How Do You Apply for Charitable Status in Canada?

Published on

March 26, 2025

Last updated on

July 24, 2026

Starting a charity in Canada means getting official status from the government. Many people want to help their communities but don't know how to make their organization official.

Applying for charitable status in Canada involves a four-step process through the Canada Revenue Agency: making an informed decision, setting up your organization, submitting your application, and going through the review process.

Charitable status gives your organization important benefits like tax exemptions and the ability to issue donation receipts. However, the process can seem complicated with many forms and rules to follow.

We'll walk you through the requirements and help you prepare the right documents.

Understanding what makes an organization qualify for charitable status is the first step. We'll cover eligibility rules, required paperwork, and ongoing duties you'll have once you become a registered charity.

This guide will help you navigate each part of the application process with confidence.

Understanding Charitable Status in Canada

In Canada, obtaining charitable status is essential for organizations that want to issue official donation receipts and access tax benefits. To qualify, organizations must meet specific requirements set by the Canada Revenue Agency (CRA). This guide walks you through the charitable status application process and what you need to know before applying.

What Is a Registered Charity in Canada?

A registered charity is an organization approved by the CRA that operates exclusively for charitable purposes. These purposes generally fall under four categories:

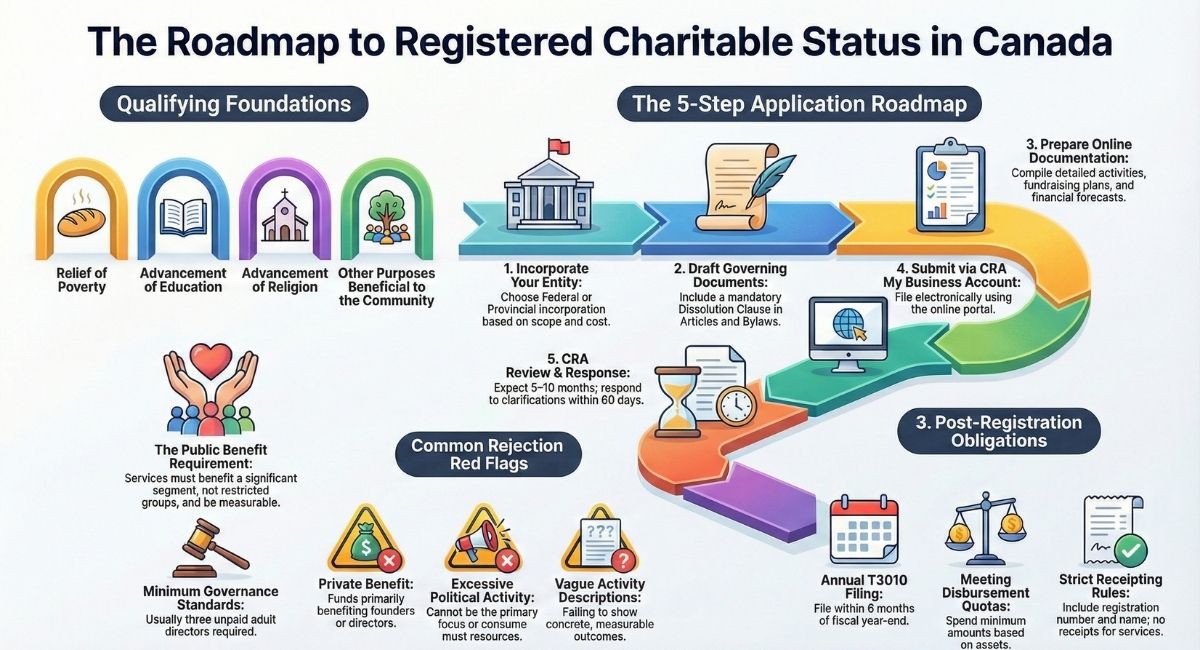

- Relief of poverty – Example: food banks, homeless shelters.

- Advancement of education – Example: scholarship programs, educational workshops.

- Advancement of religion – Example: places of worship, religious missions.

- Other purposes beneficial to the community – Example: environmental conservation, arts, animal rescue and cultural education programs.

Once registered, a charity can issue official donation receipts, apply for tax-exempt status, and receive grants from other charities or the government.

Who Can Apply for Charitable Status in Canada?

To qualify for charitable status, an organization must:

- Be established as a nonprofit or corporation.

- Have exclusively charitable purposes and activities that benefit the public.

- Ensure that no personal or private benefits arise from its activities.

- Follow strict record-keeping and governance guidelines.

If your organization meets these criteria, you can proceed with the charitable status application.

Eligibility Criteria for Charitable Registration

Organizations must meet specific requirements set by the Canada Revenue Agency to qualify for charitable registration. These requirements focus on having recognized charitable purposes, providing public benefit, and avoiding activities that could disqualify the organization.

Charitable Purposes Recognized by the CRA

The CRA recognizes four main categories of charitable purposes under Canadian law. These categories form the foundation of all charitable registration decisions.

Relief of poverty includes providing basic necessities like food, shelter, clothing, or medical care to those in need. Organizations must show they help people who cannot afford these essentials.

Advancement of education covers activities that promote learning and knowledge. This includes schools, libraries, research organizations, and programs that teach specific skills or subjects.

Advancement of religion supports religious worship, teaching, and spiritual guidance. Organizations must have clear religious beliefs and practices that benefit their community.

Purposes beneficial to the community is the broadest category. It includes health care, environmental protection, arts and culture, and community development projects.

Your organization must fit clearly into at least one of these four categories. Mixed purposes are allowed if they all qualify as charitable.

The Public Benefit Requirement

All charitable organizations must provide tangible benefits to the public or a significant portion of it. The benefit must be clear, measurable, and available to people beyond the organization's members.

Public access means your services cannot be restricted to a small, private group. You can focus on specific populations like seniors or students, but the group must be large enough to constitute a public benefit.

Measurable benefit requires you to show how your work helps people. The CRA looks for concrete outcomes, not just good intentions.

Private benefit is strictly limited. Your organization cannot primarily benefit its founders, directors, or their families through salaries, contracts, or other payments.

The benefit must also be legal and align with Canadian public policy. Activities that conflict with Canadian laws or values will not qualify.

Qualified Donee Status

Charitable registration automatically grants qualified donee status under the Income Tax Act. This status allows your organization to issue official donation receipts for tax purposes.

Donation receipts can only be issued by qualified donees. This makes your organization more attractive to donors who want tax deductions.

Investment income from your charitable activities may be tax-exempt. This includes interest, dividends, and capital gains on investments held for charitable purposes.

You must keep detailed records of all donations received. The CRA requires specific information about donors and donation amounts.

Qualified donee status also allows you to receive gifts from other registered charities and qualified donees.

Common Disqualifying Factors

Several factors can prevent charitable registration or cause the CRA to revoke existing status. These restrictions protect the integrity of Canada's charitable sector.

Political activities beyond permitted limits will disqualify your organization. Charities can engage in some political advocacy, but it cannot be their primary focus or consume most of their resources.

Private benefit to founders, directors, or related parties is strictly prohibited. This includes excessive salaries, personal use of charity property, or business deals that benefit insiders.

Illegal activities of any kind will result in immediate disqualification. Your organization must operate within all federal, provincial, and municipal laws.

Non-charitable purposes mixed with charitable ones can cause problems. Business activities, social clubs, and political parties do not qualify for charitable status.

Poor governance and financial management also raise red flags with the CRA during the review process.

Preparing Your Organisation for Application

Before applying for charitable status, your organisation must establish proper legal structure and governance. The Canada Revenue Agency requires specific governing documents, appropriate organisational structure, and qualified board members to process your application.

Governing Documents and Foundational Steps

Your organisation needs proper governing documents before applying for charitable status with the CRA. These documents prove your organisation exists as a legal entity and outline how it operates.

Articles of incorporation serve as your primary foundational document. They must include your organisation's name, purpose, and basic structure.

The articles create your organisation as a legal entity under provincial or federal law. Your constitution provides detailed rules about how your organisation operates, covering membership, meetings, voting procedures, and governance structures.

Some provinces combine articles and constitution into one document. We must ensure these governing documents clearly state charitable purposes.

The CRA reviews these documents to confirm your organisation meets charitable requirements. Vague or unclear language can delay approval.

Key elements your governing documents must include:

- Charitable purposes clause that aligns with CRA requirements

- Dissolution clause stating assets go to qualified donees

- Activities description that supports charitable purposes

- Geographic limitations if applicable

Selecting the Right Organisational Structure

Canadian organisations can choose between federal or provincial incorporation for charitable status. Each option has different requirements, costs, and benefits for your organisation.

Federal incorporation allows operations across all provinces and territories. It costs more but provides national recognition and simpler expansion.

We apply through Corporations Canada for federal status. Provincial incorporation limits operations to one province initially and typically costs less with simpler requirements.

Each province has different rules and processing times. Non-profit corporations represent the most common structure for charities.

They cannot distribute profits to members and must use surplus funds for charitable purposes. This structure aligns well with CRA requirements.

Consider these factors when choosing structure:

Board of Directors and Trustees Requirements

Your organisation needs qualified directors or trustees to meet CRA standards. These individuals oversee operations and ensure compliance with charitable purposes and legal requirements.

Minimum director requirements vary by jurisdiction but typically require at least three directors. Directors must be adults with legal capacity to serve.

Some provinces require Canadian residents as directors. Trustees manage charitable property and ensure funds serve charitable purposes.

In many organisations, directors also serve as trustees. They have legal duties to act in the organisation's best interests.

We must ensure directors understand their responsibilities. They oversee finances, approve major decisions, and maintain charitable compliance.

Director qualifications include:

- Age requirements (typically 18 or older)

- Residency rules (varies by jurisdiction)

- Conflict of interest policies

- Financial literacy for oversight duties

Directors cannot receive compensation beyond reasonable expenses. The CRA monitors director payments to ensure charitable funds serve public benefit rather than private interests.

Required Documentation and Forms

The CRA requires specific forms and documents to process your charity application. You'll need to submit everything through their online portal with detailed financial information and supporting materials.

Key Application Forms and Online Submission

The Government of Canada switched from the T2050 form to an online application system in 2019. You now submit your application to register a charity through the My Business Account portal on the Canada Revenue Agency website.

The online form replaces the old Application to Register a Charity under the Income Tax Act. This system makes the process faster and easier to track.

You must create a CRA My Business Account if you don't already have one. The account lets you submit documents and check your application status online.

The charity application asks for detailed information about your organization's structure. You'll need to explain your legal form, directors, and expected activities clearly.

Financial Statements and Activity Descriptions

Your application needs a complete financial forecast showing expected income and expenses. The CRA wants to see how you plan to fund your charitable work.

You must include a detailed fundraising plan. This shows how you'll raise money and what methods you'll use.

Financial statements from your organization are required if you've been operating. New organizations need projected budgets instead.

The application requires specific descriptions of all activities you plan to do. You must explain how each activity achieves your charitable objects.

Your financial position needs to be clearly documented. Include bank statements and any existing assets or debts.

Supporting Documents Checklist

Your governing documents are essential for your application. These include articles of incorporation, bylaws, and trust deeds.

Required organizational documents:

- Articles of incorporation or letters patent

- Bylaws or trust deed

- Board resolutions

- Director information forms

Financial documentation needed:

- Current financial statements

- Bank statements

- Revenue projections

- Expense forecasts

You need detailed information about your directors or trustees. Include their names, addresses, and qualifications.

Provide supporting documentation for all claims in your application. Missing documents can cause delays or rejections.

Steps to Apply for Charitable Status in Canada

1. Incorporate Your Organization (If Not Already Done)

Most charities in Canada incorporate federally or provincially before applying for charitable status. This step provides a legal structure and ensures compliance with governance laws.

- Federal Incorporation: Processed by Corporations Canada, typically takes 1-3 days.

- Provincial Incorporation: Varies by province, may take longer.

2. Draft Governing Documents

Your organization’s governing documents (e.g., bylaws, constitution) must clearly outline its charitable purposes and activities. The CRA will review these to ensure they align with charitable objectives.

3. Prepare the CRA Charitable Status Application

To apply for registered charity status, you need to complete the CRA’s charitable status application. This includes:

- A detailed description of your organization’s charitable activities.

- A breakdown of how donations will be used.

- Information about your board of directors and governance structure.

- Financial projections showing how funds will be managed.

4. Submit the Application to the CRA

Once you have gathered all necessary documents, you can submit the charitable status application to the CRA via the CRA's online My Business portal. The CRA's preference is for electronically filed charity applications.

5. Wait for CRA Review and Respond to Any Requests

The CRA review process can take 5-10 months, depending on the complexity of your application, and experience of the charity lawyer filing the charity application. The CRA may request additional information or clarification, so be prepared to respond promptly, though the CRA typically provides 60 days to respond.

6. Receive Your Charity Registration Number

If your application is approved, you will receive a Charitable Registration Number from the CRA, allowing you to issue official donation receipts and apply for funding.

Common Reasons for Charitable Status Application Rejections

Not all applications are approved. Here are some common reasons why applications are denied:

- Purposes do not meet the CRA’s definition of charity.

- Activities are too vague or not directly charitable.

- Poor governance structure (e.g., lack of board oversight).

- Failure to demonstrate public benefit.

- Financial mismanagement concerns.

To avoid rejection, ensure your application is detailed, clear, and aligned with CRA guidelines.

Benefits of Registering as a Charity in Canada

Once registered, a charity in Canada can:

- Issue official donation receipts to donors, allowing them to claim tax credits.

- Access funding from government grants and other registered charities.

- Benefit from income tax exemptions.

- Enhance credibility and attract more donors and volunteers.

How to Start a Charity in Ontario

If you are starting a charity in Ontario, you must comply with both provincial and federal regulations. Ontario charities often incorporate under the Ontario Not-for-Profit Corporations Act (ONCA) before applying for charitable status with the CRA.

Is Applying for Charitable Status Right for Your Organization?

Registering as a charity in Canada has many benefits, but it also comes with strict regulations. Before applying, ensure your organization meets all requirements and has a clear charitable purpose. A well-prepared application can increase your chances of approval and allow you to start making an impact as a registered charity.

If you need assistance with the charitable status application, consider consulting a charity lawyer to help navigate the process efficiently.

Post-Registration Obligations and Ongoing Compliance

Registered charities must meet strict ongoing requirements to keep their charitable status. These include filing annual returns, issuing proper donation receipts, spending funds on charitable activities, and passing compliance reviews.

Issuing Donation Receipts

Registered charities can issue official donation receipts for income tax purposes. We follow CRA guidelines when creating these receipts.

Each receipt needs specific information. Include the charity's registered name and number, donor details, donation amount, and date received.

We cannot issue receipts for all types of support. Receipts are only for monetary gifts and certain property donations.

We cannot provide receipts for volunteer time or services.

The CRA has strict rules about receipt content and format. Receipts must show the donation was voluntary with no benefit given to the donor.

We keep copies of all receipts issued. These records help during CRA audits and compliance reviews.

Annual Returns and Reporting

All registered charities file a T3010 form each year. We have six months after our fiscal year ends to submit this return.

The T3010 gives detailed information about our activities, revenues, and spending. It shows how we used donated funds for charitable purposes.

Missing the filing deadline can result in penalties or loss of charitable status. We must file even if our charity was inactive during the year.

The form requires financial statements and program details. We report on governance, fundraising costs, and executive compensation.

Our T3010 becomes public information once filed. Donors and the public can view these returns through the CRA website.

Maintaining Eligible Charitable Activities

We must spend our resources only on approved charitable activities. These fall into four categories: relief of poverty, advancement of education, advancement of religion, or other purposes that benefit the community.

Registered charities must meet annual disbursement quotas. We need to spend a minimum amount on charitable activities each year based on our assets.

Activities outside our stated charitable purposes can put our status at risk. We cannot engage in political activities beyond allowed limits.

We keep detailed records of all programs and spending. This documentation proves our activities align with our registered charitable purposes.

Any major changes to our activities or purposes require CRA approval. We cannot change what we do without proper authorization.

Re-Registration and Compliance Reviews

The CRA conducts regular compliance reviews of registered charities. These reviews check if we follow all legal requirements and use funds properly.

Reviews can happen randomly or due to complaints. We must provide requested documents and information during these audits.

Serious compliance failures can result in loss of charitable status. Common issues include improper receipting, inadequate record keeping, and inappropriate activities.

Some charities need to re-register after compliance problems. This process requires submitting a new application with corrective measures.

We can appeal CRA decisions about our charitable status. Legal advice helps with complex compliance issues and appeals.

Conclusion

Applying for charitable status in Canada requires careful planning and attention to detail. The CRA's process involves making an informed decision, setting up your organization, completing the application, and navigating the review process.

Success depends on meeting all regulatory requirements and providing complete documentation. Your organization must show genuine charitable purposes and follow CRA guidelines during the application process.

Contact B.I.G. Charity Law Group for expert guidance through your charitable registration journey. Our team understands Canadian charity law and can help ensure your application meets all requirements.

Reach us at dov.goldberg@charitylawgroup.ca or (416) 488-5888 to discuss your needs. Visit CharityLawGroup.ca for more information about our services.

Frequently Asked Questions

Applying for charitable status involves specific requirements, costs, and timelines. Many nonprofits also wonder about starting alone and what donations qualify under Canadian law.

What are the requirements for charitable status in Canada?

Your organization must have only charitable purposes under one of four categories. These include relief of poverty, advancement of education, advancement of religion, or other purposes that benefit the community.

You need proper governing documents like articles of incorporation or a constitution. Establish your organization as a legal entity before applying.

Your activities must meet the Canada Revenue Agency's definition of charitable work. Political activities are allowed but only to a limited extent.

How long does it take to get charity status in Canada?

The Canada Revenue Agency usually takes 6 to 12 months to review applications. Simple applications with complete documentation process faster.

Complex cases or incomplete submissions can take longer. The CRA may request more information during their review.

You cannot issue tax receipts until you receive official charitable registration. Plan ahead because the process takes time.

What qualifies as a charitable donation in Canada?

Donations must go to registered charities or qualified donees for tax benefits. Cash gifts, property, and securities all qualify for tax receipts.

Volunteer time and services do not qualify for tax receipts. Only monetary or property transfers count as charitable donations.

Gifts must be voluntary with no expectation of return benefit. Purchases at charity auctions or events may only partially qualify as donations.

How to get charitable status in Canada?

First, decide if your organization should apply for charitable status. Set up your legal entity before starting the registration process.

Complete the Application for Charitable Status. Provide detailed information about your structure, activities, and finances.

Submit all required documents, including governing papers, bylaws, and financial statements. The CRA reviews your application through their process.

How much does it cost to register a charity in Canada?

The Canada Revenue Agency does not charge fees for charitable registration applications. The application process is free.

You will have costs for legal setup and documentation. Incorporating your organization and preparing proper governing documents may require professional help.

Ongoing compliance costs include annual filings and maintaining proper records. Budget for accounting and legal support after registration.

Can I start a nonprofit by myself in Canada?

You can start a nonprofit alone. However, registered charities need multiple directors.

Most provinces require at least three directors on the board.

Find committed board members who share your vision. Directors help with oversight and governance.

If you start alone, you will handle all setup tasks yourself. These tasks include paperwork, legal requirements, and fundraising.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)