Can a Registered Charity Return a Donation in Canada?

Published on

May 26, 2021

Last updated on

July 19, 2026

We are a Canadian Charity in the poverty sector, operating out of British Columbia, Vancouver, to be specific. We recently received a sizable donation from a shady individual who has proceeded to publicize his contribution to our Charity. We would like to return the donation and disassociate from him.

This is one of the most sensitive legal situations a Canadian registered charity can face. The answer depends on how the donation was made, what your governing documents say, and what the Canada Revenue Agency (CRA) requires.

Can a Canadian Charity Legally Return a Donation?

Short Answer: generally, no.

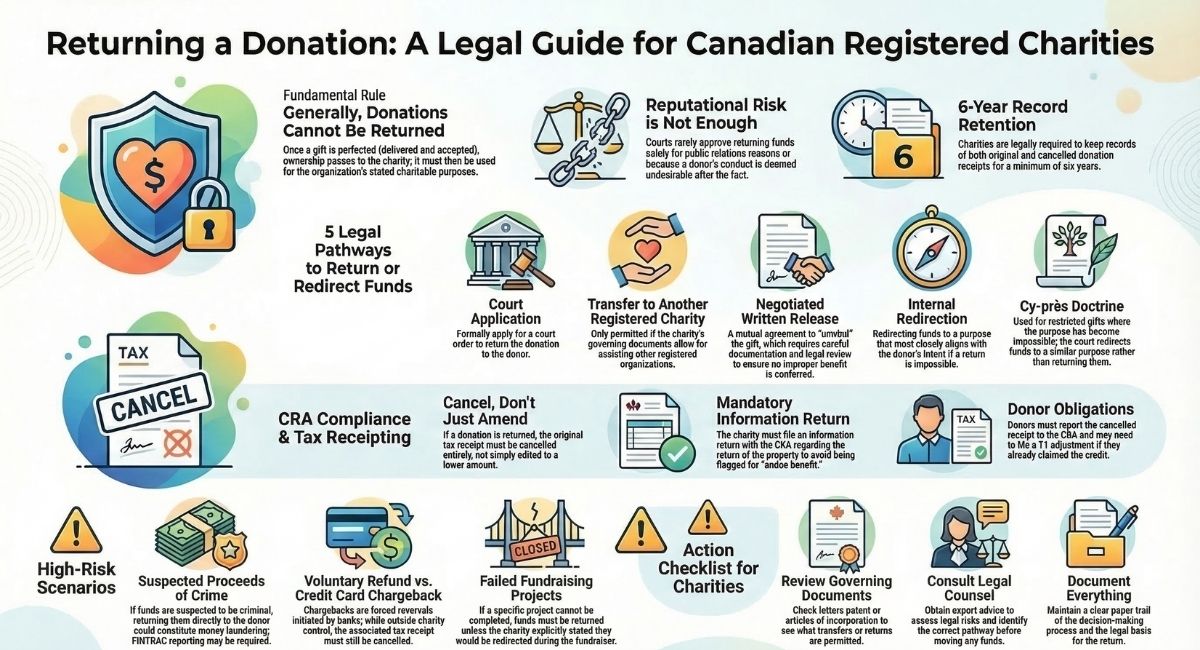

Comprehensive Answer: Generally, a charity cannot return a donation or gift that it has received. Why? Because a gift transfers ownership to the charity, and the charity's purposes in its constituting and governing documents will require it to use the donation to further its charitable purposes.

Under the Income Tax Act (Canada), a gift is defined as a voluntary transfer of property with no expectation of return. Once a donation meets this definition and is received by the charity, ownership legally passes to the organization. The CRA's published guidance on returning donated property confirms that charities must use all received funds for their stated charitable purposes — returning funds to a donor is therefore treated as a disposition of charitable property, which requires careful legal handling.

For more detailed guidance from the CRA, see here.

What Are a Charity's Options When It Wants to Return a Donation?

It is important to understand at the outset that finding a donor's conduct or reputation undesirable — sometimes described as finding a donor "shady" after the fact — is generally not a sufficient legal ground to return a completed gift under Canadian law.

Once a gift is perfected (transfer of title, delivery, and acceptance), charitable assets cannot be returned simply for reputational or public relations reasons without a valid legal basis. Doing so without legal authority may be viewed as a breach of fiduciary duty by the charity's directors.

Courts are extremely hesitant to approve the return of funds solely for dissociation purposes unless the donation itself causes the charity to violate its own objects or the law.

Option 1: Make a court application to return the donation to the donor.

Option 2: Transfer the donation to another registered charity. Note: a charity may only do so if its governing or constating documents and governing documents allow assistance to other registered charities.

Option 3: Negotiate a written release with the donor. In some cases, a charity and donor may reach a mutual agreement to unwind the gift. This must be documented carefully and reviewed by a charity lawyer, as the CRA may still scrutinize the transaction to confirm no benefit was conferred.

Option 4: Apply funds to a closely related charitable purpose. If returning the donation is not possible and transferring to another charity is not permitted under your governing documents, you may be able to redirect the funds internally to a purpose that most closely aligns with the donor's original intent. Legal advice is essential before doing this.

Option 5: Seek a court order under the cy-près doctrine. In cases involving restricted gifts where the original purpose has failed or become impractical, a court may apply the cy-près doctrine to redirect the funds to a similar charitable purpose rather than returning them to the donor.

Note: Where a charity fundraises for a specific project and later cannot complete that project — whether intentionally or due to circumstances beyond its control — the donations collected for that project must be returned to donors.

This is the case unless the charity clearly communicated to potential donors at the time of fundraising that their contributions would be redirected to other projects if the specific project did not proceed.

Importantly, courts generally treat the cy-près doctrine as a preferred first remedy when a specific charitable purpose fails — returning funds to the donor is typically the last resort a court will consider, not the first, particularly where the donor's intent reflected a general charitable purpose.

What Happens to the Donation Tax Receipt When a Donation Is Returned?

When a registered charity returns a donation to a donor, the original official donation receipt must be cancelled — not amended. The charity is also required under the Income Tax Act to file an information return with the CRA regarding the return of the property.

Issuing a receipt that simply shows a $0 eligible amount without following the proper cancellation and reporting procedure is not sufficient and does not satisfy the charity's legal obligations.

Where a charity returns property that was subject to an official donation receipt without complying with the applicable provisions of the Income Tax Act, the CRA may treat this as an undue benefit or a failure to devote resources to charitable activities, with significant compliance consequences.

The donor is then obligated to report the amended receipt to the CRA. If the donor has already filed their tax return claiming a credit for that donation, they may be required to file a T1 adjustment. Failure to do so could result in a tax liability for the donor.

Charities should retain copies of both the original and amended receipts in their records for a minimum of six years, as required by the Income Tax Act.

What Does the CRA Say About Returning Donated Property?

The Canada Revenue Agency has published guidance specifically on returning donated property. The CRA's position is that a charity must be able to demonstrate that any disposition of charitable property — including a return to the original donor — is consistent with its stated charitable purposes and complies with the Income Tax Act.

The CRA notes that where a charity returns funds without a valid legal basis, it may be considered to have made an improper disbursement. This can trigger compliance consequences, including revocation of charitable status in serious or repeated cases.

Before taking any action to return a donation, Canadian charities should:

- Review their governing documents (letters patent, articles of incorporation, or constitution) to confirm what is permitted.

- Consult a Canadian charity lawyer to assess the legal risk and identify the appropriate pathway.

- Document all steps taken and the legal basis for the decision.

- Issue amended tax receipts correctly and promptly.

The CRA's published guidance on returning donated property is available directly on their website and is updated periodically. Charities should always refer to the most current version.

What If the Donation May Be Proceeds of Crime?

If a charity has reason to suspect that a donation may constitute proceeds of crime, it must not simply return the funds to the donor. Doing so could inadvertently constitute money laundering under Canadian law.

Under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA), charities may have mandatory reporting obligations to FINTRAC before any movement of funds takes place.

Returning suspected criminal proceeds directly to their source without legal guidance could expose the charity and its directors to serious criminal liability.

In these situations, the charity should immediately seek independent legal counsel and, where appropriate, consult law enforcement before taking any action with the funds.

Can an Online or Credit Card Donation Be Returned?

With the rise of online fundraising platforms, many charities now ask whether a digital donation — made by credit card, e-transfer, or through platforms such as CanadaHelps — can be returned or reversed.

Credit card chargebacks are initiated by the donor through their bank or card provider and are outside the charity's direct control. If a donor successfully disputes a transaction, the funds may be reversed automatically. This is not the same as the charity voluntarily returning a donation, but charities should maintain clear donation records and written confirmations to defend against unwarranted chargebacks. If a chargeback is successful, the charity must also cancel any tax receipt issued for that donation.

E-transfers and online payments follow the same legal rules as any other gift. Once received and accepted by the charity, they are treated as donations subject to the same CRA rules. They cannot be returned simply at the donor's request.

Platform-based donations — for example, those processed through CanadaHelps or similar platforms — may have their own refund policies at the platform level. Charities should review their platform agreements carefully to understand how refund requests are handled and what obligations fall on the charity versus the platform.

Conclusion

Updated for 2026: Canadian charity law continues to evolve, and the CRA regularly updates its guidance on charitable gift administration. If your organization is facing a donation return situation, it is essential to get current legal advice rather than relying on general information. Rules around tax receipting, governing documents, and CRA compliance interact in ways that vary by organization.

Navigating donation return situations requires expert legal guidance to protect your charity's reputation and compliance status. Whether you're dealing with problematic donors, project changes, or complex gift arrangements, understanding your legal obligations is crucial for maintaining your registered charity status.

B.I.G. Charity Law Group specializes in helping Canadian charities handle these delicate situations while maintaining CRA compliance. Our experienced team understands the nuances of charitable law and can guide you through donation return processes, policy development, and risk prevention strategies.

Don't let donation complications jeopardize your charitable mission. Contact us at dov.goldberg@charitylawgroup.ca or call 416-488-5888 to discuss your specific situation. Visit CharityLawGroup.ca to learn more about our services, or schedule a FREE consultation today to get the legal support your charity deserves.

Frequently Asked Questions

Can a charity refund a donation in Canada?

Generally, no. Once a registered charity receives a donation, the funds legally belong to the organization and must be used for its charitable purposes.

Refunds are only permitted in exceptional circumstances, such as fraud, court orders, or the failure of a specifically fundraised project. In all cases, legal advice should be sought before returning any donation.

Can a donor demand their donation back?

A donor has no automatic legal right to demand a donation back once it has been received by a registered charity. A completed gift transfers ownership to the charity.

Donors may only recover funds through a court process, or in limited cases involving fraud or misrepresentation. Charities should document all donations and donor communications to protect against unwarranted refund demands.

What should a charity do if it receives a donation from a problematic donor?

If a charity receives a donation from a donor whose reputation or conduct may harm the organization, it has limited options.

The charity may seek legal advice to explore whether a court-approved return is possible, or whether the funds can be transferred to another registered charity. Simply returning the money without legal authority creates CRA compliance risk. Prevention through donor screening policies is the best protection.

What is the difference between a donation refund and a credit card chargeback?

A refund is a voluntary return of funds by the charity. A chargeback is a forced reversal initiated by the donor's bank or credit card provider.

Charities should maintain records of all transactions and donor communications to dispute unwarranted chargebacks. If a chargeback is successful, the charity must also cancel any tax receipt issued for that donation.

Does the charity need to cancel the tax receipt if a donation is returned?

Yes. If a donation is returned for any reason, the charity must cancel the original official donation receipt and file the required information return with the CRA.

The donor must then update their tax filings accordingly, including filing a T1 adjustment if a credit was already claimed. Charities are required to retain copies of both the original and cancelled receipts in their records for at least six years.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)