How to Create a Not-for-Profit Corporation in Canada

Published on

October 26, 2023

Last updated on

April 18, 2026

To create a not-for-profit corporation in Canada, you must file Articles of Incorporation with either the federal government or your provincial government. The choice depends on where you plan to operate.

The process involves choosing a unique name, appointing directors, and establishing bylaws that govern how your organization will run. While the steps may seem complex at first, understanding the requirements makes the process much more manageable.

This guide covers everything from understanding the legal requirements to securing funding for your new organization. You'll learn about the differences between federal and provincial incorporation, how to obtain charitable status for tax benefits, and the ongoing responsibilities that come with running a not-for-profit corporation. By the end, you'll have a clear roadmap to turn your vision into a legally recognized organization.

Understanding Not-for-Profit Corporations in Canada

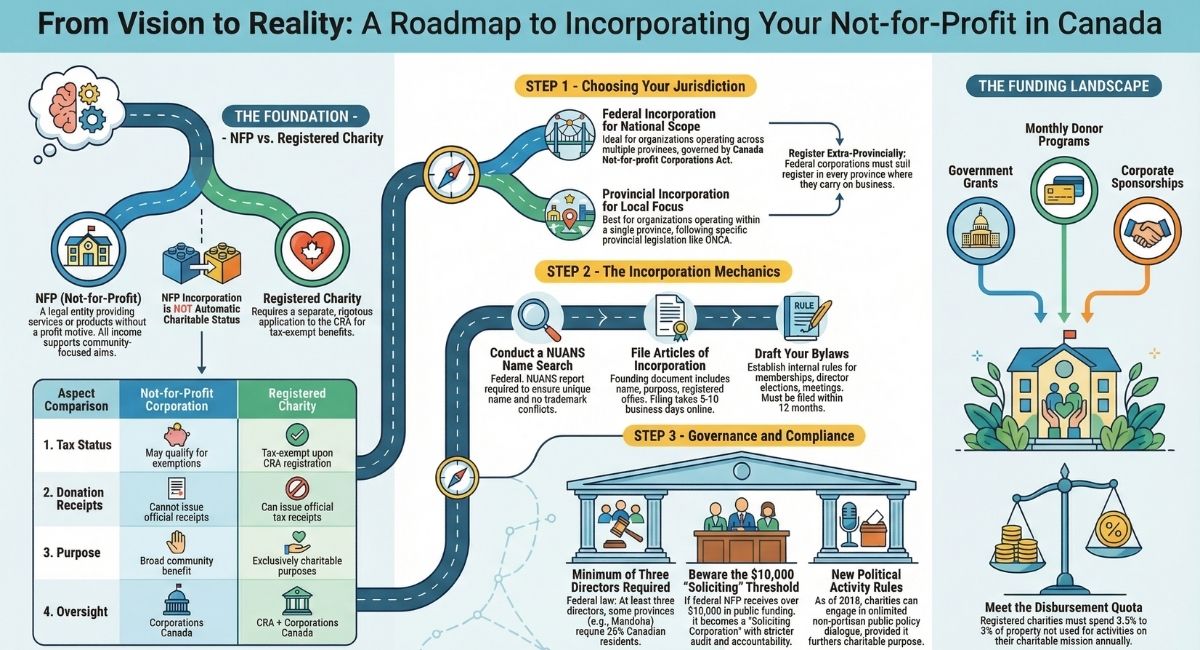

Not-for-profit corporations in Canada serve community interests rather than generate profit for shareholders. These organizations operate under federal or provincial laws and can pursue charitable, educational, or social purposes. They have distinct legal differences from registered charities.

Legal Definition and Purpose

A not-for-profit corporation is a legal entity that provides products or services without the primary goal of making profit. Under the Canada Not-for-profit Corporations Act (NFP Act), these organizations must dedicate their activities to improving or benefiting a community.

Not-for-profit corporations can generate revenue. However, any income must go back into the organization to support its aims and projects. This requirement ensures the corporation serves its stated purpose instead of enriching individuals.

The Not-for-Profit Act governs federally incorporated not-for-profit corporations. This legislation allows organizations to operate across all provinces and territories in Canada. Part 2 of the Not-for-Profit Act outlines the incorporation process and requirements.

Key legal characteristics include:

- Separate legal entity status

- Limited liability protection for directors and members

- Ability to enter contracts and own property

- Perpetual existence beyond founding members

Types of Not-for-Profit Organizations

Not-for-profit corporations can serve various purposes and take different forms. Common types include educational, charitable, religious, and community service organizations.

Educational organizations focus on learning and knowledge sharing. These include schools, training institutes, and research foundations.

Charitable organizations work to relieve poverty, advance education, promote health, or benefit communities. They can qualify for registered charity status with tax benefits.

Religious organizations serve spiritual communities and promote religious activities. Incorporation gives them legal recognition and operational structure.

Community service organizations address local needs through housing, recreation, or social services. These corporations often partner with government agencies to deliver public benefits.

Professional associations can also incorporate as not-for-profit corporations. However, incorporation does not grant authority to regulate professional practice.

Not-for-Profit vs. Charity: Key Differences

Understanding the difference between not-for-profit corporations and registered charities helps you choose the right structure for your organization.

Not-for-profit incorporation under the Not-for-Profit Act does not automatically provide tax-exempt status. Organizations must apply to the Canada Revenue Agency (CRA) for tax exemptions or charitable registration.

Registered charities must operate exclusively for charitable purposes as defined by the Income Tax Act. They can issue official donation receipts. Upon successful registration with the CRA, they receive tax-exempt status. The registration process requires meeting CRA requirements.

If you plan to seek charitable status, review CRA requirements before preparing incorporation documents. Changes to articles after incorporation require amendments and extra fees.

Key Steps to Incorporate a Not-for-Profit Corporation

The incorporation process involves three key actions: choosing between federal and provincial incorporation, selecting a name, and preparing your articles of incorporation. Each step requires careful consideration to ensure your organization meets legal requirements and can operate effectively.

Choosing a Structure: Federal vs Provincial Incorporation

Decide whether to incorporate federally under the Canada Not-for-profit Corporations Act or provincially under your province's legislation. This choice affects where your organization can operate and which regulations it must follow.

Federal incorporation allows your corporation to operate across all Canadian provinces and territories. You'll work with Corporations Canada and follow federal regulations. This option works well if you plan to operate nationally or in multiple provinces.

Provincial incorporation limits your operations to one province initially. Each province has its own incorporation process and requirements. For example, Ontario uses the Ontario Not-for-Profit Corporations Act (ONCA), while Manitoba uses the Corporations Act (Manitoba).

Federal incorporation offers broader operational scope and easier expansion into other provinces. However, it's important to note that federal name protection, while the strongest available, does not automatically override prior-existing trademarks or well-established provincially incorporated names. Additionally, federal corporations must still register extra-provincially in every province where they carry on business, which may involve a separate name search in that province.

Provincial incorporation may be simpler if you only plan to operate locally. Requirements and fees can vary between provinces. Some provinces offer faster processing times or lower costs.

Consider your long-term goals when making this choice. If you're unsure about future expansion, federal incorporation provides more flexibility.

Selecting a Name and Name Search Process

Every not-for-profit corporation needs a distinct name that legally identifies the organization. The name appears in your articles of incorporation and must meet specific requirements.

Your name must be unique and not confuse the public with existing organizations. It should reflect your organization's purpose clearly. Avoid names that suggest commercial activities if you plan to register as a charity.

Name search requirements vary by jurisdiction. For federal incorporation, you'll need a NUANS (Newly Upgraded Automated Name Search) report. This report shows similar names already in use and helps prevent conflicts.

Federal not-for-profit corporations may include legal endings such as "Corporation," "Incorporated," or their abbreviations. However, under the Not-for-Profit Act, organizations can also operate without these legal endings if their activities are clearly not for profit. Some provinces have different requirements for not-for-profit organizations.

Reserve your chosen name if it's available. Name reservations usually last 90 days, giving you time to complete your incorporation documents. The reservation fee is separate from incorporation costs.

Consider alternative names in case your first choice isn't available. Backup options prevent delays in the process.

Drafting and Filing Articles of Incorporation

The articles of incorporation serve as your corporation's founding document. This legal document establishes your organization's existence and outlines its basic structure and purpose.

Key components include your corporation's name, registered office address, and purpose statement. You'll also specify the number of directors and any membership classes. The language can be English, French, or bilingual depending on your preference.

Draft your purpose statement carefully, especially if you plan to register as a charity later. The Canada Revenue Agency has specific requirements for charitable purposes.

For federal corporations, the registered office must be located in the province specified in your Articles of Incorporation. You cannot incorporate a federal not-for-profit and later move the head office to a different province without amending your Articles (using Form 4004). For provincial corporations, the registered office must be in the incorporating jurisdiction. This address receives official correspondence and legal documents.

The filing process can be completed online for federal incorporation through Corporations Canada's website. You'll pay the incorporation fee and submit your completed articles. Processing usually takes 5-10 business days for online applications.

Provincial filing processes vary by jurisdiction. Some provinces offer online filing, while others require paper submissions. Check your province's specific requirements and processing times.

Review your articles carefully before submission. Changes after incorporation require amendments, which involve extra fees and processing time.

Establishing Governance and Operations

Once your not-for-profit corporation receives its certificate of incorporation, you must establish governance structures and create bylaws to guide operations. Directors need clear roles and responsibilities to ensure effective leadership and compliance with regulations.

Appointing the Board of Directors

The Canada Not-for-profit Corporations Act requires every corporation to have at least three directors. Select individuals who bring diverse skills and share your organization's mission.

Directors must be at least 18 years old and mentally competent. For federal incorporation, as of current federal law, there is no residency requirement for directors—all directors may be non-residents of Canada. This also applies in Ontario under the Ontario Not-for-Profit Corporations Act (ONCA) as of July 5, 2021.

However, provincial requirements vary. For example, under the Corporations Act (Manitoba), at least 25% of directors must be residents of Canada. Check your specific provincial legislation for director residency requirements if incorporating provincially.

Consider appointing directors with expertise in:

- Financial management and accounting

- Legal affairs and compliance

- Strategic planning and governance

- Fundraising and community relations

Directors serve terms specified in your bylaws, usually one to three years. Plan for staggered terms to maintain continuity.

Understanding Soliciting vs. Non-Soliciting Corporations

An important distinction under the Not-for-Profit Act is between soliciting and non-soliciting corporations. If your federal not-for-profit receives more than $10,000 in public or government funding in a single year, it becomes a "Soliciting Corporation."

This designation triggers additional requirements:

- At least three directors, with at least two who are not officers of the corporation - Stricter financial audit or review requirements - Enhanced accountability standards

Even if you don't initially expect to receive significant public funding, it's wise to structure your governance with these requirements in mind to avoid complications later.

Developing Corporate Bylaws

Bylaws establish the internal rules for operating your corporation. The Not-for-Profit Act requires bylaws to be created at the first directors' meeting and confirmed by members within 12 months.

Corporations Canada provides a Bylaw Builder online tool to help create customized bylaws.

Your bylaws must address:

- Membership classes and voting rights

- Director election procedures and terms

- Meeting requirements and quorum rules

- Financial management and signing authority

- Amendment procedures

Bylaws don't need filing with your incorporation application. However, you must file them within 12 months after member confirmation.

Roles and Responsibilities of Directors

Directors hold responsibility for your corporation's stewardship and must act in its best interests. They make strategic decisions and ensure compliance with legal obligations.

Key director duties include:

- Fiduciary duty: Act honestly and in good faith

- Duty of care: Exercise reasonable skill and diligence

- Oversight responsibility: Monitor organizational performance

Directors approve budgets, financial statements, and major policy changes. They hire and evaluate senior management and ensure proper internal controls exist.

The board typically elects officers including a president, secretary, and treasurer. Officers handle day-to-day management duties as delegated by the board.

Directors can be held personally liable for certain corporate debts if they fail to meet their legal obligations.

Applying for Incorporation and Legal Requirements

The incorporation process involves submitting your completed application to Corporations Canada and maintaining compliance with federal regulations. You must file specific documents and meet continuous reporting obligations once your corporation is established.

Filing the Incorporation Application

The incorporation process can be completed online through Corporations Canada's website. This is the fastest and easiest method.

The Articles of Incorporation form the core of your application. You must include your corporation's name, registered office address, and statement of purposes.

Your articles can be filed in English, French, or both official languages. You can choose the format that best serves your organization's needs.

Professional associations face special considerations. Incorporation doesn't grant authority to practise or regulate professions, so you must comply with provincial professional laws separately.

The filing fee varies by province or territory. You pay this fee when submitting your online application.

Once approved, you receive a Certificate of Incorporation. This document officially creates your not-for-profit corporation as a legal entity.

Regulatory Requirements and Ongoing Compliance

Directors must create bylaws at the first organizational meeting. These internal rules govern how your corporation operates day-to-day.

You can use Corporations Canada's Model bylaws or their online Bylaw builder tool. These resources make the process easier for most not-for-profit corporations.

Important deadline: You must file confirmed bylaws within 12 months after members approve them.

You have ongoing reporting obligations to Corporations Canada. These include annual returns and updates to corporate information.

Tax registration requires separate steps. Incorporation does not automatically make you tax-exempt or qualify you as a registered charity under the Income Tax Act.

If you plan to become a registered charity, review Canada Revenue Agency requirements before incorporating. Your statement of purposes must meet CRA standards for charitable registration.

You must also register your federal corporation in the province or territory where you operate.

Obtaining Charitable Status and Tax Benefits

Not-for-profit corporations can apply to the Canada Revenue Agency for charitable status. This allows organizations to issue official donation receipts and access tax exemptions. The process requires meeting specific criteria. Application review usually takes 6 to 18 months.

Applying to the Canada Revenue Agency for Charitable Status

Charitable status is not automatic when you create a not-for-profit corporation. The Canada Revenue Agency requires organizations to operate only for charitable purposes.

The application process follows four main steps. First, decide if your organization should pursue charitable status. Second, set up your legal entity properly before applying.

Required Documentation:

- Articles of incorporation

- Organizational bylaws

- Detailed description of activities

- Financial projections

- Governance structure information

The third step is to submit the formal application with all required documents. The Application to Register a Charity is now a digital-only submission via the CRA's My Business Account (MyBA). Paper applications are generally no longer accepted unless a specific digital barrier exists. Finally, the CRA reviews your application in detail.

Your organization must show one of four charitable purposes: relief of poverty, advancement of education, advancement of religion, or other purposes that benefit the community. You need to show that all activities directly support these charitable purposes.

During the review, the CRA may request more information or clarification about your activities and governance structure.

Tax Benefits and Obligations of Registered Charities

Once you obtain charitable status through successful CRA registration, your organization gains significant tax advantages. Registered charities become exempt from paying income tax on their charitable activities and can issue official donation receipts to donors.

Key Tax Benefits:

- Exemption from income tax upon successful registration

- Ability to issue tax-deductible donation receipts

- Eligibility for certain government grants

- Access to foundation funding opportunities

Charitable status comes with strict obligations. You must file annual returns with the CRA and keep detailed financial records.

Important: Political Activity Rules Have Changed. As of 2018, registered charities may engage in unlimited non-partisan "Public Policy Dialogue and Development Activities" (PPDDAs), provided these activities directly further the charity's stated purposes. The only absolute prohibition is on direct or indirect partisan political activity (supporting or opposing a candidate or party). The old "10% rule" no longer applies.

Your organization must spend a minimum amount on charitable activities each year, known as the disbursement quota. Current rates (as of 2023/2024) apply to property not used directly in charitable activities or administration:

- 3.5% for the first $1 million of such property

- 5% for the portion of such property exceeding $1 million

This ensures that donated funds support your charitable purposes instead of accumulating indefinitely.

If you fail to meet these requirements, you risk penalties or losing charitable status. You should consult legal or accounting professionals to stay compliant with all CRA requirements.

Securing Funding and Grants for Not-for-Profits

Funding your not-for-profit corporation requires a strategic approach. Organizations can combine government grants with other fundraising methods. You can access federal, provincial, and municipal funding programs. Building sustainable revenue also depends on community engagement and partnerships.

Identifying Government Grants and Financial Assistance

Government grants are a major funding source for Canadian not-for-profit corporations. Federal agencies offer grants for sectors like health, education, and social services.

Explore federal grant programs through agencies such as Employment and Social Development Canada and the Canada Revenue Agency. These programs often support community development, skills training, and charitable initiatives.

Provincial and municipal governments provide substantial funding opportunities. Each province has its own grant databases and application processes. Research eligibility criteria carefully. Requirements vary significantly between programs.

Common government funding types include:

- Operating grants for day-to-day expenses

- Project-based funding for specific initiatives

- Capital grants for equipment and infrastructure

- Capacity-building funds for organizational development

You must keep detailed financial records and show measurable impact to secure ongoing government support. Grant applications usually need project plans, budgets, and evaluation frameworks.

Fundraising Strategies for Not-for-Profits

Organizations need diverse fundraising strategies to ensure financial stability. Individual donations form the backbone of many not-for-profit funding models.

Corporate sponsorships offer valuable partnerships. Businesses support your mission while meeting their corporate social responsibility goals. Prepare clear proposals that show mutual benefits and community impact.

Effective fundraising methods include:

- Monthly donor programs for predictable revenue

- Major gift campaigns targeting significant contributors

- Community fundraising events like galas and charity runs

- Online crowdfunding through social media platforms

- Membership fees for ongoing services or benefits

In-kind donations of goods, services, or expertise can reduce operating costs. Professional services, meeting spaces, and equipment donations provide value without cash transactions.

Consider joining not-for-profit networks and associations. These connections lead to funding opportunities, partnerships, and shared resources that strengthen your financial position.

Conclusion

Creating a not-for-profit corporation in Canada involves several important steps, from choosing the right name to filing your incorporation documents. It's crucial to pay close attention to legal requirements and maintain compliance with government regulations.

Don't forget to prepare your bylaws within 12 months of incorporation and consider charitable registration if you want tax-exempt status. Consulting a legal professional can help you avoid common pitfalls and set up your organization correctly from the start.

At B.I.G. Charity Law Group, we help organizations navigate the incorporation process with confidence. Our team understands Canadian not-for-profit law and can guide you through each step. Visit us to learn how we can support your mission and ensure your corporation starts on solid legal ground.

Frequently Asked Questions

Starting a not-for-profit corporation in Canada means understanding federal incorporation laws. Costs range from basic filing fees to legal consultation expenses. The structure prevents for-profit ownership but offers tax exemptions and charitable status benefits.

How to start a not-for-profit in Canada?

Begin by incorporating under the Canada Not-for-profit Corporations Act. The fastest way is to submit your application online through Corporations Canada. You'll need to choose a name, prepare your documents, and appoint at least three directors.

What is a not-for-profit organization in Canada?

A not-for-profit corporation is a legal entity under the Canada Not-for-profit Corporations Act that operates for charitable, educational, cultural, or community purposes rather than profit. It has separate legal status from its members, can own property and enter contracts, but must apply separately to CRA for tax-exempt status.

How much does it cost to register a non-profit in Canada?

Costs include basic filing fees (varies by province), optional name search fees, potential legal consultation fees (hundreds to thousands), possible amendment fees, and required annual filing fees to maintain good standing.

Can a for-profit own a nonprofit in Canada?

No. Not-for-profit corporations cannot have shareholders or distribute profits. Members have participation rights but not ownership rights, and directors cannot receive financial benefits, ensuring tax-exempt status is maintained.

What are the benefits of a non profit organization in Canada?

Benefits include potential tax exemption upon CRA registration, ability to issue donation receipts if registered as a charity, legal protection for members and directors, credibility with funders, and ability to operate across all provinces and territories with federal incorporation.

How does the Canada Not-for-profit Corporations Act impact the formation and functioning of not-for-profits?

The Act (which replaced the Canada Corporations Act in 2011) governs federal not-for-profits by setting incorporation requirements, outlining director duties and member rights, establishing governance frameworks, mandating annual reporting, and providing procedures for amending corporate documents.

Embed this infographic on your site:

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)