How Canadian Charities Operate Outside the Shores Of Canada

Published on

May 26, 2021

Last updated on

February 9, 2026

The Canada Revenue Agency (CRA) regulates all registered charities in Canada, including their international operations. Under the Income Tax Act, Canadian charities can legally operate outside Canada, but must follow strict compliance requirements to maintain their charitable status.

Many Canadian charities seek to expand their impact beyond Canadian borders. Whether providing disaster relief, supporting international development, or addressing global challenges, these organizations must navigate complex regulatory requirements while ensuring their activities remain charitable under Canadian law.

The Income Tax Act recognizes the right of Canadian charities to conduct charitable operations both within and outside Canada. However, these international charity operations may only be carried out through specific approved methods, each with distinct compliance requirements.

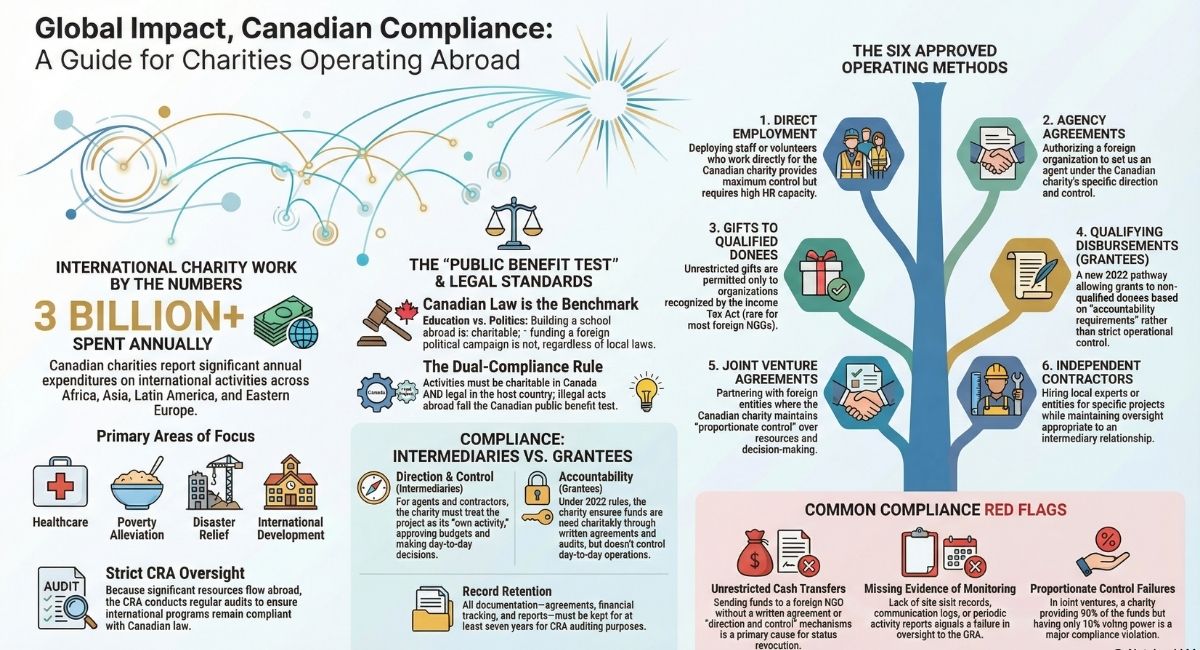

International Charity Work by the Numbers

According to recent CRA data, thousands of Canadian registered charities conduct international operations. Understanding the scope of this work helps contextualize the regulatory framework:

- Canadian charities report spending over $3 billion annually on international activities

- Common regions include Africa, Asia, Latin America, and Eastern Europe

- Typical activities include disaster relief, international development, education, healthcare, and poverty alleviation

- The CRA conducts regular audits of international programs to ensure compliance

These statistics demonstrate why the CRA maintains strict oversight of foreign operations – significant charitable resources flow internationally, and proper safeguards protect both donors and beneficiaries.

Legal Framework for International Charity Operations

Canadian charities operating internationally must comply with two fundamental legal requirements under the Income Tax Act:

Requirement 1: Use Approved Operating Methods

Charity operations abroad must be carried out through staff, agents, or intermediaries. This means the people selected to work for the charity internationally must be either bonafide employees or authorized agents of the Canadian charity.

Requirement 2: Restrict Gifts to Qualified Donees

Charities can only make unrestricted gifts to qualified donees. Qualified donees are organizations that can, under the Income Tax Act of Canada, issue official donation receipts that allow for tax credits (for individuals) or tax deductions (for corporations). Most foreign charities and NGOs do not fall in this category and are not regarded as qualified donees. This means Canadian charities cannot make unrestricted donations to most foreign organizations.

However, Canadian charities can transfer funds or assets to foreign organizations through two main pathways: (1) when the relationship is structured as an agency or intermediary arrangement where the Canadian charity maintains direction and control over resources, or (2) when making qualifying disbursements to grantees under the new rules introduced in 2022, which focus on accountability requirements rather than direction and control.

The Public Benefit Test for Foreign Activities

Before launching international operations, your charity must ensure activities meet the public benefit test under Canadian law. This critical requirement ensures that charitable activities performed by your charity are recognized as charitable under Canadian legal standards.

Why This Test Matters

Canadian courts have established that activities must be charitable under Canadian law to qualify for charitable status. The legal principle is clear: an activity that is legal in a foreign country but not charitable under Canadian law cannot be funded by a Canadian charity.

Example of Activities That Don't Transfer

It is charitable under Canadian law to increase the effectiveness and efficiency of Canada's armed forces. However, it is not charitable to support the armed forces of another country. Similarly, advocating for policy changes in Canada may be acceptable ancillary activity, but directly supporting foreign political campaigns would not meet the public benefit test under Canadian law, even if such activity is legal in the foreign country.

Practical Application

A Canadian charity focused on education can build schools in developing countries because education is recognized as charitable under Canadian law. However, that same charity cannot use funds to support a foreign political campaign, as this would not meet the public benefit test under Canadian law regardless of whether such activity is legal abroad.

Local Law Compliance

Your charity must also ensure compliance with the laws of the foreign country where you operate. If an activity is charitable under Canadian law but illegal in the host country, the charity cannot perform it because illegal acts are contrary to public policy and thus fail the Canadian public benefit test. Your international operations must not violate local regulations. Research local requirements thoroughly before establishing programs abroad.

Six Approved Structures for International Charity Work

A Canadian charity does not necessarily need to establish a legal presence abroad to operate internationally. The CRA recognizes six distinct structures through which Canadian charities can conduct foreign activities while maintaining compliance:

1. Direct Employment of Staff or Volunteers Abroad

Your charity can employ staff or deploy volunteers who work directly for the organization in foreign locations.

How It Works:

- Individuals are employees or authorized volunteers of the Canadian charity

- They carry out activities that align with your charity's registered purposes

- No transfer of funds to external foreign organizations occurs

- All expenditures are internal operational costs

Benefits:

- Maximum control over activities and resources

- Simpler compliance documentation

- Direct accountability through employment relationship

Considerations:

- Requires HR capacity to manage international employees

- May involve complex labor law and tax considerations

- Need for ongoing supervision and support systems

2. Agency Agreements with Foreign Organizations

Your charity can authorize an agent or agent organization to act on your behalf abroad.

How It Works:

- The Canadian charity enters a written agency agreement

- The agent carries out activities under your charity's direction and control

- You retain decision-making authority over how resources are used

- The agent reports regularly on activities and expenditures

Required Documentation:

- Comprehensive written agency agreement

- Detailed scope of authorized activities

- Reporting and monitoring requirements

- Financial controls and approval processes

Key Distinction: This is not a donation – it's an operational arrangement where your charity directs how funds are used to accomplish your charitable purposes through what the CRA classifies as an intermediary relationship.

3. Gifts to Qualified Donees

A Canadian charity can make unrestricted gifts to other qualified donees to support charitable causes.

How It Works:

- Transfer funds to another organization that holds qualified donee status

- The receiving organization uses funds for their own charitable purposes

- No direction and control requirements apply to unrestricted gifts

Important Limitation: Most foreign charities are not qualified donees under Canadian law. This structure typically applies only to:

- Other Canadian registered charities

- Certain international organizations with qualified donee status

- Limited categories of foreign charitable organizations specifically recognized in the Income Tax Act

When Restrictions Apply: If you want to restrict a gift to a particular location or specific cause, additional compliance requirements apply, and the arrangement may be reclassified as requiring direction and control.

4. Qualifying Disbursements to Grantees

Since June 23, 2022, Canadian charities can make "qualifying disbursements" by way of grants to "grantees" (non-qualified donees) without maintaining the strict direction and control requirements.

How It Works:

- Your charity makes a grant to a foreign organization (the "grantee") that is not a qualified donee

- Instead of direction and control, you must meet "accountability requirements"

- The grantee must use resources for a charitable purpose

- This method focuses on accountability and reporting rather than operational control

Key Difference from Agency Relationships:

- Direction and Control (Agency): Your charity effectively treats the project as its own activity and directs exactly how funds are used

- Accountability Requirements (Grantee): Your charity ensures funds are used for charitable purposes but does not control day-to-day operations

Accountability Requirements Include:

- Written agreement specifying the charitable purposes for which funds are granted

- Requirement that the grantee provide periodic reports on use of resources

- Right to conduct audits or site visits to verify appropriate use of funds

- Obligation to return unused funds or funds not used for charitable purposes

- Requirement that the grantee maintain books and records

When to Use This Method: This structure is particularly valuable when:

- You want to support established foreign organizations with expertise in their region

- The foreign organization has its own governance and programs

- You want to provide funding support without operational involvement

- You trust the grantee's capacity but need accountability

CRA Guidance: For detailed information about the grantee rules, consult CRA Guidance CG-032, "Registered charities making disbursements to grantees."

5. Joint Venture Agreements

Your charity can partner with a foreign charity to pool resources and work collaboratively toward shared charitable objectives.

How It Works:

- Both organizations contribute resources to a joint account or program

- Partners collaborate on shared charitable objectives

- Activities must align with both charities' purposes

- A legally binding agreement governs the relationship

Required Elements:

- Written joint venture agreement

- Clear definition of each party's contributions and responsibilities

- Governance structure for decision-making

- Procedures for financial management and reporting

- Exit provisions and asset distribution terms

Critical CRA Requirement - Proportionate Control:

Your Canadian charity must maintain a level of control that is proportionate to the resources it contributes. The CRA requires this to ensure your charity is carrying out its "own activities" rather than merely funding another organization.

Example:

- If your charity provides 90% of the funding for a joint venture, it must have decision-making authority proportionate to that contribution

- Having only 10% voting power when contributing 90% of resources would likely fail CRA scrutiny

- The CRA would view this as improperly funding another organization rather than conducting your own charitable activities

CRA Requirements:

Even in joint ventures, your Canadian charity must demonstrate that:

- Activities further your charitable purposes

- You exercise oversight proportionate to your contribution

- Resources are used for charitable activities

- Documentation supports the collaborative nature of the work while maintaining appropriate control

Source: CRA Guidance CG-002, Section 6.4 specifically addresses proportionate control in joint ventures.

6. Independent Contractors and Cooperative Participants

Your charity can contract with individuals, groups, or entities to work on specific projects or objectives. The CRA classifies these relationships as intermediary arrangements under the "own activities" test.

How It Works:

- The Canadian charity contracts services from an independent party

- Contractors provide specific expertise, knowledge, or regional experience

- The charity maintains oversight and approval authority appropriate to an intermediary relationship

- Contractors deliver defined services or outcomes

Cooperative Participant Agreements:

These legally binding agreements establish cooperation between your charity and another entity to work together on mutually agreed-upon projects. Both parties contribute resources or expertise, but your charity retains ultimate authority over its own resources, consistent with CRA requirements for intermediaries.

Independent Contractor Relationships:

Useful when your charity needs resources it cannot otherwise provide, such as:

- Specialized technical skills

- Local language capabilities

- Regional knowledge and cultural understanding

- Established relationships with beneficiary communities

CRA Classification: Under CRA Guidance CG-002, independent contractors are viewed as intermediaries alongside agents and joint venture partners. All intermediary relationships require that your charity demonstrate it is carrying out its "own activities" with appropriate direction and control.

Pre-Engagement Requirements:

Before contracting an intermediary or independent contractor, your charity must:

- Verify the contractor can carry out the required activities

- Ensure the contractor will use resources as directed

- Establish clear reporting and monitoring requirements

- Document the contractor's qualifications and track record

Direction and Control Requirements

When operating internationally through intermediaries (including agents, joint ventures, and independent contractors), Canadian charities must demonstrate ongoing direction and control over all resources and activities. This is the most critical compliance requirement for foreign operations conducted through the "own activities" pathway, and failure to meet these standards can result in serious consequences including loss of charitable status.

Note: The new grantee rules introduced in 2022 provide an alternative pathway focusing on accountability requirements rather than direction and control. See the "Qualifying Disbursements to Grantees" section above.

What the CRA Requires

The CRA requires specific, detailed documentation to prove your charity maintains direction and control when working through intermediaries:

Required Documentation Includes:

- Written Agreements: Comprehensive contracts specifying exactly how funds will be used, reporting requirements, and monitoring procedures

- Regular Activity Reports: Detailed updates from intermediaries describing activities conducted, beneficiaries served, and outcomes achieved

- Financial Tracking: Documentation showing all expenditures align with charitable purposes and approved budgets

- Evidence of Monitoring: Records of communications, site visits (when possible), and ongoing oversight activities

- Quarterly or Annual Reviews: Formal evaluations of international programs assessing effectiveness and compliance

What "Direction and Control" Means in Practice

Your charity must retain decision-making authority over how resources are used, even when working through intermediaries. This includes:

- Budget Approval: Your board or authorized officers approve detailed budgets before funds are transferred

- Program Design: Your charity determines what activities will be conducted and how they align with your charitable purposes

- Ongoing Oversight: Regular check-ins, progress reports, and course corrections as needed

- Financial Controls: Approval requirements for expenditures, documentation of how money was spent, and verification that spending aligns with approved plans

- Activity Monitoring: Tracking what activities actually occur, who benefits, and what outcomes are achieved

- Corrective Authority: The right and ability to redirect activities or withhold further funding if problems arise

What Does NOT Constitute Direction and Control

Simply transferring funds without oversight does not meet CRA standards. The following arrangements are insufficient:

- Unrestricted cash transfers with no reporting requirements

- Generic agreements without specific activity descriptions

- Passive receipt of occasional updates

- Reliance on the intermediary's judgment without your charity's approval

- Post-facto review of how money was spent

- Lack of documented communication or monitoring

Red Flags the CRA Looks For

During audits of international activities, CRA auditors specifically look for these compliance failures:

- Red Flag #1: Unrestricted cash transfers to foreign organizations without written agreements

- Red Flag #2: Lack of written agreements or agreements that don't specify direction and control mechanisms

- Red Flag #3: Missing activity reports or financial documentation

- Red Flag #4: No evidence of ongoing monitoring, such as site visits, regular communications, or program reviews

- Red Flag #5: Activities that deviate from the charity's stated purposes or the terms of agreements

- Red Flag #6: Inability to demonstrate what specific charitable activities were accomplished with transferred resources

- Red Flag #7: Transfers to organizations with potential terrorism financing concerns or operating in high-risk jurisdictions without enhanced due diligence

Documentation Best Practices

To ensure your charity can demonstrate direction and control (for intermediary relationships) or accountability (for grantee relationships):

Before Any Transfer:

- Execute comprehensive written agreements

- Approve detailed budgets and charitable purposes

- Establish reporting schedules and accountability mechanisms

During Operations:

- Collect regular reports

- Maintain communication logs

- Review financial statements

- Document any program modifications

After Activities Conclude:

- Obtain final reports

- Verify all funds were used appropriately

- Retain all documentation for at least seven years

Annual Review:

- Board or committee review of all international programs

- Assessment of compliance with agreements

- Evaluation of effectiveness

Common Compliance Mistakes to Avoid

Based on CRA audits and compliance reviews, these are the most frequent mistakes Canadian charities make when operating internationally:

Mistake #1: Treating Foreign Partners as Qualified Donees

The Problem: Most foreign charities are not qualified donees under Canadian law. Transferring unrestricted funds to them as if they were qualified donees violates the Income Tax Act.

The Consequence: The CRA may impose penalties, require repayment of improperly transferred funds, or revoke charitable status in serious cases.

The Solution: Always structure relationships with foreign organizations as agency agreements with clear direction and control requirements. Never make unrestricted transfers to organizations that aren't qualified donees.

Mistake #2: Inadequate Documentation

The Problem: Charities fail to maintain comprehensive records of agreements, monitoring activities, financial tracking, and compliance verification.

The Consequence: During CRA audits (which can occur years after activities conclude), charities cannot prove they maintained direction and control. The CRA may disallow expenses, assess penalties, or revoke charitable status.

The Solution: Maintain detailed records including:

- Original signed agreements

- All activity and financial reports

- Communication logs

- Evidence of monitoring and oversight

- Board minutes documenting approval and review of international programs

Retain all documentation for at least seven years, as required by CRA regulations.

Mistake #3: Assuming Charitable Status Transfers Across Borders

The Problem: Charities assume that activities charitable in Canada are automatically charitable everywhere, or that activities legal in foreign countries are automatically acceptable for Canadian charities.

The Consequence: Your charity may fund activities that don't meet the public benefit test under Canadian law, jeopardizing compliance.

The Solution: Before expanding internationally:

- Ensure proposed activities meet charitable definitions under Canadian law

- Understand that activities must be charitable under Canadian legal standards, not just legal in the foreign country

- Verify compliance with local regulations (illegal acts fail the public benefit test even if charitable in nature)

- Consult with legal experts familiar with Canadian charity law

- Document your legal analysis

Mistake #4: Failing to Monitor Intermediaries

The Problem: After signing an agreement and transferring funds, charities fail to actively monitor how intermediaries use resources.

The Consequence: Without ongoing oversight, you cannot demonstrate direction and control. Resources may be misused, and your charity remains legally responsible.

The Solution: Implement active monitoring through:

- Regular scheduled reports (monthly or quarterly)

- Site visits when feasible

- Financial reviews and audits

- Ongoing communication with intermediaries

- Annual program evaluations

- Immediate investigation of any concerns

Mistake #5: Operating Without Legal Review

The Problem: Charities launch international operations without consulting charity law specialists, relying on general advice or assumptions.

The Consequence: Compliance failures that could have been prevented through proper legal guidance, potentially resulting in CRA penalties or revocation.

The Solution: Before launching foreign operations:

- Consult with charity lawyers experienced in international compliance

- Have agreements professionally drafted and reviewed

- Develop comprehensive policies for international activities

- Train board members on their governance responsibilities

- Establish compliance monitoring systems

Mistake #6: Insufficient Due Diligence on Partners

The Problem: Charities don't adequately vet foreign organizations before entering partnerships or agency relationships.

The Consequence: Your charity may inadvertently partner with organizations involved in terrorism financing, corruption, or activities incompatible with charitable purposes.

The Solution: Conduct thorough due diligence including:

- Verification of partner organization's legal status

- Background checks on key personnel

- Review of financial statements and governance documents

- Assessment of reputation and track record

- Screening against terrorism financing lists

- Understanding of local political and security context

Mistake #7: Unclear Governance Authority

The Problem: Boards don't clearly authorize international operations or establish appropriate oversight mechanisms.

The Consequence: Staff may enter agreements or transfer funds without proper authority, creating governance failures and compliance risks.

The Solution: Ensure your board:

- Formally approves international operations through minuted resolutions

- Establishes clear delegation of authority for international programs

- Reviews international activities at least annually

- Approves significant agreements and budget allocations

- Understands their fiduciary duties for foreign operations

Mistake #8: Confusion Between Direction and Control vs. Accountability

The Problem: Charities don't understand the difference between the direction and control requirements for intermediaries and the accountability requirements for grantees introduced in 2022.

The Consequence: Using the wrong compliance framework for a relationship, leading to insufficient documentation and CRA penalties.

The Solution:

- Understand that direction and control applies when using intermediaries (agents, contractors, joint ventures)

- Recognize that accountability requirements apply when making qualifying disbursements to grantees

- Choose the appropriate structure based on your desired relationship with the foreign organization

- Document compliance using the correct framework

- Consult CRA Guidance CG-002 (for intermediaries) and CG-032 (for grantees)

Get Expert Guidance for International Charity Operations

Operating a Canadian charity abroad introduces complex legal, tax, and compliance requirements that demand specialized expertise. The CRA's direction and control standards are stringent, and mistakes can jeopardize your charitable status.

Before launching international programs, Canadian charities should:

1. Review Governing Documents

Confirm your articles of incorporation and bylaws permit international work and that proposed activities align with your registered charitable purposes.

2. Develop Comprehensive Policies

Create detailed policies governing international operations, including approval processes, monitoring requirements, financial controls, and risk management procedures.

3. Create Robust Documentation Systems

Establish systems for maintaining all required records, tracking direction and control, and demonstrating compliance with CRA requirements.

4. Consult Charity Law Specialists

Work with lawyers experienced in international charity compliance to review your plans, draft compliant agreements, and ensure your documentation meets CRA standards.

Need Help Navigating CRA Requirements for International Charity Work?

B.I.G. Charity Law Group specializes in helping Canadian charities expand globally while maintaining full compliance with CRA regulations. Our charity lawyers can:

- Review your international program plans and governance structure

- Draft compliant agency agreements, joint venture agreements, and contractor arrangements

- Ensure your documentation demonstrates proper direction and control

- Advise on the public benefit test for your specific activities

- Conduct legal reviews of your international operations

- Represent you in CRA audits or compliance reviews

For more detailed information about international charity operations, visit the CRA's guidance on foreign activities.

Contact us at 416-488-5888 or book a free consultation to discuss your charity's international operations and ensure you're meeting all CRA compliance requirements.

Frequently Asked Questions About Canadian Charities Operating Abroad

Can a Canadian charity donate directly to a foreign charity?

No, in most cases. Foreign charities are typically not qualified donees under the Income Tax Act, which means Canadian charities cannot make unrestricted donations to them. However, you can transfer funds to foreign organizations if the relationship is structured as an agency agreement where your charity maintains direction and control over how the funds are used. The key distinction is that this is not a donation – it's your charity using an agent to carry out your own charitable purposes.

Do we need CRA approval before operating internationally?

No pre-approval from the CRA is required before launching international operations. However, your charity must ensure all international activities align with your registered charitable purposes as stated in your governing documents and meet the CRA's direction and control requirements. Document everything thoroughly, as the CRA may audit these activities during routine compliance reviews or in response to specific concerns. While pre-approval isn't required, consulting with charity law specialists before launching foreign operations is strongly recommended.

What's the difference between an intermediary and a grantee?

Intermediary (Agent, Contractor, or Joint Venture Partner):

- Works under your charity's direction and control to carry out your charitable purposes abroad

- You retain decision-making authority over day-to-day operations

- Requires detailed direction and control documentation

- You effectively treat the project as your own activity

Grantee (Since 2022):

- Receives a grant from your charity for charitable purposes

- Operates with independence but meets accountability requirements

- You ensure funds are used for charitable purposes but don't control operations

- Focuses on reporting and accountability rather than operational control

The relationship structure determines what documentation and oversight you must maintain. Choose based on whether you want operational control (intermediary) or funding support with accountability (grantee).

What's the difference between a grantee and a qualified donee?

Qualified Donee:

- Has specific legal status under the Income Tax Act

- Can issue official donation receipts for tax credits/deductions

- Can receive unrestricted gifts from your charity

- No direction, control, or accountability requirements

- Most foreign organizations do NOT qualify

Grantee:

- Does not have qualified donee status

- Cannot issue tax receipts

- Receives grants with accountability requirements

- Must report on use of funds and meet charitable purposes

- Provides way to fund most foreign organizations that aren't qualified donees

The 2022 grantee rules essentially created a middle ground between unrestricted gifts to qualified donees and the strict direction and control required for intermediaries.

Can we hire local staff in the foreign country?

Yes, hiring employees abroad is one of the five CRA-approved methods for international operations. These employees work directly for your Canadian charity and must carry out activities that align with your registered charitable purposes. You'll need to navigate local employment law, tax obligations, and potentially immigration requirements depending on the country. This structure provides maximum control since employees work under your direct supervision, though it requires HR capacity to manage international personnel effectively.

What happens if we don't maintain proper compliance?

Failure to maintain the required compliance standards—whether direction and control for intermediaries or accountability for grantees—can result in serious consequences:

- The CRA may impose financial penalties

- Require repayment of funds that were improperly transferred

- Reclassify expenditures as non-charitable (making them taxable)

- In severe cases, revoke your charitable status entirely

The CRA takes these requirements very seriously because they prevent misuse of charitable resources and ensure funds actually accomplish charitable purposes rather than being diverted.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)