How to Draft Purposes for Charitable Registration in Canada

Published on

May 20, 2024

Last updated on

July 19, 2026

Are you passionate about making a difference in your community? Have you considered starting a charitable organization to address an issue close to your heart? Whether you're thinking about applying for charitable registration or already have a registered charity but want to amend your purposes, it's crucial to understand the current regulatory landscape and requirements.

With the CRA facing unprecedented backlogs and processing delays, getting your charitable purposes right the first time has never been more critical. The good news is that the CRA recently made this process significantly more accessible. In April 2026, the Charities Directorate released a brand new Short Guide: How to Write a Charitable Purpose — a condensed, plain-language resource designed to help applicants and registered charities write compliant purposes more quickly and easily. At the same time, the CRA also revised its comprehensive technical guidance, CG-019: Charitable Purposes of a Registered Charity, which now includes additional detail on the incidental purposes doctrine, visual aids, expanded guidance on purposes involving qualifying disbursements (grants), and a new Appendix A listing subcategories of charity.

Both resources are worth bookmarking. The Short Guide is the right starting point for most applicants. The full CG-019 is there when you need deeper legal grounding. This article draws on both to walk you through what you need to know.

Current CRA Processing Challenges and Why Precision Matters

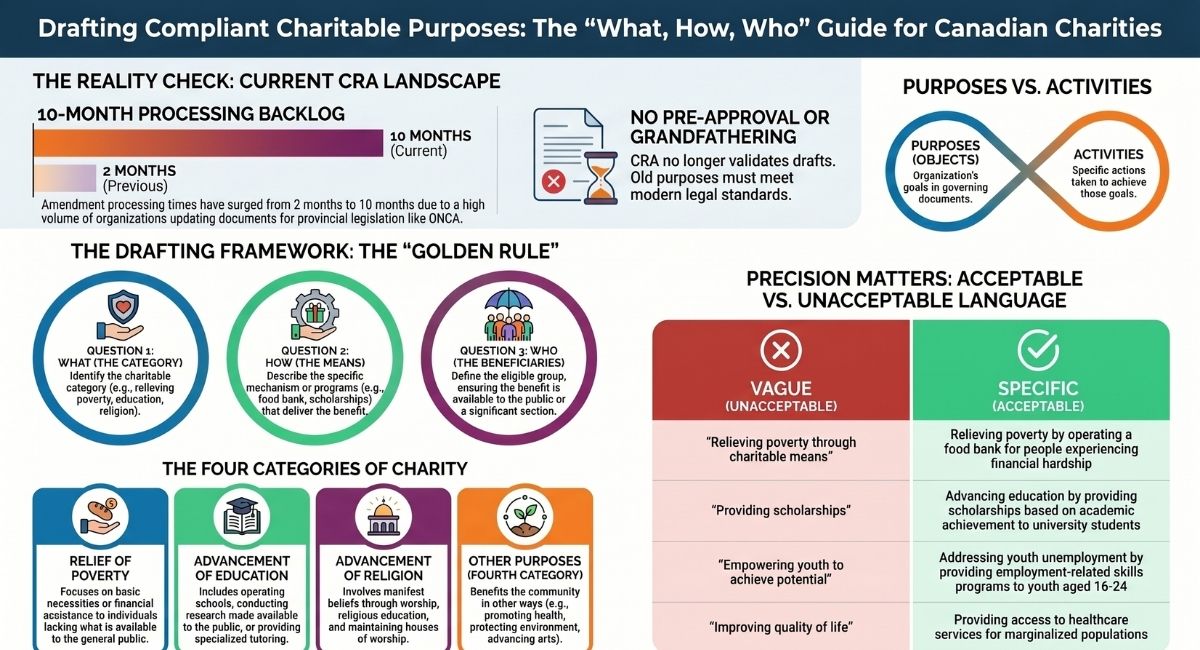

The Canada Revenue Agency currently faces a massive backlog of requests for changes in charitable purposes by registered charities. Processing times for purpose amendments have increased dramatically from 2 months to 10 months for operating charities. This surge is largely due to new provincial legislation like Ontario's Not-for-Profit Corporations Act (ONCA), which has prompted thousands of organizations to update their governing documents.

Approximately 20,000 of Ontario's 60,000 non-profits are registered charities, many with outdated purposes that are either too narrow for their current needs or don't meet today's CRA standards. Importantly, there is no grandfathering of purposes - even if your purposes were approved by the CRA decades ago, they must still meet current legal requirements.

Understanding Charitable Purposes and Activities

Before diving into drafting requirements, it's essential to understand the distinction:

Purposes (also called "objects") are the goals your organization aims to achieve, as outlined in your governing document such as letters patent, articles of incorporation, or constitution.

Activities are the specific actions your organization takes to achieve these goals.

The CRA uses a "two-part test" to assess charitable registration, evaluating both your stated purposes and the activities you conduct to further those purposes.

General Requirements for Charitable Registration

To qualify as a charity under the Canadian Income Tax Act, your organization's purposes must meet specific criteria:

1. Exclusively Charitable

Your purposes should fall into one of four categories: relieving poverty, advancing education, advancing religion, or other purposes beneficial to the community. Additionally, they must provide a charitable benefit to the public or a sufficient section of the public.

2. Defined Scope of Activities

Your organization's resources must be dedicated solely to activities that further its charitable purposes. Subject to limited exceptions, all resources must be devoted to these activities.

Key Elements of Charitable Purposes: The Three-Element Framework

According to CRA Guidance CG-019, each charitable purpose should identify three essential elements, either expressly or through context:

The CRA's new Short Guide distills this framework into a simple golden rule: What, How, Who. Every charitable purpose you write should answer all three questions: what type of benefit the purpose provides (the category of charity), how your organization will provide that benefit (the scope of activities), and who will receive the charitable benefit (the eligible beneficiary group). Keep this three-word checklist in front of you as you draft.

If you are looking for a practical shortcut, the CRA has published an extensive list of example charitable purposes that you can copy directly or adapt. When using an example, make sure it still contains all three elements — what, how, and who — before submitting.

1. Charitable Purpose Category

Clearly identify the category your purpose falls into, such as relieving poverty or advancing education.

Example: "To relieve poverty by providing food and shelter to homeless individuals in our community."

For fourth category purposes, you must specify the particular charitable benefit:

- "To promote health..."

- "To protect the environment..."

- "To advance the arts..."

2. Means of Providing Charitable Benefit

Describe how your organization will achieve its purpose, outlining specific activities that directly contribute to the charitable benefit.

Example: "By operating a food bank and transitional housing program to address immediate needs and empower individuals to break the cycle of homelessness."

This element defines the scope of activities your charity can legally conduct and ensures the provision of a recognizable, measurable charitable benefit that is socially useful and has demonstrable public impact.

3. Eligible Beneficiary Group

Define the group of individuals who will benefit from your organization's activities, ensuring that the benefit reaches the public or a significant section of the public.

Example: "Our services are available to all members of the community experiencing poverty, regardless of age, gender, or background."

Different charitable purposes have different requirements for what constitutes "the public." Some purposes require restrictions (poverty relief must target those experiencing poverty), while others should be available to the public as a whole (general hospitals).

Specific Requirements for Each Category

Relief of Poverty

Focus on aiding individuals experiencing poverty. This includes not only the destitute but anyone lacking basic necessities or simple amenities available to the general public.

Enhanced Examples:

- "To relieve poverty by providing financial assistance and job training programs to low-income families in [specific location]"

- "To relieve poverty by operating a micro-lending program for entrepreneurs starting small businesses who lack access to traditional banking"

- "To relieve poverty by providing tuition subsidies directly to educational institutions for students demonstrating financial need"

Advancement of Education

Emphasize educational initiatives and programs that provide knowledge, develop abilities, or improve useful branches of human knowledge through research.

Enhanced Examples:

- "To advance education by operating a public school providing specialized programs for students with learning disabilities"

- "To advance education by conducting research into sustainable agriculture practices and making results publicly available"

- "To advance education by offering scholarships and tutoring services to support students from underprivileged backgrounds in pursuing higher education"

Advancement of Religion

Specify the religious community or group your organization serves, focusing on manifesting, promoting, or sustaining belief in the religion's key attributes: faith in a higher power, worship, and comprehensive doctrinal system.

Enhanced Examples:

- "To advance the [specific faith] religion by establishing and maintaining a house of worship with services conducted according to traditional doctrines"

- "To advance religion by providing religious education programs for children and adults of the [specific faith] community"

Other Charitable Purposes (Fourth Category)

Clearly define the specific benefit your organization provides to the community, such as promoting health or protecting the environment.

Enhanced Examples:

- "To promote health by operating a public clinic providing preventive healthcare services to underserved populations"

- "To protect the environment by preserving wildlife habitats and conducting conservation education programs"

- "To advance the arts by providing free, high-quality musical performances and music education to the general public"

Purposes to Make Gifts to Qualified Donees

A registered charity may also have a purpose of making gifts or grants to qualified donees — organizations that are themselves legally authorized to receive charitable gifts, such as other registered charities, municipalities, and certain foreign organizations. The updated CG-019 includes expanded guidance and examples on how to draft these purposes correctly, including what language the CRA expects to see when your charity's primary mode of operating is distributing funds rather than delivering programs directly.

If your organization plans to operate as a grantmaking charity — whether a public or private foundation, or an operating charity that funds third parties — your purposes must clearly reflect that grantmaking function. Vague language such as "to support other charitable organizations" is insufficient. The CRA expects language that identifies the charitable category, describes the grantmaking mechanism, and defines the eligible beneficiaries of the downstream work.

Avoiding Broad or Vague Purposes

Ensure clarity and precision in your purposes to avoid potential registration issues. The CRA has provided clear examples of problematic versus acceptable purpose statements:

Broad/Vague Purposes (Unacceptable):

- "Relieving poverty through charitable means"

- "Providing scholarships"

- "Building strong communities through social enterprise"

- "Empowering youth to achieve their maximum potential"

Specific and Clear Purposes (Acceptable):

- "Relieving poverty by operating a food bank for people experiencing financial hardship"

- "Advancing education by providing scholarships based on academic achievement to university students"

- "Improving socio-economic conditions in [specific location] by operating social businesses for people with disabilities"

- "Addressing youth unemployment by providing employment-related skills programs, conferences, and workshops to unemployed youth aged 16-24"

Specific Guidance:

- Broad Purposes: Aim to be specific rather than overly broad, clearly outlining the activities and beneficiaries. Instead of "Supporting community development," specify activities such as "Building playgrounds and recreational facilities for children in underserved neighbourhoods."

- Vague Language: Use concrete terms to describe your organization's goals, avoiding ambiguity. Instead of "Improving quality of life," specify actions such as "Providing access to healthcare services for marginalized populations."

What to Do If Your Registered Charity Plans to Change Its Purposes or Carry On New Activities

Given the current processing delays, careful planning is essential:

1. Assessment and Planning

Review whether your current purposes accurately reflect your organization's activities. Many charities discover their purposes are either too narrow for their work or too broad to meet current standards.

2. Understand the New CRA Support Model

It is important to note that the CRA no longer pre-approves changes to a charity's purposes or activities before you submit your formal amendment. If you previously relied on a pre-review submission to get informal sign-off on proposed wording, that option is no longer available.

The CRA's client service representatives remain available to help — but their role is now to direct you to the relevant published guidance and answer general questions about what is considered charitable. They are not able to review or validate draft purposes in advance. For general questions about charitable purposes, you can reach the Charities Directorate at 1-800-267-2384, Monday to Friday, 8 a.m. to 5 p.m. Eastern time.

This shift makes it more important than ever to draft your purposes carefully before filing, using the CRA's Short Guide and CG-019 as your primary reference points — or working with a charity lawyer who can assess your draft against current CRA standards before submission.

3. Comprehensive Documentation

The CRA requires both charitable purposes and detailed activity statements. These must clearly demonstrate how your proposed activities will directly further your stated charitable purposes.

4. Timeline Considerations

With processing times now extending to 10 months, plan your amendments well in advance of any operational changes or new program launches.

5. Activities That Further Unstated Purposes

Sometimes organizations conduct activities that further charitable purposes not stated in their governing documents. For example:

- A charity stating "relieving poverty by operating a hospital" that actually provides healthcare to the general public may be furthering an unstated purpose of "promoting health"

- An educational charity that also produces cultural performances may be furthering an unstated purpose of "advancing the arts"

If this applies to your organization, you may need to amend your governing documents to include additional charitable purposes.

6. The Incidental Purposes Doctrine

The updated CG-019 now includes an explanation of the common law incidental purposes doctrine. Under this doctrine, a purpose that is not explicitly stated in your governing documents may still be permissible if it is genuinely incidental to your stated charitable purposes. However, relying on this doctrine involves legal nuance and should not be used as a substitute for properly drafted purposes. If your charity's work has evolved beyond its stated purposes, the safer course is to amend your governing documents to reflect what you actually do.

Power Clauses vs. Charitable Purposes

Don't confuse power clauses with charitable purposes. Power clauses specify your organization's authority to conduct certain operational activities (buying property, employing staff, making investments) but don't define your charitable mission. The CRA generally doesn't scrutinize power clauses unless they allow for non-charitable purposes.

Provincial and Federal Requirements

Remember that provincial or territorial charitable registration requirements may differ from federal Income Tax Act requirements. The fact that a provincial government accepts certain purposes doesn't guarantee CRA approval for federal charitable registration.

Conclusion

Drafting corporate purposes for charity registration in Canada requires precision, legal knowledge, and strategic thinking. With current CRA processing delays extending up to 10 months, organizations cannot afford to submit poorly crafted purposes that may result in rejections or lengthy revision cycles.

The three-element framework—charitable category, means of benefit, and eligible beneficiaries—provides a roadmap for creating compliant purposes, but navigating the nuances of charitable law can be complex. From avoiding broad language to ensuring your activities align with stated purposes, each detail matters for successful registration and ongoing compliance.

At Charity Law Group, we specialize in helping organizations draft effective charitable purposes that meet CRA requirements and support your mission. Book my free consultation to learn how our expertise in Canadian charity law can guide your organization through the registration process and ensure your charitable purposes position you for long-term success in serving your community.

Frequently Asked Questions

What are charitable purposes in Canada?

Charitable purposes are the specific goals your organization aims to achieve, which must fall into one of four categories: relief of poverty, advancement of education, advancement of religion, or other purposes beneficial to the community in a way the law regards as charitable.

What are the three types of charities in Canada?

Canada has three types of registered charities: charitable organizations (operate their own programs), public foundations (raise funds from the public and give grants), and private foundations (typically funded by one source and distribute grants).

How to establish a charitable foundation in Canada?

To establish a charitable foundation, you must incorporate or create a trust, draft charitable purposes that meet CRA requirements, apply for charitable registration with the CRA, and meet ongoing compliance obligations including annual filings and disbursement quotas.

What are the requirements for charitable status in Canada?

Your organization must have exclusively charitable purposes, provide public benefit, be non-profit, have proper governance structure, meet disbursement quota requirements, maintain adequate books and records, and file annual returns with the CRA.

What is the purpose of your charity?

A charity's purpose defines what it aims to achieve and must be clearly stated in governing documents. It should identify the charitable category, means of providing benefit, and eligible beneficiaries while being specific enough to define the scope of permitted activities.

What are the four types of charity?

The four categories of charitable purposes in Canada are: relief of poverty (helping those lacking basic necessities), advancement of education (providing knowledge or training), advancement of religion (promoting religious belief and practice), and other purposes beneficial to the community (such as promoting health or protecting the environment).

Related Articles:

- What is the Cost to Register a Charity in Canada?

- How Do You Apply for Charitable Status in Canada?

- Charity Registration Timeline: What to Expect at Each Stage

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)