Board of Trustees vs Board of Directors Canada: Differences

Published on

September 24, 2024

Last updated on

March 10, 2026

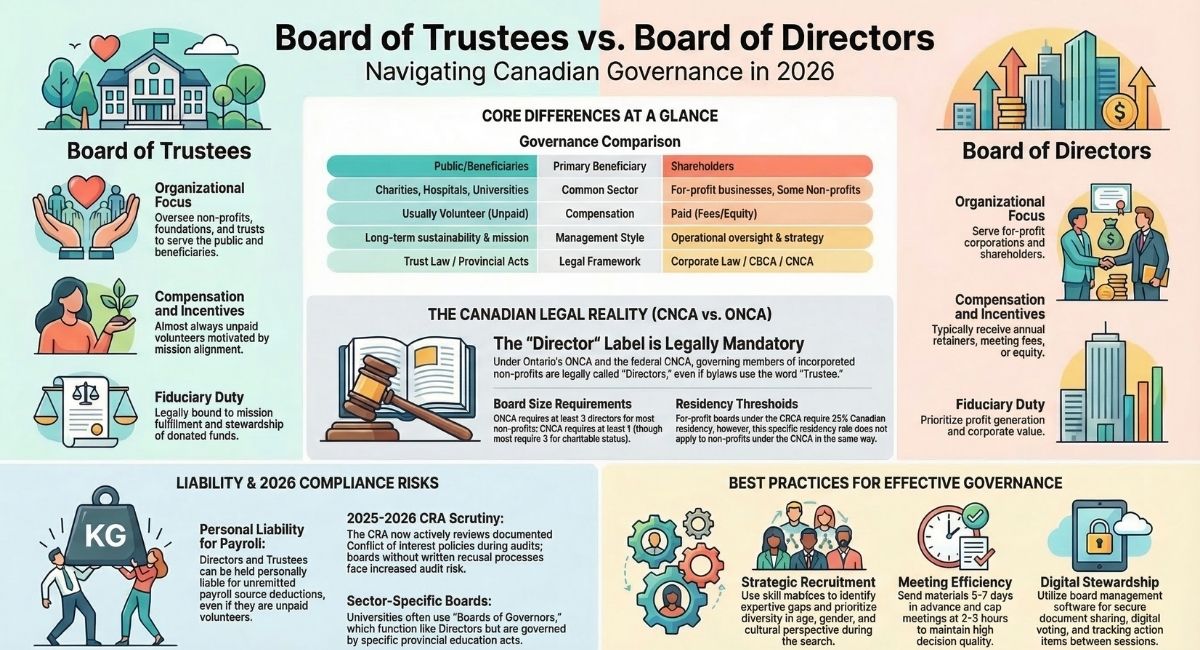

The main difference lies in their organisational focus: boards of directors typically govern for-profit corporations and serve shareholders, while boards of trustees usually oversee non-profit organisations, charitable foundations, and trusts, serving beneficiaries and the broader public interest.

As of 2026, both the Canada Not-for-Profit Corporations Act (CNCA) and Ontario's Not-for-Profit Corporations Act (ONCA) continue to shape how charity and nonprofit boards are structured and governed across Canada.

We'll explore how these governance structures differ in their roles, responsibilities, and legal obligations within the Canadian context. From understanding their typical compositions to examining sector-specific applications, this comprehensive guide will help clarify when each type of board is appropriate and how they can operate most effectively under Canadian law.

Definition and Overview: Board of Trustees vs Board of Directors

Both boards oversee organizations, but they differ in structure, legal obligations, and the types of organizations they serve.

Understanding these distinctions helps clarify which governance model applies to specific organizational contexts.

What Is a Board of Trustees?

A board of trustees is a group of individuals who hold legal responsibility for managing an organization's assets and ensuring its mission is fulfilled.

We typically find trustees in non-profit organizations, charities, and educational institutions.

Trustees have a fiduciary duty to protect the organization's resources. They must act in the best interests of beneficiaries and stakeholders.

The key responsibilities include:

- Overseeing the organization's mission and strategic direction

- Managing endowments and charitable funds

- Ensuring compliance with charitable regulations

- Appointing senior leadership

In Canada, trustees often govern universities, hospitals, foundations, and religious organizations.

They usually serve without compensation and bring specialized expertise to support the organization's goals.

Trustees typically have less direct involvement in daily operations.

They focus on long-term sustainability and ensuring the organization serves its intended purpose.

What Is a Board of Directors?

A board of directors is a governing body elected by shareholders to oversee a corporation's management and strategic decisions.

We see directors primarily in for-profit companies and some non-profit organizations.

Directors represent shareholder interests and work to maximize organizational value.

They have legal duties to act with care, loyalty, and good faith.

Primary responsibilities include:

- Hiring and evaluating executive leadership

- Approving major business decisions

- Setting corporate strategy and policies

- Ensuring regulatory compliance

Canadian corporations must have at least one director, though most have multiple members.

Directors can be more involved in operational decisions than trustees.

Directors face potential personal liability for corporate actions.

They must balance stakeholder needs while fulfilling their duties to shareholders and the organization.

Common Terminology Mistakes

Many people use "board of trustees" and "board of directors" interchangeably, but this creates confusion about governance roles and legal responsibilities.

The most common mistake is calling all governance bodies "boards of directors." Non-profit organizations often have trustees, not directors, even though their functions may seem similar.

Key distinctions:

- Purpose: Trustees serve beneficiaries; directors serve shareholders

- Compensation: Trustees usually unpaid; directors often receive fees

- Legal framework: Different regulations govern each type

Some organizations use both terms incorrectly in their bylaws or documentation. This can create legal complications and unclear accountability structures.

In Canada, provincial incorporation laws often specify which term applies to different organization types.

We recommend checking local regulations to ensure proper terminology and compliance.

Key Differences Between Boards of Trustees and Boards of Directors

Boards of trustees and boards of directors serve different types of organizations and have distinct legal duties, compensation structures, and liability frameworks.

These differences shape how board members operate and fulfill their fiduciary responsibilities.

Legal Duties and Fiduciary Responsibilities

Board members in both structures have fiduciary duties to act in their organization's best interests.

The specific focus of these duties differs significantly.

Directors serve shareholders of for-profit corporations.

Their primary fiduciary responsibility centres on maximizing shareholder value and protecting investor interests.

Trustees serve broader stakeholder groups in non-profit organizations.

Trustees are accountable to donors, beneficiaries, and the general public rather than shareholders.

Key Legal Differences:

- Directors must prioritize profit generation and shareholder returns

- Trustees must focus on mission fulfillment and public benefit

- Both face potential personal liability for breaching fiduciary duties

- Trust law governs trustees more strictly than corporate law governs directors

The fiduciary responsibility of trustees often involves managing donated funds or endowments.

This creates additional legal obligations around fund stewardship.

The CRA expects registered charities to demonstrate that their board exercises independent oversight and that directors or trustees do not benefit personally from charitable assets. Boards that lack documented conflict of interest policies face increased scrutiny during CRA audits.

Compensation and Volunteerism

Most trustees serve without pay as volunteers.

This reflects the charitable nature of the organizations they govern.

Directors typically receive compensation for their service.

Payment structures vary but often include annual retainers, meeting fees, or equity compensation.

Compensation Patterns:

- Trustees: Usually unpaid volunteers

- Directors: Receive monetary compensation or benefits

- Exception: Some large non-profits may pay trustee stipends

The volunteer nature of trustee roles attracts people motivated by mission alignment rather than financial gain.

Directors balance fiduciary duties with compensation expectations.

This difference affects recruitment strategies and board composition.

Trustees often bring passion for the cause, while directors bring business expertise.

Types of Organizations Served

The type of organization determines whether we use trustees or directors.

Each structure serves specific organizational forms.

Organizations with Trustees:

- Charitable foundations

- Religious institutions

- Educational institutions

- Charitable trusts

- Endowment funds

Organizations with Directors:

- For-profit corporations

- Some non-profit corporations

- Business enterprises

- Publicly traded companies

Many non-profits use "board of directors" terminology even when legally functioning as trustees.

This creates confusion but doesn't change their actual legal responsibilities.

The organizational structure affects governance approaches.

Trustees focus on mission preservation while directors emphasize business performance.

Liability Considerations

Both trustees and directors face personal liability risks, but the sources and types of liability differ between roles.

Trustees face liability for mismanaging charitable assets or violating trust terms.

Provincial trust laws provide specific protections and requirements for trustee conduct.

Directors face liability for corporate decisions that harm shareholders or violate corporate laws.

Business judgment rules often protect directors making reasonable decisions.

Liability Protection Measures:

- Directors and officers insurance coverage

- Organizational indemnification policies

- Legal safe harbour provisions for good-faith decisions

Trustee liability often relates to asset management and mission compliance.

Director liability typically involves business decisions and regulatory compliance.

Both roles require careful attention to conflicts of interest and proper governance procedures to minimize personal liability exposure.

In Canada, volunteer directors of registered charities are not automatically exempt from personal liability. Under the Income Tax Act, directors can be held personally liable for unremitted payroll source deductions — even if they received no compensation for their board service. This applies under both federal and provincial employment and tax legislation, and it is one of the most important liability risks that unpaid charity board members need to understand.

Roles and Responsibilities in the Canadian Context (2026)

Both boards of trustees and boards of directors in Canada share core governance duties under federal and provincial legislation.

These responsibilities centre on strategic oversight, financial stewardship, and ensuring compliance with legal requirements.

Strategic Planning and Oversight

Both types of boards carry primary responsibility for setting organizational direction in Canada.

Under the Canada Business Corporations Act and provincial legislation, directors establish long-term strategic plans that guide their organizations forward.

For-profit corporations require directors to focus on shareholder value creation.

These boards work closely with executive directors to develop business strategies that drive growth and profitability.

Non-profit organizations operate differently under the Canada Not-for-Profit Corporations Act.

Trustees must prioritize mission fulfillment over profit generation.

Their strategic planning focuses on advancing charitable purposes and community benefit.

Key oversight duties include:

- Monitoring executive performance

- Approving major strategic initiatives

- Ensuring organizational goals align with stakeholder interests

Both board types must delegate day-to-day management while maintaining supervisory roles.

Canadian organizations often balance board direction with operational autonomy.

Financial Management and Resource Allocation

Canadian boards face strict fiduciary duties regarding financial oversight.

Directors and trustees must act in good faith when managing organizational resources and making financial decisions.

Corporate directors focus on maximizing returns for shareholders.

They approve budgets, oversee financial reporting, and ensure proper allocation of financial resources.

These boards regularly review revenue streams and investment strategies.

Trustees manage resources to advance charitable missions.

They must ensure donated funds serve intended purposes while maintaining organizational sustainability.

Common financial responsibilities include:

- Approving annual budgets

- Monitoring cash flow and reserves

- Overseeing audit processes

- Ensuring transparent financial reporting

Both board types must understand financial statements and maintain adequate internal controls.

Canadian legislation requires directors to exercise reasonable care in financial decision-making.

Risk Management and Compliance

Risk management forms a critical component of board responsibilities in Canada.

Directors and trustees must identify, assess, and mitigate risks that could impact their organizations.

Compliance requirements vary by organization type.

Corporate directors ensure adherence to securities regulations and business laws.

Trustees must follow charity regulations and maintain tax-exempt status.

Essential risk management duties include:

- Establishing ethical standards

- Monitoring legal compliance

- Implementing internal controls

- Overseeing insurance coverage

Canadian boards must stay current with changing regulations.

The Canada Revenue Agency closely monitors charitable organizations, while securities commissions oversee public companies.

Both board types face personal liability for governance failures.

Directors who fail to meet their duties may face legal consequences under Canadian law.

How Provincial Law Affects Your Board Structure in Canada

Governance terminology and legal requirements for boards vary significantly depending on how and where your organisation is incorporated. Federal incorporations fall under the Canada Not-for-Profit Corporations Act (CNCA), while organisations incorporated in Ontario fall under the Ontario Not-for-Profit Corporations Act (ONCA). Understanding which legislation governs your board is essential for compliance.

Ontario Not-for-Profit Corporations Act (ONCA)

ONCA came into full force on October 19, 2021, and applies to all Ontario-incorporated nonprofits and charities.

Under ONCA, governing members are referred to as directors, not trustees — even in registered charities. If your organisation uses the word "trustee" in its bylaws, this does not change your legal obligations as a director under ONCA.

Key requirements under ONCA include:

- A minimum of three directors for most Ontario nonprofits

- Directors must be individuals, at least 18 years old, and not bankrupt

- At least one director must be a resident Canadian unless the organisation qualifies for an exemption

- Public benefit corporations (which includes most registered charities) must have at least three directors who are not employees of the organisation

ONCA also introduced stronger member rights, clearer rules around board accountability, and updated provisions for conflict of interest. Organisations should review their bylaws to confirm compliance with ONCA's updated requirements.

For a detailed breakdown of ONCA compliance, visit our ONCA resources page.

Federal Nonprofits Under the CNCA

The Canada Not-for-Profit Corporations Act (CNCA) governs federally incorporated nonprofits and charities in Canada.

Under the CNCA, all governing members are called directors. Key requirements include:

- At least one director, though most boards require a minimum of three

- Directors must be individuals (not corporations), at least 18 years old, and not bankrupt

- At least 25% of directors must be resident Canadians; if the board has fewer than four members, at least one must be a resident Canadian

- This Canadian residency requirement does not apply to nonprofit corporations under the CNCA in the same way it does under the CBCA

Federal nonprofits with charitable status are also subject to CRA oversight and must ensure their board composition and governance practices meet both CNCA and Income Tax Act requirements.

British Columbia and Other Provinces

Provincial legislation varies across Canada and uses different terminology, election rules, and board composition requirements.

- British Columbia: Nonprofits are governed by the BC Societies Act, which came into force in November 2016. Governing members are called directors, and societies must file annual reports with BC Registries.

- Alberta: Nonprofits fall under the Societies Act (Alberta) and, in some cases, the Companies Act. Alberta societies must have a minimum of five directors.

- Other provinces: Each province has its own nonprofit legislation with distinct default rules on board size, elections, and member rights.

If your charity or nonprofit operates across multiple provinces, you need to understand which provincial law applies to your incorporation and how it interacts with your CRA registration requirements.

Typical Structures and Composition

Both boards of directors and boards of trustees follow specific structures in Canada, with differences in how members are selected and organized.

The composition varies based on whether the organization is for-profit or non-profit, affecting everything from board size to committee requirements.

Appointment, Election, and Terms

Board of Directors are elected by shareholders at annual meetings through majority vote.

Directors can serve terms up to three years, with the specific length set in corporate by-laws.

If no term is stated, directors serve until the next shareholders' meeting.

Directors must be at least 18 years old and cannot be corporations themselves.

At least 25% of directors must be resident Canadians, or one director if the board has fewer than four members.

Shareholders can remove directors through a special meeting with majority approval.

When vacancies occur, remaining directors can appoint replacements if a quorum still exists.

Trustees are typically appointed through different methods depending on the organization's governing documents.

Many non-profit organizations use nomination committees or member elections.

Some charitable foundations have self-perpetuating boards where existing trustees select new members.

Terms for trustees often range from two to four years.

Many organizations implement staggered terms to maintain continuity.

Board Size and Composition

Corporate Boards in Canada must have at least one director, though most have between three to fifteen members.

The exact number is specified in the articles of incorporation.

Public companies typically maintain larger boards with diverse expertise.

Private corporations often operate with smaller boards, sometimes just one person serving as sole director, officer, and shareholder.

Trustee Boards vary significantly in size.

Small charitable organizations might have five to seven trustees, while large foundations can have twenty or more members.

Many non-profit boards seek diverse representation reflecting their communities or beneficiaries.

Religious institutions often include clergy and lay members, while educational trusts typically include academics and community leaders.

Board Member Roles and Committees

Directors organize into several key committees:

- Audit Committee - Oversees financial reporting and risk management.

- Governance Committee - Manages board nominations and ethics.

- Compensation Committee - Reviews executive pay and benefits.

The chairperson leads meetings and sets agendas.

Directors can join meetings electronically if by-laws allow.

Trustees often form similar committees with different focuses:

- Finance Committee - Manages investments and budgets.

- Program Committee - Oversees mission-related activities.

- Development Committee - Handles fundraising and donor relations.

Trustees often take more hands-on roles in organizational activities.

Corporate directors focus mainly on oversight and strategic direction.

Sector-Specific Applications in Canada

Different sectors in Canada use boards of trustees or directors based on their legal structure and mission.

Non-profit organizations usually use trustees, while for-profit entities rely on directors for governance and oversight.

Trustees in Foundations and Charities

Canadian foundations and charities operate under boards of trustees who hold assets in trust for charitable purposes.

These trustees have fiduciary duties to protect the organization's mission and resources.

Charitable trustees must ensure funds are used according to the organization's charitable objects.

They oversee grant-making processes and investment strategies.

Trustees manage endowment funds and ensure compliance with Canada Revenue Agency requirements.

They maintain charitable status by following strict guidelines for activities and spending.

Key responsibilities include:

- Protecting charitable assets

- Ensuring mission alignment

- Maintaining CRA compliance

- Overseeing financial stewardship

Trustees in foundations often serve longer terms than corporate directors.

This continuity helps preserve the founder's vision across generations.

Boards in Hospitals and Museums

Canadian hospitals use boards of trustees or directors depending on their ownership structure.

Public hospitals often have boards appointed by provincial governments.

Museum boards govern both public and private institutions across Canada.

They balance cultural mandates with financial sustainability.

Hospital board priorities:

- Patient care quality

- Budget management

- Strategic planning

- Community health needs

Museum trustees focus on collection stewardship and public programming.

They ensure cultural artifacts are preserved for future generations.

These boards work closely with professional management.

Hospital CEOs and museum directors handle daily operations while boards provide strategic oversight.

Both sectors need specialized knowledge from board members.

Medical expertise helps hospital boards, while cultural and business experience benefits museums.

Boards in Educational Institutions

Educational institutions in Canada use various board structures.

Universities have boards of governors while school districts operate under elected school boards.

Private schools often use boards of trustees similar to charitable organizations.

These trustees ensure educational mission fulfillment and financial stability.

University boards of governors typically:

- Set academic policies

- Approve budgets

- Hire senior administrators

- Oversee campus development

School boards make decisions affecting entire districts.

They hire superintendents and approve curriculum changes within provincial guidelines.

Educational boards balance academic freedom with accountability.

They must serve students while managing public resources responsibly.

Board composition varies by institution type.

Public universities include government appointees, while private schools select trustees based on expertise and commitment to educational values.

Looking to define clear goals for your nonprofit school or program? Explore our guide to developing charitable purposes for education-based organizations in Canada.

2025–2026 Updates: What Canadian Charity Boards Need to Know

Governance requirements for Canadian charity and nonprofit boards have continued to evolve. The following updates reflect what registered charities and nonprofits need to be aware of as of 2026.

CRA Conflict of Interest Expectations

The CRA has increased scrutiny of conflict of interest policies for registered charity boards. As of 2025, charities are expected to have a written conflict of interest policy in place. Directors and trustees must disclose any actual or perceived conflicts and must recuse themselves from votes or decisions where a conflict exists. This is actively reviewed during CRA audits and compliance reviews.

Boards that cannot demonstrate a documented conflict of interest process face increased audit risk and potential compliance issues that could affect charitable registration.

CBCA Residency Requirements Remain in Force

Under the Canada Business Corporations Act, at least 25% of directors must be resident Canadians. For boards with fewer than four directors, at least one must be a resident Canadian. This requirement applies to federally incorporated for-profit corporations but not to nonprofits incorporated under the CNCA.

Boards should confirm that their current composition meets the residency threshold, particularly when filling vacancies or adding new directors.

Director Liability for Payroll Remittances

Canadian courts have continued to reinforce that charity directors and trustees can face personal liability for unpaid source deductions — including payroll remittances — even if they are unpaid volunteers. This liability arises under the Income Tax Act and the Canada Pension Plan Act.

Directors who are found to have failed to prevent non-remittance of employee deductions can be held personally responsible for the outstanding amounts, plus interest and penalties. Directors and officers insurance is strongly recommended for all Canadian charity boards regardless of organisation size.

Governance Policies the CRA Expects in 2026

The CRA's guidance recommends that registered charities maintain documented policies covering the following areas:

- Board meetings and quorum requirements

- Director terms, election procedures, and removal

- Conflict of interest disclosure and recusal

- Financial signing authority and internal controls

- Compensation and expense reimbursement for directors and staff

Boards that lack these written policies face increased scrutiny during CRA audits. Having these policies in place also protects individual directors from personal liability by demonstrating that the board exercised proper oversight.

Best Practices for Effective Board Governance

Strong governance needs structured meetings, proper recruitment processes, and the right technology tools.

These elements help boards make better decisions and serve their organizations more effectively.

Meeting Management and Board Collaboration

Well-run meetings form the foundation of effective governance.

Board members need quality information before each meeting to make informed decisions.

Meeting Preparation

- Send meeting materials 5-7 days in advance.

- Include financial reports, committee updates, and key documents.

- Provide clear agendas with time limits for each topic.

During Meetings

Encourage respectful debate while staying focused on strategic issues.

The chair keeps discussions on track and ensures all voices are heard.

Board meetings work best when they last 2-3 hours maximum.

Longer meetings reduce focus and decision quality.

Follow-Up Actions

Meeting minutes should capture key decisions and action items clearly.

Track progress on assigned tasks between meetings.

Regular executive sessions without staff present help board members discuss sensitive topics openly.

Need a clear example for your nonprofit’s records? Explore our guide to meeting minutes for Canadian charities to ensure compliance and effective governance.

Recruitment and Orientation

Strategic recruitment brings the right skills and experience to boards.

Identify specific expertise gaps before starting the search process.

Recruitment Strategy

- Create skill matrices to identify needed competencies.

- Look for candidates with relevant professional backgrounds.

- Consider diversity in age, gender, and cultural perspectives.

Orientation Process

New board members need comprehensive orientation within 30 days of joining.

This includes reviewing governance policies, financial statements, and strategic plans.

Pair new members with experienced board colleagues as mentors.

This helps them understand board culture and expectations quickly.

Ongoing Development

Board education sessions keep members current on industry trends and governance best practices.

Budget for conference attendance and training workshops.

Regular board evaluations help identify areas for improvement and training needs.

Leveraging Board Management Software

Board management software streamlines administrative tasks and improves communication between meetings.

Modern platforms offer secure document sharing and meeting management tools.

Key Features to Consider

- Secure document libraries with version control.

- Meeting scheduling and agenda building tools.

- Digital voting capabilities for remote decisions.

- Mobile access for board members.

Implementation Benefits

Digital tools reduce preparation time for staff and board members.

Access meeting materials anywhere and track action items more effectively.

Board management software also supports fundraising by organizing donor information and tracking relationship management activities.

Security Considerations

Choose platforms with strong encryption and access controls.

Board documents often contain confidential information that needs protection.

Regular software updates and user training help maximize these tools' benefits while maintaining security standards.

Conclusion

Understanding the key differences between boards of trustees and boards of directors helps Canadian organizations choose the right governance structure. Trustees focus on fiduciary duties and asset management for non-profits, charities, and foundations. Directors handle strategic oversight and decision-making for corporations and businesses.

Both governance models serve important roles in Canada's organizational landscape. The choice between them depends on your organization's legal structure, purpose, and regulatory requirements. Non-profits typically benefit from trustee governance, while corporations need director-led boards.

We help Canadian organizations navigate these complex governance decisions at Charity Law Group. Our legal expertise ensures your board structure aligns with Canadian law and serves your organization's mission effectively. Whether you need trustee or director governance, proper legal guidance protects your organization's interests.

Frequently Asked Questions

Is the board of trustees the same as the board of directors?

No. Directors serve for-profit companies and focus on maximising shareholder value, while trustees manage charitable organisations and prioritise nonprofit missions. Trustees face stricter regulations under charitable trust acts and, in many cases, higher personal liability standards than directors in for-profit corporations.

What is the difference between a trustee and a director in a Canadian charity?

Many charities use both terms informally, but legally, under ONCA and the CNCA, governing members of incorporated nonprofits are called directors — not trustees. Trustees typically govern unincorporated charitable trusts or are used informally in some foundations. If your charity is incorporated in Ontario or federally, your board members are directors under the law, regardless of what your bylaws call them.

Does a Canadian charity need a board of directors or a board of trustees?

Incorporated charities in Canada — whether under the CNCA or ONCA — are required to have a board of directors. Unincorporated charities operating as trusts use trustees instead. The vast majority of CRA-registered charities in Canada are incorporated and therefore governed by a board of directors.

What is the role of the board of directors in Canada?

Directors oversee management, strategy, and legal compliance for corporations and incorporated nonprofits. They are elected by members or shareholders to protect the organisation's interests and must act as fiduciaries. Under the Canada Business Corporations Act and the CNCA, directors must act honestly, in good faith, and with the care, diligence, and skill of a reasonably prudent person.

Can a trustee also be a director?

Yes, one person can serve both roles — but only on different boards, never within the same organisation. In some charitable foundation structures, the same individuals serve as corporate directors and also hold assets in trust as trustees. Each position carries separate legal obligations and liability exposure that must be clearly documented in your governing documents.

What are the minimum number of directors required for a Canadian nonprofit?

Under the CNCA, a federal nonprofit requires at least one director, though most constitutions require at least three. Under ONCA, Ontario nonprofits require a minimum of three directors. Public benefit corporations under ONCA — which includes most registered charities — must have at least three directors who are not employees of the organisation.

What happens if a charity director breaches their fiduciary duty in Canada?

A director who breaches their fiduciary duty can face personal liability, removal from the board, and in serious cases, the CRA may revoke the charity's registration. Directors and officers insurance is strongly recommended for all Canadian charity boards. Courts have found that even unpaid, volunteer directors are not automatically protected from personal liability.

Is a board of governors the same as a board of directors in Canada?

Not exactly. In Canada, universities and some large institutions use the term "board of governors" for their governance body. This functions similarly to a board of directors but is governed by specific provincial university or education acts rather than general corporate law. The legal duties are broadly similar, but the enabling legislation and composition rules differ.

What governance policies does the CRA expect charity boards to have in 2026?

The CRA expects registered charities to maintain written policies covering board meetings and quorum, director election and removal, conflict of interest disclosure and recusal, financial signing authority, and expense reimbursement. Boards without these documented policies face increased audit risk and potential compliance action.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)