When to Issue a Donation Receipt for Shares: The Case That Cost a Charity Its Registered Status

Published on

March 31, 2026

Last updated on

March 31, 2026

A single donation receipt — issued 19 months too early and $4.4 million too high — ended a Canadian charity's registered status. The Moon Gate Foundation case is one of the clearest examples of how a receipting error, however it originates, can have permanent consequences.

This article breaks down what happened, why the Canada Revenue Agency (CRA) revoked the Foundation's registration, and what charities and donors must do differently when securities are involved.

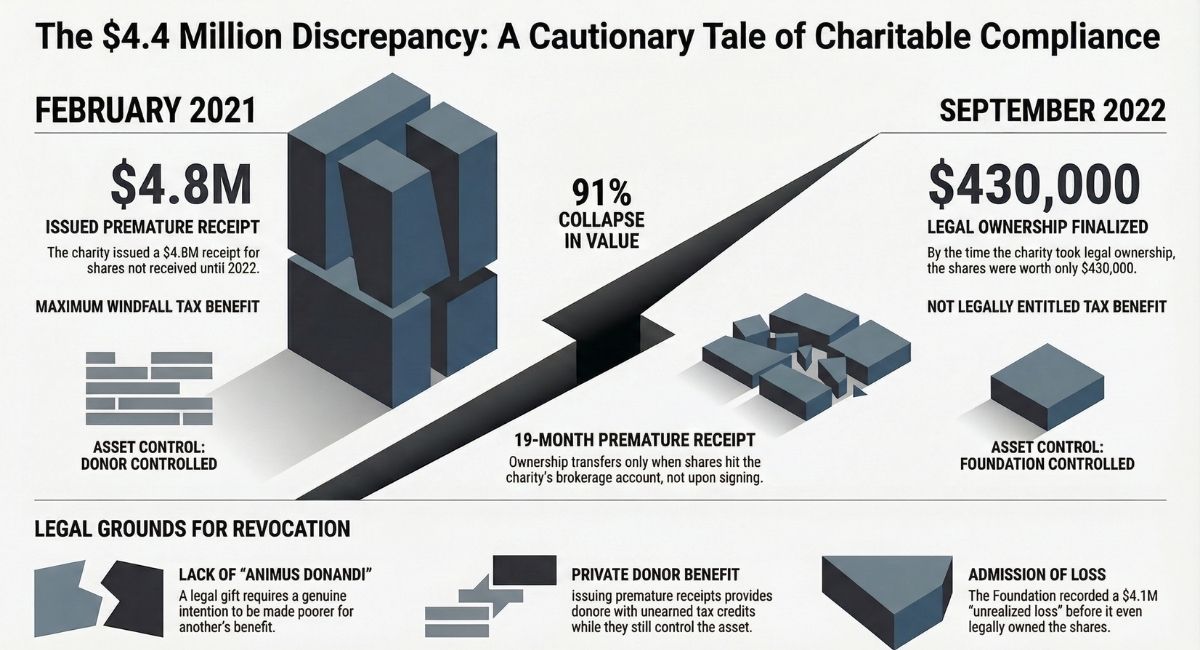

What Happened: The Moon Gate Foundation Timeline

The Moon Gate Foundation case illustrates how quickly a receipting error can escalate into a full revocation. Understanding the sequence of events is the starting point for any charity that accepts non-cash donations.

The Moon Gate Foundation was registered in Vancouver in 2011. Over 13 years, it distributed approximately $15,000 in charitable grants — a modest record for a long-standing registered charity.

In February 2021, the Foundation issued a single donation receipt for $4,836,000 worth of publicly listed shares. The problem: those shares did not arrive in the Foundation's brokerage account until September 2022 — 19 months later.

By September 2022, the shares had lost approximately 91% of their value.

That internal admission — a $4.1 million unrealized loss recorded on the Foundation's own financial statements — became one of the most telling pieces of evidence in the CRA's case.

Why the Receipt Date Is a Legal Threshold, Not a Formality

Many charities treat the receipt date as an administrative detail. The Moon Gate Foundation case makes clear it is a legal threshold with significant consequences.

Under the Income Tax Act, a donation receipt for securities must be dated the day the charity receives the shares — meaning the day those shares appear in the charity's brokerage account. Nothing before that moment constitutes a completed transfer.

Here is what does not qualify as the transfer date:

- The date a transfer certificate is signed

- The date a donor instructs their broker to initiate the transfer

- The date a donation agreement is prepared or executed

- The date a donor verbally commits to the gift

The precise legal threshold that CRA applies is not simply account settlement — it is the moment the charity acquires beneficial ownership of the shares. Under Canadian common law, this means the charity has legally acquired three specific rights: the right to receive dividends, the right to receive proceeds on liquidation, and the right to exercise votes attached to the shares.

For electronic transfers, beneficial ownership is confirmed when the shares settle in the charity's brokerage account. However, for donations involving physical share certificates, beneficial ownership can transfer upon physical delivery of an endorsed certificate — even before a brokerage account reflects the change. Charities accepting physical certificates should seek legal advice on how to document this transfer properly.

A useful analogy: giving someone a house key does not transfer ownership of the house. The transfer happens when they can actually use the key to get in. For shares, that moment is confirmed by the acquisition of beneficial ownership — not by paperwork alone.

The Legal Grounds for Revocation: What CRA Actually Found

The CRA's decision to revoke the Moon Gate Foundation's registered status was based on several overlapping compliance failures — not just one mistake. Each failure reinforced the others.

Incorrect Receipt Date

The shares were not in the Foundation's brokerage account on February 19, 2021. A donation receipt can only be issued for a gift that has been legally completed. Issuing a receipt before transfer is complete is not a minor irregularity — it is the issuance of an invalid receipt.

Incorrect Valuation

The Foundation used the February 2021 share price to calculate the receipt value. Because the shares had not transferred in February 2021, that price had no legal basis as the FMV for receipting purposes. The correct FMV — approximately $430,000 — was the price at the time of actual transfer in September 2022.

No Valid Gift Under Canadian Law

Canadian law requires animus donandi for a valid charitable gift. This means:

- A genuine, irrevocable intention to transfer property

- An actual transfer of that property

- The donor making themselves poorer for the donee's benefit

In February 2021, none of those conditions had been met. The donor had not parted with the shares. The CRA's position was straightforward: no completed gift means no valid receipt.

Private Benefit to the Donor

By issuing a receipt for shares the donor still effectively controlled, the Foundation provided a tax credit the donor was not entitled to receive. This engages CRA's private benefit rules — a serious and separate compliance failure that, on its own, can ground a revocation.

How CRA Revokes a Charity's Registered Status

Revocation is the most serious enforcement outcome available to the CRA. It is not a fine or a warning — it is the permanent end of registration unless successfully appealed.

When the CRA revokes a charity's registered status, the following consequences apply:

- The charity loses its tax-exempt status immediately

- It can no longer issue valid donation receipts

- The revocation is published in the Canada Gazette — publicly and permanently

- Directors may face personal exposure for prior receipts that are later disallowed

- The charity's assets may be subject to revocation tax if not transferred to a qualified donee

The 125% Penalty: A Consequence Even Without Revocation

Revocation is not the only financial consequence available to the CRA when a charity issues a false or inflated receipt. Under section 188.1(9) of the Income Tax Act, a charity that issues a receipt containing false information — including an overstated amount — can be assessed a penalty equal to 125% of the receipted amount.

In the Moon Gate Foundation's case, that calculation would have produced a penalty of approximately $6 million on a single receipt. CRA opted for revocation in this instance, but the 125% penalty remains an active tool in CRA's enforcement arsenal. Board directors of charities accepting non-cash donations should be aware that this penalty can be applied independently of, or in addition to, revocation proceedings.

This is not a theoretical risk. It is a statutory mechanism designed to deter exactly the kind of inflated receipting that occurred here.

The Moon Gate Foundation's revocation letter and the Foundation's legal response are available through the Investigative Journalism Foundation.

Compliance Checklist: What Charities Must Do Before Issuing a Receipt for Shares

For charities that accept donated securities, a clear internal process is not optional — it is a governance requirement. The steps below reflect what the Moon Gate Foundation failed to do.

Before issuing any receipt for donated shares, a charity must:

- Confirm the shares are in the charity's account. Contact the brokerage directly. Do not rely on a donor's word or a transfer instruction alone.

- Record the confirmed transfer date. This is the only date that can appear on the receipt.

- Obtain the FMV on the correct date using a consistent method. For publicly listed securities, CRA allows charities to use either the closing price on the date of transfer, or the average of the high and low trading prices on that date. Both are acceptable — but the charity must choose one method and apply it consistently across all donations of the same type. Document which method was used and retain the source data.

- Issue the receipt promptly after confirmation. Match the receipt to the actual transfer event — no pre-dating, no delay.

- Document every step. Retain brokerage confirmations, date-stamped communications, and FMV calculations in the charity's receipt file.

- Never issue a receipt based on a donor's representation alone. Independent verification is mandatory.

Charities that accept shares regularly should have this process written into their gift acceptance policy and reviewed by legal counsel. See also: Annual Checklist for Charity Board of Directors.

What Donors Need to Know About Timing a Share Donation

Donors are not passive bystanders when it comes to receipting compliance. If a charity issues an invalid receipt, the donor's tax credit may be disallowed — even if the donor acted in good faith.

Key points for any donor giving shares to a Canadian charity:

- The tax credit claimed is only as valid as the receipt it is based on

- If the receipt date or value is incorrect, CRA can reassess the donor's return

- Donors should confirm with their broker that the transfer has settled before filing their tax return

- A significant gap between instruction and settlement — as in the Moon Gate case — can indicate a problem worth investigating before a receipt is accepted

The 19-month gap in this case is an extreme example. But even a gap of a few weeks matters if share prices move significantly in that period.

Why This Case Stands Out — And What It Signals

The Moon Gate Foundation case is not just a receipting story. It reflects a broader pattern the CRA has identified in its enforcement work on in-kind donations.

The Foundation's profile — minimal program activity, a single large receipt, shares that declined sharply in value — is consistent with a category of charity the CRA watches closely: organizations where receipts appear to be the primary activity rather than charitable programming.

Key signals that draw CRA attention to in-kind donation arrangements:

- Large receipts relative to total charitable program spending

- Significant time gaps between claimed transfer dates and actual settlement

- Receipts for non-cash assets (shares, real property, art) without independent valuation documentation

- Donor-controlled assets that are receipted before actual disposition

CRA has increased its audit focus on donations of securities and private company shares in recent years. Charities accepting these gifts without legal and accounting oversight are operating at elevated risk.

Conclusion: The Real Cost of Getting a Receipt Wrong

The Moon Gate Foundation existed for 13 years, gave away $15,000, issued one disputed receipt, and is now no longer a registered charity. That outcome was not inevitable — it followed directly from a receipting process that did not meet the requirements of Canadian law.

For charities accepting non-cash donations, particularly shares, the lesson is operational: build a verification process, document every step, and do not issue a receipt until the transfer is confirmed. For donors, the lesson is to verify that the receipt received accurately reflects the transfer that actually occurred.

If a charity's gift acceptance policy does not specifically address how and when receipts are issued for donated securities, that gap should be addressed now — before a receipt, not after.

Charity Law Group works with Canadian registered charities on compliance, governance, and CRA matters. Contact us to review your gift acceptance and receipting policies.

Frequently Asked Questions

When can a charity issue a donation receipt for shares?

Only after the shares have been transferred into the charity's brokerage account and legal ownership has passed to the charity. The receipt date must match the actual transfer date — not the date of a signed form, broker instruction, or donor commitment.

What value should appear on a donation receipt for shares?

The fair market value of the shares on the date they were received into the charity's account. For publicly listed securities, this is typically the average of the high and low trading prices on that date.

What is animus donandi in Canadian charity law?

It is the legal requirement that a valid gift involve a genuine, irrevocable intention to transfer property and make the donor poorer for the recipient's benefit. A receipt issued before this transfer is complete does not satisfy the requirement and is not a valid receipt under Canadian law.

Can the CRA revoke a charity over a single incorrect receipt?

Yes. A single receipt that is materially incorrect in both date and value — particularly one that confers private benefit on the donor — can be grounds for revocation. The presence of other compliance concerns, as in the Moon Gate case, makes revocation more likely but is not always required.

What happens to a charity after CRA revokes its registration?

The charity immediately loses its tax-exempt status and its ability to issue donation receipts. The revocation is published in the Canada Gazette. It is permanent unless successfully appealed. The charity may also be subject to revocation tax on remaining assets.

Does the donor face consequences if a charity issues an incorrect receipt?

Potentially, yes. If CRA determines that a receipt is invalid, it can reassess the donor's return and disallow the tax credit — even if the donor did not cause or know about the error.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)