored at the charity's Canadian address on file with the CRA, even if the records relate to activities carried on outside Canada.

Records must be kept in either English or French. If records were originally created in another language, the charity must provide a translated version.

The charity's records need to show all financial transactions, charitable donations received, and proof that its purposes and activities remain charitable. Source documents like original receipts and invoices must support all entries in the books.

Organizations can keep records in paper format or electronically. The CRA recommends keeping all records in one area for easy access and maintaining backup copies in another location.

How long must a charity maintain its books and records according to Canadian charity law?

Different types of records have different retention periods. Copies of official donation receipts must be kept for two years from the end of the calendar year the charity received the donations.

Most financial records require six-year retention. This includes general ledgers, financial statements, source documents, and T3010 returns.

The six-year period starts from the end of the fiscal year the records cover.

Some records must be kept indefinitely while the charity remains registered. Meeting minutes of directors, trustees, members, and staff fall into this category.

Governing documents and bylaws also require indefinite retention.

If a charity's registration is revoked, it must keep most records for two years after the revocation date. Charities cannot destroy records before the required retention period ends without written permission from the Minister of National Revenue using Form T137.

Can a registered charity keep electronic copies of its records, and do these meet the CRA's compliance standards?

Registered charities can keep their books and records electronically. Electronic records meet the CRA's compliance standards when they contain the same information as paper records and remain accessible for inspection.

The charity must ensure electronic records are protected and backed up properly. A backup copy should be stored in a separate location to prevent loss of important information.

CRA officials have the authority to inspect, audit, copy, or examine all charity records. The organization must make electronic records available to these officials when requested.

What specific financial information must a charity include in its annual information return to the CRA?

The annual T3010 Registered Charity Information Return requires charities to report all revenue sources, including charitable donations received. The return must show how the charity spent its resources throughout the fiscal year.

Charities must document their programs and activities to demonstrate they are charitable in nature. Financial statements need to break down spending between charitable programs, management costs, and fundraising expenses.

The return asks for details about the charity's assets, liabilities, and overall financial position. Organizations must also report any transactions with non-arm's length parties and compensation paid to employees or contractors.

What are the consequences for a charity if it fails to keep proper books and records as per the CRA's regulations?

Failure to keep adequate books and records can result in serious sanctions from the CRA. The agency may impose monetary penalties on charities that do not meet record-keeping requirements.

The CRA can suspend a charity's tax-receipting privileges if it finds inadequate record-keeping. This suspension prevents the organization from issuing official donation receipts to donors.

In severe cases, poor record-keeping can lead to loss of registered status. Revocation means the charity can no longer operate as a registered charity and loses its tax-exempt status.

What guidelines does the CRA provide for charities to correctly allocate expenditures for charitable activities versus administrative costs in their records?

The CRA requires charities to track and report how they allocate spending across different categories. Books and records must clearly show which expenses relate to charitable programs, which cover management and administration, and which support fundraising activities.

Charities need to maintain source documents that support their allocation decisions. Invoices and receipts should demonstrate the purpose of each expense.

The T3010 return requires organizations to break down their expenditures by function. This helps the CRA verify that resources are used mainly for charitable purposes rather than administrative overhead.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

.png)