How Much Surplus Can Canadian Charities Have?

When we run a Canadian charity, we face the challenge of managing surplus funds while staying compliant with regulations.

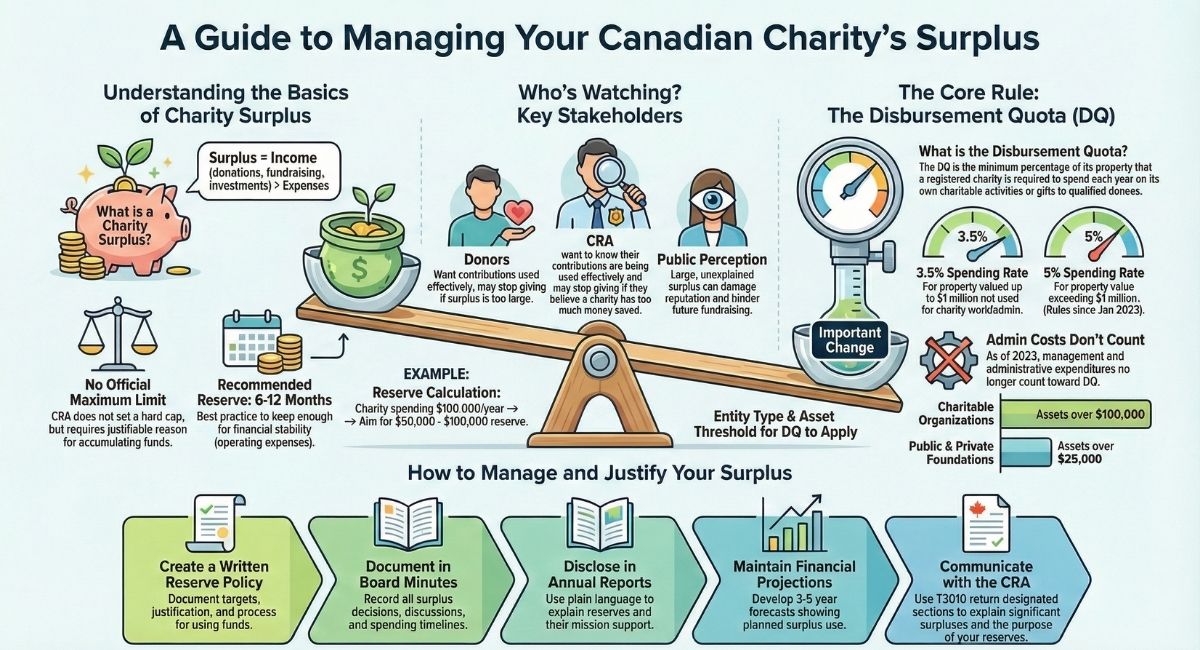

Canada has no official maximum surplus limits for charities. However, we must spend minimum amounts annually through disbursement quotas: 3.5% on property up to $1 million and 5% on amounts exceeding $1 million. We can accumulate reserves with proper justification and transparency.

In this guide, we'll explore current surplus regulations, recommended reserve amounts, and best practices for managing charity funds in 2025.

What Is Charity Surplus?

Surplus happens when we bring in more money than we spend. Think of it like having $100 to use but ending up with $120 at day's end. That extra $20 becomes our surplus.

We create surplus through donations, fundraising events, and investment returns. The Canada Revenue Agency (CRA) watches how we handle this extra money.

Current Disbursement Quota Rules

For property equal to or less than $1 million, the DQ rate remains at 3.5%. On the portion of property exceeding $1 million, the DQ rate increases to 5%. These rules started in January 2023.

We must spend a minimum amount each year on charitable activities. The disbursement quota is the minimum amount a registered charity is required to spend each year on its own charitable activities or on qualifying disbursements.

The calculation works like this: We take our property not used for charity work or administration. The threshold depends on your charity type:

- Charitable Organizations: If assets exceed $100,000, you must spend 3.5% annually (and 5% on amounts over $1 million)

- Public and Private Foundations: If assets exceed $25,000, the DQ applies at the same rates

Important Change: Management and administrative expenditures no longer count toward meeting your disbursement quota. You must spend the required percentage strictly on charitable activities or qualifying disbursements to qualified donees.

No Official Surplus Limits

Canada has no hard rules about maximum surplus amounts. The CRA says it's okay for charities to have a surplus if they have a good reason, like saving up for a big project.

We can accumulate money for valid reasons. These include future projects, emergency funds, or planned expansions. The key is having clear justification.

Recommended Surplus Amounts

It's recommended that charities keep enough money to cover 6-12 months of their expenses as a surplus. This gives us financial stability.

If we spend $100,000 yearly, we should aim for $50,000 to $100,000 in reserves. For monthly costs of $10,000, we need $60,000 to $120,000 as our safety net.

We should plan for special projects too. Major equipment purchases or building renovations require advance savings.

Who Monitors Our Surplus?

Three groups care about our surplus levels. The CRA ensures we follow charity rules. Our donors want transparency about fund use. The public watches our financial management.

If people hear that a charity has tons of extra money, they might question why it needs donations. This could hurt the charity's reputation and make it harder for them to raise funds in the future.

Managing Surplus Properly

We must be transparent about our savings. Clear communication prevents donor concerns. We should explain why we hold reserves and how we'll use them.

Good surplus management includes regular financial reviews. We track income and expenses monthly. Board oversight ensures responsible money handling.

We document reasons for accumulating funds. Written policies guide surplus decisions. Annual reports show how we use reserved money.

How Much Surplus Can Canadian Charities Accumulate?

Many charities wonder how much extra money they can accumulate while still being considered a charity. This is a common concern among Canadian charities. In simple terms, a surplus is when a charity ends up with more money than it needs, which goes against its primary goal.

Understanding Surplus: A surplus happens when a charity makes more money than it spends. Imagine having $100 to spend but ending with $120 at the end of the day. That extra $20 is your surplus.

Who Cares About Surplus?

Three main groups are interested in how much surplus a charity has: the Canada Revenue Agency (CRA), donors, and the general public.

Canada Revenue Agency (CRA): The CRA is like the referee for charities. They want to ensure charities do what they're supposed to do with their money. The CRA says it's okay for charities to have a surplus if they have a good reason, like saving up for a big project. But if a charity is hoarding money for no good reason, that could be a problem. Let's say a charity wants to build a new community center. It's okay for them to save up money for that. But if they're putting money in the bank year after year with no plan, that might not be okay with the CRA.

Donors: Donors are the people who give money to charities. They want to know that their money is being used wisely. If they see that a charity has a lot of extra cash, they might think it doesn't need their donation. This could lead them to give their money to a different charity instead. Imagine you want to donate to a charity that helps homeless animals. If you see that they already have lots of money in the bank, you might give it to a different charity that needs it more.

Public Perception: The general public's opinion of a charity is important, too. If people hear that a charity has tons of extra money, they might question why it needs donations. This could hurt the charity's reputation and make it harder for them to raise funds in the future. For example, if a charity always asks for donations, but then people find out they have lots of money saved up, they might feel the charity is dishonest.

How Much Surplus Should a Charity Have?

It's recommended that charities keep enough money to cover 6-12 months of their expenses as a surplus. If a charity spends $100,000 a year, they should aim to have between $50,000 and $100,000 saved up. If a charity spends $10,000 monthly on rent, salaries, and other costs, it should try to have between $60,000 and $120,000 in the bank as a safety net.

Managing Surplus

Charities should plan for special projects and maintain adequate reserves. As of January 1, 2023, the CRA no longer accepts applications to accumulate property outside of the disbursement quota calculation. This means all property must be included in your DQ calculation, regardless of whether you're saving for a specific future project.

When planning for major expenditures like building renovations or equipment purchases, charities must:

- Include all accumulated funds in their DQ calculation

- Ensure they meet their annual spending requirements through charitable activities

- Document their reserve purposes clearly in board minutes and financial statements

- Maintain transparency with donors about why funds are being held

For example, if a charity wants to build a new playground that will cost $50,000, it can save toward this goal, but those funds remain part of the property base for DQ calculations. The charity must still meet its annual spending requirement on charitable activities throughout the saving period.

Charities can benefit from having reserves, but they must balance accumulation with their annual disbursement obligations. They must also be transparent about their savings and follow the CRA's current rules. This will keep their donors happy and their reputation intact.

How to Document Your Surplus Justification

Proper documentation protects your charitable status and maintains donor trust. Here's what to include:

Board Minutes

Record all surplus-related decisions in board meeting minutes. Document discussions about reserve targets, accumulation purposes, and spending timelines. Include specific dollar amounts and voting results for transparency.

Written Reserve Policy

Create a formal policy stating your reserve targets, justification, and review process. Include specific percentages or dollar amounts based on your operating budget. Your policy should outline when reserves can be used and who authorizes expenditures.

Annual Report Disclosure

Explain your surplus and reserves in your annual report. Use plain language to help donors understand why you hold these funds. Show how reserves support your charitable mission and future programs.

Multi-Year Financial Projections

Maintain 3-5 year financial forecasts showing planned surplus use. Include projected income, expenses, and how reserves will be deployed. Update these projections annually as circumstances change.

CRA Communication

When filing your T3010 return, clearly explain significant surpluses in the designated sections. Proactive communication prevents future CRA inquiries. Be specific about reserve purposes and timelines.

Excess Disbursements and Carryovers

If a registered charity spends more on its charitable activities or by way of gifts to qualified donees than the disbursement quota in its fiscal year, this is known as a disbursement excess. Disbursement excesses can be carried forward for five years or carried back one year.

This flexibility helps us manage year-to-year variations. Some years we spend more, others less. The system balances out over time.

Understanding the 2023 Disbursement Quota Changes

The DQ remains 3.5% on the portion of property not used in charitable activities and administration up to $1 million, and increases to 5% on property exceeding $1 million. The new DQ applies to charities' financial periods starting on or after January 1, 2023.

These changes affect larger charities most. Organizations with over $1 million in assets must spend more annually. The goal is increasing charitable impact.

As we move through 2025, these regulations are now well-established. Charities should have systems in place to calculate and track their disbursement requirements accurately.

Practical Tips for Surplus Management

We should create written reserve policies. These explain our surplus targets and usage plans. Board approval adds legitimacy to our approach.

Regular financial monitoring helps us stay compliant. Monthly reviews catch issues early. Annual assessments ensure we meet disbursement requirements.

Communication matters greatly. We tell donors about our reserves. Transparency builds trust and ongoing support.

Risk Factors to Consider

If a material part of the excess is accumulated each year and the balance of accumulated excess at any time is greater than the association's reasonable needs to carry on its no profit activities, problems may arise.

Large surpluses without clear purposes raise red flags. The CRA questions excessive accumulation. We need documented reasons for holding money.

Economic changes affect our planning. Inflation impacts operating costs. Investment returns vary yearly. We adjust surplus targets accordingly.

Best Practices for Canadian Charities

We maintain 6-12 months of operating expenses as reserves. Clear policies guide surplus decisions. Regular communication keeps stakeholders informed.

Annual budget planning includes surplus targets. We document reasons for accumulating funds. Board oversight ensures responsible management.

Professional advice helps with complex situations. Charity lawyers and accountants provide guidance. Regular reviews keep us compliant with changing rules.

Real-World Surplus Scenarios for Canadian Charities

These examples show how different organizations approach surplus management:

Scenario 1: Youth Sports Organization

• Annual budget: $200,000

• Current surplus: $180,000

• Justification: Saving for new sports facility ($400,000 project over 3 years)

• CRA approach: Documented capital campaign plan with fundraising timeline, architect plans, and land acquisition agreement

• Key documentation: Board-approved building fund policy, quarterly progress reports, separate restricted fund accounting

Scenario 2: Mental Health Charity

• Annual budget: $500,000

• Current surplus: $400,000

• Justification: 8-month operating reserve plus emergency fund

• CRA approach: Board-approved reserve policy stating 6-8 month target with annual review requirements

• Key documentation: Risk assessment showing revenue volatility, historical cash flow analysis, written investment policy

Scenario 3: Arts Education Nonprofit

• Annual budget: $150,000

• Current surplus: $60,000

• Justification: Equipment replacement fund ($30,000) plus 3-month reserve ($37,500)

• CRA approach: Separate restricted and unrestricted fund accounting with clear allocation purposes

• Key documentation: Equipment replacement schedule, depreciation tracking, fund restriction policies

Scenario 4: Community Food Bank

• Annual budget: $400,000

• Current surplus: $250,000

• Justification: Building expansion ($150,000) plus 6-month reserve ($200,000)

• CRA approach: Architectural plans filed, construction permits obtained, fundraising campaign launched

• Key documentation: Construction contract, building permit, contractor quotes, project timeline with milestones

Conclusion

We can hold surplus funds with proper justification. No maximum limits exist, but we must spend minimum amounts annually. Transparency and good planning protect our charitable status.

Smart surplus management strengthens our organization. We balance current needs with future planning. Clear policies and open communication maintain donor trust while ensuring regulatory compliance.

As we navigate 2025, remember that the CRA closely monitors surplus accumulation. Document everything, communicate openly with stakeholders, and review your policies regularly. Stay informed about regulatory changes and adjust your strategies accordingly.

For complex surplus and disbursement quota questions, professional legal guidance is essential. The charity law experts at www.charitylawgroup.ca specialize in helping Canadian charities navigate surplus regulations, compliance issues, and strategic fund management.

Frequently Asked Questions

Here are the most common questions we receive about Canadian charity surplus and donation regulations.

Is there a limit on charitable donations in Canada?

There's no limit on how much you can donate to Canadian charities. However, tax credits are capped at 75% of your net income for most donations, plus 25% of any capital gains from donating appreciated property.

How much can you carry over in a registered charity?

Registered charities can carry forward disbursement excesses for five years or carry them back one year. If you spend more on charitable activities than your required disbursement quota in a fiscal year, you create a disbursement excess that can offset future requirements. There's no specific limit on accumulated funds, but excessive accumulation without clear charitable purpose may trigger CRA scrutiny.

How much money can a registered charity have in their bank account?

There's no legal limit on bank account balances for Canadian registered charities. However, charities must justify large accumulations and meet annual disbursement quota requirements. For charitable organizations, the DQ applies if assets not used for charitable activities exceed $100,000. For foundations, it applies if such assets exceed $25,000.

What about non-profit organizations (NPOs)?

Non-profit organizations and registered charities are legally distinct entities in Canada. NPOs operate under section 149(1)(l) of the Income Tax Act and do not have disbursement quotas. However, NPOs must meet a strict annual test: they must be operated exclusively for social welfare, civic improvement, or any other purpose except profit.

While there's no hard cap on NPO bank balances, organizations must be careful. If an NPO accumulates a surplus that is not tied to a specific, documented future activity, the CRA may deem it to have a "profit purpose," which would disqualify it from its tax-exempt status. NPOs should maintain clear documentation showing how accumulated funds support their non-profit purposes.

Key differences between NPOs and registered charities:

- NPOs cannot issue donation tax receipts

- NPOs do not have disbursement quota requirements

- NPOs must prove they operate exclusively for non-profit purposes

- Registered charities can issue tax receipts and must meet annual spending requirements

Can charities invest money in Canada?

Yes, Canadian charities can invest their funds. Common investments include GICs, bonds, mutual funds, and stocks. Investment income counts toward disbursement quota calculations, and charities must follow prudent investment practices.

What is the maximum allowed for charitable donations?

Individuals can claim charitable tax credits up to 75% of their net income, plus 25% of any taxable capital gain from donating appreciated property. Unused donation amounts can be carried forward for up to five years.

Legal Sources & References

- CRA: Accumulation of Property

- CRA: Disbursement Quota Calculation

- CRA: Annual Spending Requirement (DQ)

- CRA: Differences between registered charities and non-profit organizations

- CRA Income Tax Guide - Non-Profit Organization Information Return (T1044)

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

.png)