How to Calculate the HST Rebate for Charities in Canada

Published on

June 18, 2025

Last updated on

February 25, 2026

When your charity buys goods or services in Canada, you often pay Harmonized Sales Tax (HST). The good news is that registered charities can get a significant portion of that money back through the HST Public Service Bodies' (PSB) Rebate. This rebate helps reduce your operating expenses so more funds go towards your charitable programs.

Calculating the rebate means breaking down the total HST into its federal and provincial parts, then applying specific rebate rates based on your location and organization type. Each province has different rebate percentages, so understanding these details is key to maximizing your claim.

This guide walks through everything step by step: who qualifies, what rates apply, which forms to file, and the most common mistakes to avoid.

Understanding the HST Rebate for Charities

If your charity or nonprofit buys goods or services in Canada, you’ve likely paid the Harmonized Sales Tax (HST). The good news is that many registered charities and some nonprofits can get part of that money back from the government. This is called an HST rebate.

This guide will help you understand how to calculate your rebate, what rate applies, and which form you need to use. We’ve made it simple so anyone can follow along, even if it’s your first time.

What is the HST Rebate for Charities and Nonprofits?

When your organization buys something, you usually pay HST, which is a mix of federal and provincial taxes. The federal part is the GST (Goods and Services Tax), and the provincial part depends on where you are in Canada.

Registered charities and qualifying non-profit organizations can claim a rebate on a portion of the HST they pay. This helps them save money and put more funds toward their programs and services.

What Is the HST Rebate Rate for Charities?

Here's how the rebate usually works:

- 50% rebate on the federal part (GST) of the HST for registered charities

- Variable rebate on the provincial portion of the HST — the rate depends on the province where the expense was incurred. In Ontario, New Brunswick, and Newfoundland & Labrador, charities receive an 82% rebate on the provincial portion. In Nova Scotia and PEI, the rate is 50%.

- Qualifying NPOs (non-profit organizations that receive at least 40% of their funding from government sources) also qualify for the 50% federal rebate.

Not all provinces have an HST. Alberta and British Columbia charge only the federal 5% GST — so charities there can claim the 50% federal rebate but there is no provincial portion to rebate. Quebec uses a separate QST system described further below.

Registered charities that are also classified as public institutions — such as hospital authorities, universities, public colleges, or school authorities — are subject to different rebate rates under the Excise Tax Act. For example, a hospital authority in Ontario receives an 87% rebate on the federal portion, not the standard 50%. If your organization may qualify as a public institution, consult a charity tax specialist to determine the correct rates before filing.

What Is the HST Rebate Form for Nonprofits?

To apply for the rebate, you need to complete Form GST66 – Application for GST/HST Public Service Bodies' Rebate and HST Self-Government Refund. If your charity is in an HST province, you must also complete Form RC7066-SCH – Provincial Schedule – GST/HST Public Service Bodies' Rebate to claim the provincial portion. Both forms are typically filed together.

Here's what you'll need to prepare:

- Your total eligible expenses for the claim period

- The total amount of HST paid on those expenses

- The amount of rebate you are claiming

- Your charity's Business Number (BN) — if you do not have one, the CRA will assign one when you file

You can file online using the CRA's My Business Account, or you can mail a paper copy. Filing online is strongly recommended — it is faster, provides confirmation of receipt, and allows you to track your rebate status. The CRA typically processes online PSB rebate claims within 4 to 6 weeks. Paper submissions may take longer.

When Should You File?

You should file the rebate within four years from the end of the reporting period when you paid the HST. For example, if you paid HST during your fiscal year ending December 31, 2022, you generally have until December 31, 2026 to apply for that rebate.

If your charity is a GST/HST registrant, you must file Form GST66 for each reporting period (monthly, quarterly, or annually depending on your assigned frequency). If your charity is a non-registrant, you can typically file annually within two years of the end of your claim period — though the four-year outer limit still applies.

Eligibility Criteria for Charities

To claim an HST rebate, charities must meet specific rules set by the Canada Revenue Agency (CRA). These rules define who qualifies, the types of charities and public service bodies (PSBs) eligible for rebates, and how designated charities differ from other charities. Understanding these details helps us determine our rebate eligibility and ensures we file correctly.

Who Qualifies as a Charity?

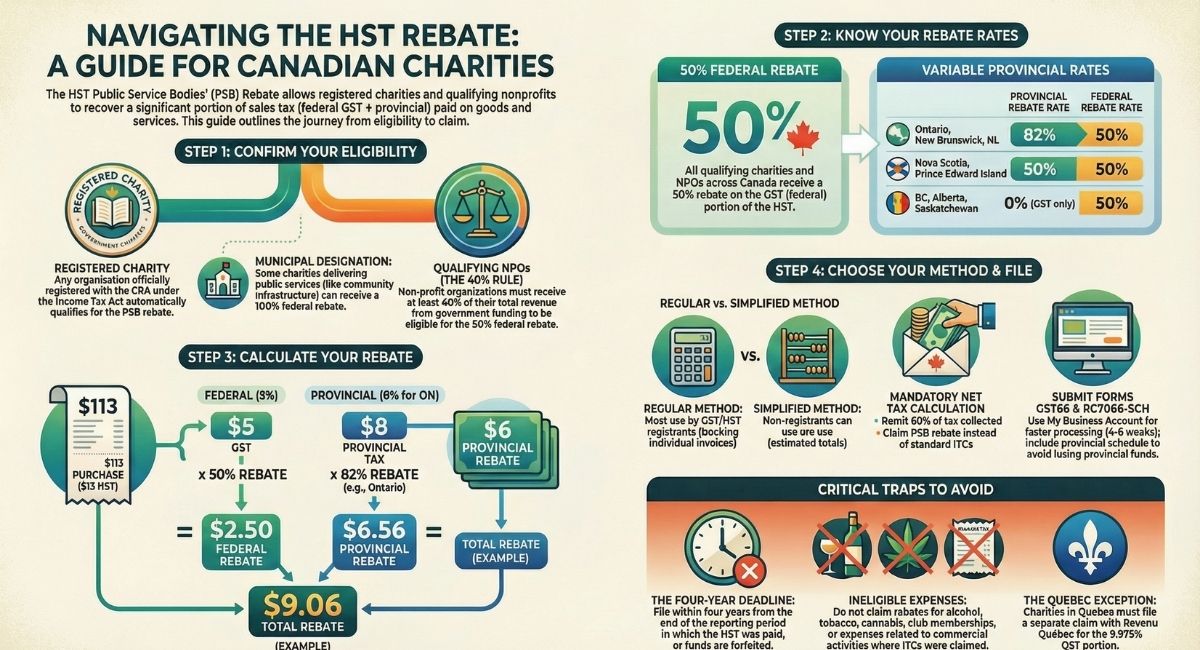

We qualify as a charity if we are a registered charity listed with the CRA. This means we must have obtained official charitable status under the Income Tax Act. Only registered charities can claim the full HST rebate.

Qualifying charities include those involved in religious, educational, charitable, or other recognized purposes. Our activities must match the CRA’s definition of charitable work, and we must comply with reporting and operational rules.

Important distinction — Charities vs. NPOs: In Canadian law, a registered charity and a non-profit organization (NPO) are legally distinct entities with different rebate rules under the Excise Tax Act. All registered charities (other than public institutions) automatically qualify for the PSB Rebate. An NPO, by contrast, does not automatically qualify. To be eligible, an NPO must meet the "qualifying NPO" test, which requires that at least 40% of its total revenue comes from government funding. This threshold is a strict CRA requirement, not a general guideline. If your NPO does not meet this threshold, it is not eligible for the PSB rebate. See CRA Guide RC4034 for the full qualifying NPO rules.

Types of Eligible Charities and Public Service Bodies

Eligible organizations include registered charities, designated charities, and other public service bodies such as hospitals, universities, and Canadian amateur athletic associations.

The CRA allows these groups to claim a rebate on a portion of the HST they pay. The rebate rate varies depending on the type of organization. Note that public institutions — hospitals, universities, and similar bodies that are also registered charities — are subject to different rates than standard registered charities, and should not apply the standard 50%/82% rates without first confirming their classification.

The gross revenue test does not determine a charity's rebate rate, and it does not affect charitable exemption status. Instead, it determines whether a charity qualifies as a small supplier — meaning it is not required to register for and collect GST/HST. A charity is generally a small supplier if its annual gross revenue is $250,000 or less (including grants and donations, not just commercial revenue). Even if gross revenue exceeds this amount, a charity may still be a small supplier if its annual taxable supplies are $50,000 or less. The PSB Rebate rate itself — 50% federal and, for example, 82% on the Ontario provincial portion — is fixed by organization type and does not change based on revenue. See CRA Info Sheet GI-067 for full small supplier guidelines for charities.

Designated Charities vs Other Charities

Designated charities are a specific category recognized by the CRA with eligibility for a higher rebate rate. They include organizations primarily involved in registered charitable activities but also serve as public service bodies.

These designated charities often have different rebate rates and may be eligible for rebates on both federal and provincial parts of HST at a higher percentage compared to regular charities.

Other charities that do not meet the criteria for being designated may only be eligible for partial rebates or the federal portion of HST. Understanding our classification helps us determine the correct rebate percentage to claim.

Can a Charity Qualify for the 100% Municipal Rebate?

Most charities receive the standard 50% federal rebate on GST/HST paid. However, the Excise Tax Act defines the term "municipality" more broadly than most people expect. The CRA has the authority to designate certain charities and non-profit organizations as municipalities for GST/HST rebate purposes — which would qualify them for a 100% rebate instead of the standard 50%.

To receive municipal designation, an organization must apply to the CRA and demonstrate that it performs functions typically carried out by municipal governments — such as operating community infrastructure, managing public spaces, or delivering publicly funded services on behalf of a government body.

This is not widely known, and many eligible charities miss this higher rebate entirely. If your charity receives significant government funding and delivers public services, it is worth speaking with a charity tax specialist to explore whether municipal designation could apply.

Taxable and Exempt Supplies for Charities

When we deal with GST/HST as charities, it's key to understand the differences between taxable, exempt, and zero-rated supplies. Each type affects how much tax we collect or pay, and what rebates we can claim. This knowledge helps us manage our finances while following tax rules.

Taxable Supplies and HST Implications

Taxable supplies are goods or services that are subject to GST/HST. We must charge and collect tax on these supplies when dealing with customers in participating provinces. The tax rate depends on the province, ranging from 5% GST alone to combined HST rates in places like Ontario and Nova Scotia.

When we make taxable sales, we need to register for GST/HST if our taxable revenues exceed $50,000 in a single calendar quarter or over the previous four quarters. We must charge GST/HST on sales and report it. Input tax credits (ITCs) can be claimed for GST/HST paid on purchases related to our taxable activities.\

Note that some real property sales by charities are also taxable, and tax must be remitted accordingly. Proper accounting of these taxable supplies ensures compliance and accurate rebate claims.

Exempt Supplies and Their Impact on Rebates

Exempt supplies include goods and services that do not attract GST/HST. Charities often provide exempt supplies, such as certain health, educational, or social services. When we supply exempt goods or services, we cannot charge GST/HST or claim ITCs on related purchases.

Because we can’t recover GST/HST on expenses tied to exempt supplies, these costs reduce the amount of rebate we may receive. However, charities using the net tax calculation method can claim a public service bodies (PSB) rebate for GST/HST amounts on eligible expenses, even if these expenses relate to exempt activities.

This rebate helps offset some costs but does not cover GST/HST paid on all exempt-related purchases. Understanding which supplies are exempt lets us plan how we track and claim rebates correctly.

Zero-Rated Supplies for Charities

Zero-rated supplies are taxable but charged at a 0% GST/HST rate. This means we do not collect tax on the sale but can still claim input tax credits for GST/HST paid on purchases related to these sales.

Examples relevant to charities include certain printed books and some food products. Zero-rated supplies are important because they allow us to recover GST/HST costs even though we do not charge tax to clients.

We must carefully identify zero-rated supplies in our accounting to ensure we claim all the ITCs available without charging unnecessary GST/HST. This keeps our tax reporting accurate and helps maximize our rebate claims.

Net Tax Calculation Methods for Charities

We must use specific calculation methods to figure out the net tax for charities. These methods depend on whether our charity is registered for GST/HST or not. Correctly applying the method impacts how we claim input tax credits and rebates, and impacts the amounts we report on our GST/HST return.

Net Tax Calculation for GST/HST Registrant Charities

If your charity is registered for GST/HST, you are generally required by law to use the Net Tax Calculation for Charities as outlined in CRA Info Sheet GI-066. This is a mandatory method — not an optional one — unless your charity qualifies for a specific exception or makes a formal election to use the regular method instead.

Under this mandatory calculation:

- Your charity remits 60% of the GST/HST collected on taxable supplies rather than 100%.

- In exchange, you generally cannot claim Input Tax Credits (ITCs) on most purchases the way a standard registrant would.

- Instead of ITCs, you claim the PSB Rebate on eligible purchases.

This interaction between the 60% remittance rule and the PSB Rebate is often misunderstood. The rebate is not simply applied to all expenses independently — for registrant charities, the two calculations work together on the same GST/HST return. Charities that file as registrants without applying the mandatory net tax method risk filing incorrectly and may face CRA adjustments.

On the GST/HST return, amounts related to the net tax calculation appear at line 103 (tax collected) and line 106 (input tax credits claimed). Because this method has significant implications for how much GST/HST you remit and how much you recover through the rebate, we strongly recommend working with a charity accountant to ensure it is applied correctly.

We must remember that charities classified as public institutions, or those that have made a valid election to use the regular method, do not apply this mandatory calculation.

Net Tax Calculation for Non-Registrant Charities

For charities not registered for GST/HST, the net tax calculation process is different. Since we do not charge GST/HST, we cannot claim input tax credits like registrants do.

However, non-registrant charities may still be eligible for certain rebates on GST/HST paid on their purchases. We calculate our net tax in relation to rebates claimed, often using Form GST26 for reporting.

Because these charities do not file full GST/HST returns, the focus is on identifying amounts eligible for rebates rather than on tax collected or credits claimed. The net tax calculation here is simpler but requires careful review to ensure expenses qualify under CRA rebate rules.

We must follow CRA instructions carefully to correctly report and receive the rebate allowed for non-registrant charities.

Simplified Method vs. Regular Method: Which Should Your Charity Use?

When calculating the PSB rebate, charities can use either the regular method or the simplified method. The CRA allows eligible charities to choose the method that best suits their record-keeping capacity.

Regular Method You calculate non-creditable tax charged on each eligible purchase individually. This method is more precise and may produce a higher rebate if you have detailed expense records. It is required for charities that are GST/HST registrants.

Simplified Method You use total purchases to estimate the rebate without tracking each invoice separately. This is better suited for smaller charities or those with limited accounting staff. It may result in a slightly lower rebate in some cases. Available to non-registrant charities only.

If you are a GST/HST registrant subject to the mandatory net tax calculation, you must follow the rules specific to that method. Non-registrant charities may use either the regular or simplified method. Note that switching methods requires CRA approval. Always confirm your choice with a charity accountant to ensure you are maximizing your eligible rebate.

Step-by-Step Process to Calculate the HST Rebate

Calculating the HST rebate involves identifying which expenses qualify, separating non-creditable tax, applying the correct rebate rates, and dealing with capital or real property costs properly. Each step requires careful attention to ensure the amount we claim is accurate and reflects the rules set by the Excise Tax Act.

Calculating Eligible Expenses

We start by determining which expenses are eligible for the HST rebate. Generally, expenses must be for goods or services used directly in our charity’s day-to-day activities. This includes office supplies, utilities, and contracted services.

Not all purchases are eligible. The following expenses are NOT eligible for the PSB rebate:

- Club memberships where the main purpose is dining, recreational, or sporting activities

- Tobacco products, cannabis products, and alcoholic beverages (unless included in the price of a meal you supply)

- Property and services acquired to provide long-term residential accommodation (with limited exceptions for seniors, youth, or disability-focused housing)

- Expenses related to commercial (taxable) activities where ITCs are already being claimed

Keep all original receipts and invoices showing the HST amount paid. Proper documentation is essential for audit purposes.

Determining Non-Creditable Tax Charged

Non-creditable tax charged means the portion of HST or GST that we can’t claim back as an input tax credit (ITC) or rebate. We must identify this amount because it affects the rebate total.

The Excise Tax Act helps define when tax is non-creditable. For charities, non-creditable tax usually shows up on goods or services not used directly for charity functions or where the rebate doesn’t apply.

We separate the non-creditable tax from the creditable amounts before applying rebate rates. This ensures we don’t claim taxes that the Canada Revenue Agency (CRA) won’t approve. Keeping accurate records here is essential for audit purposes.

Applying the Correct Rebate Rates

Once we have our eligible expenses and non-creditable tax sorted, we apply the rebate rates determined for our type of organization and province.

For registered charities (excluding public institutions), the federal GST portion has a 50% rebate rate. The provincial portion varies. In Ontario, for example, the rebate on the provincial part is 82%. Other provinces like Prince Edward Island offer a 50% provincial rebate.

We calculate the rebate by splitting the total HST paid into its federal and provincial parts, then multiplying each by their respective rebate rates. Using a simple table helps:

Adding these gives us the total HST rebate claim.

How to Calculate the HST Rebate

Let’s walk through an example:

Imagine your charity bought office supplies and paid $113 in total. That includes $100 for the items and $13 HST (which is 13% in Ontario).

Step 1: Break the HST into federal and provincial parts

- Ontario’s HST rate is 13%

- 5% is federal (GST) = $5

- 8% is provincial = $8

Step 2: Apply the rebate rate

- Federal GST rebate (50% of $5) = $2.50

- Ontario portion rebate (82% of $8) = $6.56

Step 3: Add the rebates

$2.50 + $6.56 = $9.06 total rebate

So your charity can claim back $9.06 out of the $13 HST paid.

Accounting for Capital and Real Property

Capital property, including buildings and land, requires special treatment under the rebate rules. We need to track HST paid on these items separately because capital acquisitions have different rebate calculations.

If the property is used for charitable activities, a portion of the HST paid on the purchase or improvement may be refundable as a Public Service Bodies’ Rebate (PSB rebate). The rebate may be spread over several years if the property is capital in nature.

We must also consider whether the property use changes, which affects future rebate claims. Properly accounting ensures we comply with the Excise Tax Act and maximize eligible rebates on capital and real property.

Common Mistakes Charities Make When Claiming the HST Rebate

The following mistakes result in charities either underclaiming their rebate or facing a CRA review. Review these carefully before filing your next claim.

1. Filing late or missing the four-year deadline The HST rebate must be claimed within four years of the end of the reporting period in which the tax was paid. Many charities lose recoverable money simply because the claim is overlooked until it is too late.

2. Using the wrong provincial schedule Some charities file Form GST66 without attaching Form RC7066-SCH for the provincial portion. This means they recover only the federal rebate and completely miss the provincial portion — which in Ontario is worth up to 82% of the 8% provincial component.

3. Claiming rebates on ineligible expenses Club memberships, alcoholic beverages, tobacco and cannabis products, and expenses related to commercial activities do not qualify for the PSB rebate. Including these inflates your claim and can trigger a CRA review.

4. Not claiming the rebate at all Non-registrant charities (those that do not charge GST/HST) are still eligible for the PSB rebate. Many assume they cannot claim because they are not registered. This is incorrect — non-registrant charities are entitled to file Form GST66.

5. Failing to track government funding for NPO eligibility Non-profit organizations need at least 40% of their funding from government sources to qualify for the 50% federal rebate. If this funding is not clearly labelled in financial statements under GIFI code 8242 ("Subsidies and grants"), the CRA may disallow the claim.

6. Registrant charities not applying the mandatory net tax calculation. If your charity is registered for GST/HST, you are generally required to use the Net Tax Calculation for Charities, which means remitting 60% of GST/HST collected and claiming the PSB Rebate in place of most ITCs. Filing as though you can claim full ITCs and the PSB Rebate independently is incorrect and may result in a CRA reassessment.

Special Provincial Considerations and Other Rebate Types

We need to consider different tax rules depending on the province where the charity operates. Some provinces have unique tax systems, rebate options, or requirements that affect how much a charity can claim back. Understanding these details will help us maximize the rebates available to our organisation.

Quebec Sales Tax (QST) and Charities

In Quebec, the sales tax system differs because the Quebec Sales Tax (QST) replaces the provincial part of the HST. The QST rate is 9.975%. Registered charities must navigate both the GST (administered by the CRA) and the QST (administered by Revenu Québec) to claim their full rebates.

Registered charities in Quebec file two separate rebate claims: one with the CRA for the federal GST portion using Form GST66, and one with Revenu Québec for the QST portion. The QST rebate structure for charities is distinct from the HST provincial rebates in other provinces — consult Revenu Québec's current guidance or a charity accountant for the applicable rebate rate.

Charities not registered for QST should not charge it but may still be eligible to claim a QST rebate on eligible purchases. Follow the specific deadlines and procedures set by both the CRA and Revenu Québec.

Point-of-Sale Rebates and Participating Provinces

In some provinces, charities and qualifying nonprofits can receive point-of-sale rebates on certain goods and services. This means the vendor reduces the HST amount charged at the time of purchase, so the organisation pays less upfront.

These provinces include Ontario, Nova Scotia, New Brunswick, and Newfoundland and Labrador. The point-of-sale rebate typically matches the rebate rates charities would claim later through forms.

For purchases in provinces without point-of-sale rebates, like Prince Edward Island and British Columbia, we must pay full HST and claim the rebate later through the CRA using forms such as Form GST66.

Point-of-sale rebates simplify budgeting since we don't have to wait for reimbursement. However, we must provide vendors with proof of our charity status or exemption certificates for the rebate to apply.

Other Rebates for Charities and Public Service Bodies

Besides the standard HST rebate, charities may qualify for other rebates or refunds:

- PSB Rebate under section 259 of the Excise Tax Act: The main rebate mechanism described throughout this guide.

- Self-Government Refund: Specific to Indigenous self-governing bodies operating under certain agreements, allowing them to recover GST/HST paid on eligible expenses.

- Printed Books Rebate: A 100% rebate of the GST or federal part of HST paid on qualifying printed books, audio recordings of printed books, and printed versions of religious scriptures. This is a distinct rebate separate from the PSB rebate.

- New GST/HST Rebate for Purpose-Built Rental Housing (PBRH): Introduced in 2023 and applicable for charities involved in affordable housing construction. If your charity is constructing or substantially renovating qualifying rental housing, speak with a charity accountant about this rebate.

There are also specific rebates available for services provided by auctioneers or agents acting on behalf of charities. These follow detailed rules and usually require additional documentation during claims.

Understanding these different rebates ensures that we capture all possible tax relief options relevant to our organisation’s activities.

Final Tips for Canadian Charities

- Confirm your registered status. Only registered charities and qualifying NPOs — those that meet the strict 40% government funding threshold — can apply for the PSB rebate. If you are unsure about your organization's status, verify it through the CRA's charity listings at canada.ca.

- Keep all receipts. Maintain original invoices and receipts for all purchases where HST was charged. The CRA may request documentation to support your rebate claim.

- Do not skip the provincial schedule. Always attach Form RC7066-SCH when claiming the provincial portion of the HST rebate in an HST province. Missing this form means leaving a significant portion of your rebate unclaimed.

- Registration is not required to claim. You do not need to be a GST/HST registrant to file the PSB rebate. Non-registrant charities are entitled to claim using Form GST66.

- Track the four-year limit. Set a calendar reminder to ensure rebate claims are filed well before the four-year deadline. Missed deadlines mean forfeited refunds.

- Review your NPO's government funding percentage. If you operate a nonprofit rather than a registered charity, make sure government grants and subsidies are clearly labelled in your financial statements under GIFI code 8242 so the 40% funding threshold can be verified by the CRA.

If registered, confirm your net tax calculation method. Registrant charities must generally use the mandatory Net Tax Calculation for Charities. Speak with a charity accountant before filing to ensure you are applying the correct method and not leaving money on the table — or inadvertently overclaiming.

By claiming the HST rebate, Canadian charities and nonprofits can reduce their costs and free up more money to help their communities. It's worth taking the time to understand the rules and apply them properly.

If you need help, speak with an accountant or bookkeeper who specializes in charity and nonprofit accounting, tax filing, and bookkeeping or visit the CRA website for more details.

Frequently Asked Questions

We will cover how to figure out the HST rebate for charities, understand tax credits for donations, and explain GST rules for charities in Canada. We will also show the basic HST calculation and limits on tax deductions for donations.

How to calculate HST rebate for charities in Canada?

To calculate the HST rebate, first separate the total HST paid into federal (GST) and provincial parts. Apply the rebate rates: registered charities (excluding public institutions) usually get 50% back on the federal part and a percentage (such as 82% in Ontario) on the provincial part. Add these amounts together to find the total rebate your charity can claim. Registrant charities must also factor in the mandatory net tax calculation, which affects how the rebate interacts with GST/HST remittances.

How to calculate charitable donation tax credit in Canada?

The tax credit is based on the amount donated.

For federal tax, there is a base rate (15%) on the first $200 donated and a higher rate (29%) on amounts over $200.

Provinces add their own credits, which vary by region.

Multiply your donation by the combined federal and provincial rates to get the total tax credit.

What is the formula for calculating HST?

HST is calculated by multiplying the purchase price by the HST rate of the province.

For example, if the HST rate is 13%, the formula is: Purchase Price × 0.13 = HST amount.

This total HST includes both the federal GST and the provincial portion.

Do Canadian charities pay GST?

Generally, registered charities must charge GST/HST if they provide taxable goods or services.

However, many charities qualify for rebates on the GST/HST they pay when buying goods and services.

Certain supplies made by charities may be exempt, so not all activities require charging GST/HST.

Does GST apply to charities?

GST applies to charities on taxable goods and services, but some charity activities are exempt from GST.

Charities are often eligible for partial rebates to recover some of the GST/HST they pay.

The rules depend on the charity’s registration status and the types of supplies made.

What is the maximum tax deduction for charitable donation?

The maximum tax credit depends on your income and province.

In general, the federal credit rates apply up to annual donation limits based on income.

Any donation amount exceeding these limits may be carried forward for up to five years.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)