Essential Rules for Keeping Proper Books and Records

Published on

April 19, 2023

Last updated on

February 23, 2026

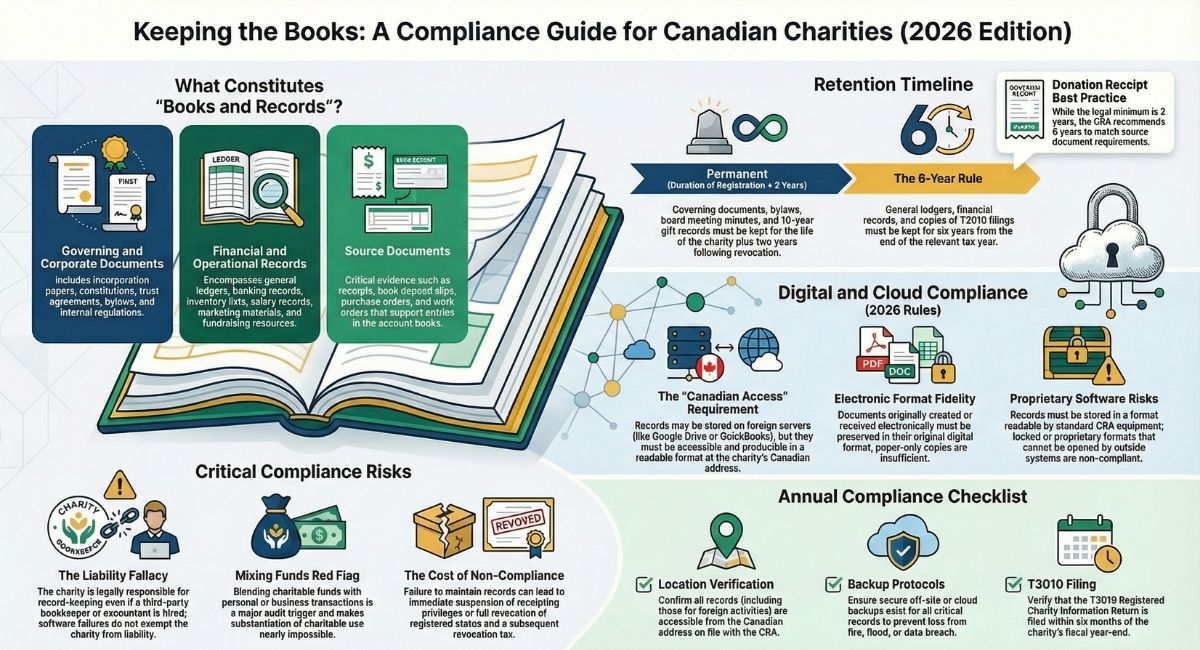

Every registered charity in Canada is legally required to maintain proper books and records under the Income Tax Act. These records allow the Canada Revenue Agency (CRA) to verify that charitable revenues are being reported accurately, that resources are directed to charitable purposes, and that the charity's activities align with its registered objects.

Records must be kept at a Canadian address and retained for specific periods depending on the document type. Failing to meet these requirements can result in suspension of receipting privileges or full revocation of charitable status.

What's New in 2025–2026: CRA Record-Keeping Updates

The CRA has continued to update its guidance on record-keeping compliance in recent years. Here is what charities should be aware of heading into 2026:

CRA's My Business Account Portal. The CRA now encourages all registered charities to manage their compliance obligations through the My Business Account portal, including filing the T3010 Registered Charity Information Return online. Charities that have not yet registered for this portal should do so to simplify annual reporting and correspondence with the CRA.

Increased Scrutiny on Charities with Foreign Activities. The CRA has stepped up audits on charities that carry out activities outside of Canada. These charities are expected to maintain thorough records of all foreign expenditures, partner agreements, and project documentation — all of which must still be kept at a Canadian address or be electronically accessible within Canada.

Electronic Records and Cloud Storage. The CRA has clarified that cloud-based record storage is acceptable, provided that records are stored in a format that can be accessed and read using standard CRA equipment. Charities using international cloud providers such as Google Drive or QuickBooks Online are generally compliant, as long as records can be produced in an electronically readable and usable format to CRA auditors on demand at the Canadian place of business.

T3010 Filing Deadlines Unchanged. The T3010 Registered Charity Information Return must still be filed within six months of the charity's fiscal year-end. Copies of all filed T3010s must be retained for six years from the end of the relevant tax year, plus two years following revocation of registration if applicable.

What Are Books and Records?

Books and records for a registered charity include a wide range of documents:

Governing and corporate documents such as incorporation papers, constitutions, trust agreements, bylaws, and internal regulations.

Financial records including account books, general ledgers, banking records, expenditure accounts, inventory lists, investment arrangements, salary records, and accountants' working papers.

Compliance documents such as copies of annual T3010 filings, official donation receipt copies, and written contracts or agreements.

Meeting records including minutes from board, director, trustee, executive, and members' meetings, as well as annual summaries and resolutions.

Operational documents such as marketing materials and fundraising resources.

Source documents are also considered part of the books and records. These serve as evidence to support the information recorded in the books and include receipts, statements, official agreements, work orders, shipping notices, purchase orders, and bank deposit slips.

Where Must Books and Records Be Kept?

All books and records must be kept at the charity's Canadian address on file with the CRA. This applies to records related to activities carried out both inside and outside of Canada.

A registered charity is not permitted to keep its books and records exclusively at a foreign address. However, charities using international cloud providers such as Google Drive, QuickBooks Online, or similar platforms are generally compliant under CRA Information Circular IC78-10R5, provided that records are accessible from Canada, stored in a readable and usable format, and can be produced to CRA auditors on demand at the Canadian place of business. The key requirement is that an accessible copy exists in Canada — not that the physical server must be located in Canada.

Charities with any uncertainty about their current cloud storage setup should seek legal advice to confirm compliance.

How Long Must a Charity Keep Its Books and Records?

The following retention periods apply to registered charities in Canada:

Note for dissolved corporations: Where a corporation is dissolved rather than having its registration revoked, certain records must be retained for two years following the date of dissolution.

Practical tip on donation receipts: While the Income Tax Regulations set a two-year minimum for duplicate receipts specifically, the CRA treats receipts as source documents subject to the six-year rule in broader audit practice. Retaining donation receipts for six years is the safest approach and the standard recommended by charity law practitioners.

Digital and Cloud Record-Keeping: What the CRA Accepts in 2026

Yes, charities may store their books and records electronically. However, several conditions apply.

Format requirements. Electronic records must be stored in a format that is accessible and readable — meaning the information can be processed and reviewed by CRA auditors using CRA equipment. Storing records in a proprietary format that cannot be opened or read by outside systems does not meet this standard.

Originally electronic records. If a document was created, transmitted, or received electronically — such as a digital contract or an email agreement — it must be preserved in its electronic format. Printing it and keeping only a paper copy is not sufficient.

Scanned paper documents. Scanned images of original paper documents are acceptable, provided that proper imaging practices are followed and documented. The charity should maintain records of when documents were scanned and by whom.

Cloud-based platforms. Tools such as QuickBooks Online, Xero, and Google Drive are commonly used by charities and are generally acceptable under CRA Information Circular IC78-10R5. These platforms are compliant as long as the records they contain are accessible from Canada, stored in a readable format, and can be produced to CRA auditors on demand at the Canadian place of business. However, if the software provider shuts down or changes its systems, the charity is responsible for ensuring records remain accessible for the full required retention period. Charities should keep offline backups of all critical records.

The foreign server clarification. A common misconception is that using a US-based or internationally hosted cloud service automatically puts a charity out of compliance. This is not accurate. CRA guidance under IC78-10R5 allows for records stored on foreign servers, provided the charity can produce an accessible copy in an electronically readable and usable format on demand at their Canadian place of business. What the CRA does not accept is a situation where records cannot be produced at all, or cannot be read in a standard format during an audit.

E-signatures and digital contracts. The CRA accepts e-signatures and digital agreements as source documents, provided they are stored in a readable electronic format and can be produced during an audit.

Who Is Responsible for Maintaining Books and Records?

The registered charity itself is always legally responsible for its books and records, even if it has hired a third party to manage them. Third parties may include bookkeepers, accountants, online transaction managers, or application service providers.

This means that if your bookkeeper fails to retain records properly, or your accounting software loses data, the liability falls on the charity — not the vendor. Charities should have written agreements in place with any third-party service providers that clearly set out record-keeping obligations, data ownership, and what happens to records if the relationship ends.

Best practices include:

- Keeping all books and records consolidated in one primary location for easy access during audits or board transitions

- Maintaining duplicates or backups at a separate, preferably off-site or secure cloud location

- Ensuring CRA officials can access records on request — they have the authority to inspect, audit, examine, and copy any records, including electronic ones

Common Record-Keeping Mistakes Canadian Charities Make

These are the most frequent compliance errors the CRA identifies in charity audits:

Keeping records with no accessible Canadian copy. Charities that store records exclusively on foreign servers without maintaining an accessible Canadian copy are at risk. It is not enough for records to exist on a cloud platform — they must be producible in a readable format at the Canadian place of business on demand.

Assuming the bookkeeper is responsible. Even if your charity outsources all its accounting and bookkeeping, the legal obligation for record-keeping compliance belongs to the charity. A CRA audit will hold the charity — not the third party — accountable for any gaps.

Not maintaining off-site backups. Many charities store records in a single location. If that location is damaged by fire, flood, or a data breach, records may be unrecoverable. The CRA expects charities to maintain duplicates at a secondary location.

Storing electronic records in unreadable formats. Records stored in outdated software formats, locked proprietary systems, or formats incompatible with CRA equipment do not meet the standard for electronic record-keeping.

Confusing accessibility with compliance on cloud storage. As noted above, records on foreign servers are not considered "kept in Canada" even if they can be accessed from a Canadian device.

Mixing charity and personal or business finances. Records that blend charitable funds with personal or non-charitable transactions make it extremely difficult to substantiate that resources were used for charitable purposes. This is a major audit red flag.

Not retaining donation receipts long enough. Some charities discard donation receipt copies after one year. While the regulatory minimum for duplicate receipts is two years, charities are advised to retain them for six years from the end of the relevant tax year, consistent with the source document rules that apply in practice.

Annual Record-Keeping Checklist for Registered Charities

Use this checklist each year to confirm your charity remains compliant with CRA record-keeping requirements.

Location and Storage

- ☐ All books and records are kept at the charity's Canadian address on file with the CRA

- ☐ Records related to foreign activities are also kept at or accessible from the Canadian address

- ☐ Off-site or secure cloud backups exist for all critical records

- ☐ Cloud storage meets CRA format and accessibility standards under IC78-10R5

- ☐ Records can be produced in a readable and usable format to CRA auditors on demand

Retention

- ☐ Donation receipt copies are retained for at least 6 years from the end of the relevant tax year

- ☐ 10-year gift records are retained for the full duration of registration plus at least 2 years post-revocation

- ☐ Board and members' meeting minutes are retained for the full duration of registration plus 2 years post-revocation

- ☐ Governing documents and bylaws are retained for the full duration of registration plus 2 years post-revocation

- ☐ General ledgers and financial records are retained for at least 6 years from the end of the relevant tax year

- ☐ T3010 copies are retained for at least 6 years from the end of the relevant tax year, plus 2 years post-revocation if applicable

Electronic Records

- ☐ All electronic records are stored in a CRA-readable format

- ☐ Originally electronic documents are preserved electronically, not only as printed copies

- ☐ Scanned paper documents have been imaged using proper imaging practices

Oversight and Access

- ☐ The charity (not just its bookkeeper) has reviewed its record-keeping practices in the past 12 months

- ☐ All records are consolidated and accessible in one primary location

- ☐ CRA officials could be given access to all records on request without significant delay

Frequently Asked Questions

What happens if a charity fails to maintain proper books and records?

If the CRA determines that a registered charity has not maintained adequate books and records, it can suspend the charity's ability to issue official donation receipts. In more serious cases, the CRA may revoke the charity's registered status entirely. Revocation means the charity loses its ability to issue tax receipts and may be subject to a revocation tax on its assets.

Can a Canadian charity store its records with a third-party bookkeeper or accountant?

Yes, but the charity remains fully responsible for compliance. Even when records are managed by a third party such as a bookkeeper, accountant, or online transaction manager, the legal obligation for proper record-keeping belongs to the registered charity. Charities should have a written agreement with any third-party provider covering record retention, data ownership, and what happens to records if the relationship ends.

Are cloud-based records acceptable to the CRA?

Yes. Under CRA Information Circular IC78-10R5, electronic records stored on foreign servers are acceptable provided they are accessible from Canada, stored in a readable and usable format, and can be produced to CRA auditors on demand at the Canadian place of business. Using platforms such as Google Drive or QuickBooks Online does not automatically put a charity out of compliance. The key issue is whether records can actually be produced and read when required.

How long must a charity keep its board meeting minutes?

Board, director, trustee, and executive meeting minutes must be retained for the full duration of the charity's registration, plus a minimum of two years after the charity's registration has been revoked. For corporations, the two-year period begins from the date of dissolution.

How long must donation receipts be kept?

While the Income Tax Regulations set a two-year minimum for duplicate receipts, charities are strongly advised to retain donation receipts for six years from the end of the relevant tax year. This aligns with the CRA's source document rules, which apply to receipts in broader audit practice.

Do record-keeping obligations continue after a charity loses its registered status?

Yes. Record-keeping obligations do not end when a charity's registration is revoked or when a corporation is dissolved. Charities must retain most records for at least two years after revocation or dissolution. Financial records and T3010 copies must be kept for six years from the end of the relevant tax year, plus two years post-revocation.

What are source documents, and are they required?

Source documents are records that support the information in a charity's books and records. They include receipts, bank statements, invoices, official agreements, work orders, shipping notices, purchase orders, and bank deposit slips. Yes, they are required. Source documents form part of the charity's books and records and are subject to the same retention requirements as other financial records — generally six years from the end of the relevant tax year.

Where must a charity keep its books and records?

Books and records must be kept at the charity's Canadian address as registered with the CRA, or be accessible and producible from that address. Charities using cloud storage on foreign servers are generally compliant under IC78-10R5, provided records can be produced in a readable format to CRA auditors on demand at the Canadian place of business.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)