How to Start a Charity Foundation in Canada: Expert Guide

Published on

July 21, 2025

Last updated on

April 13, 2026

You've built a successful business or enjoyed a rewarding career, and now you want to give back in a meaningful, lasting way. Maybe you're passionate about education, healthcare, environmental protection, or helping vulnerable populations. A charitable foundation feels like the right vehicle to make a significant impact while creating a lasting legacy.

But here's what most people don't realize when they first consider starting a foundation: it's not just about having good intentions and writing checks. Foundations in Canada are sophisticated legal structures with specific requirements, ongoing obligations, and strategic considerations that can make or break their effectiveness.

The difference between a foundation that thrives for generations and one that struggles or even fails often comes down to decisions made during the setup phase. Choose the wrong structure, underestimate funding requirements, or misunderstand governance obligations, and you could create problems that plague your foundation for years.

The good news is that with proper planning, professional guidance, and realistic expectations, starting a charitable foundation can be one of the most rewarding ways to make a lasting difference. Let's walk through everything you need to know to establish a foundation that achieves your philanthropic goals while maintaining full compliance with Canadian law.

This guide has been updated for 2026 to reflect current CRA processing timelines, disbursement quota rates, and registration requirements.

Step-by-Step: How to Start a Charitable Foundation in Canada in 2026

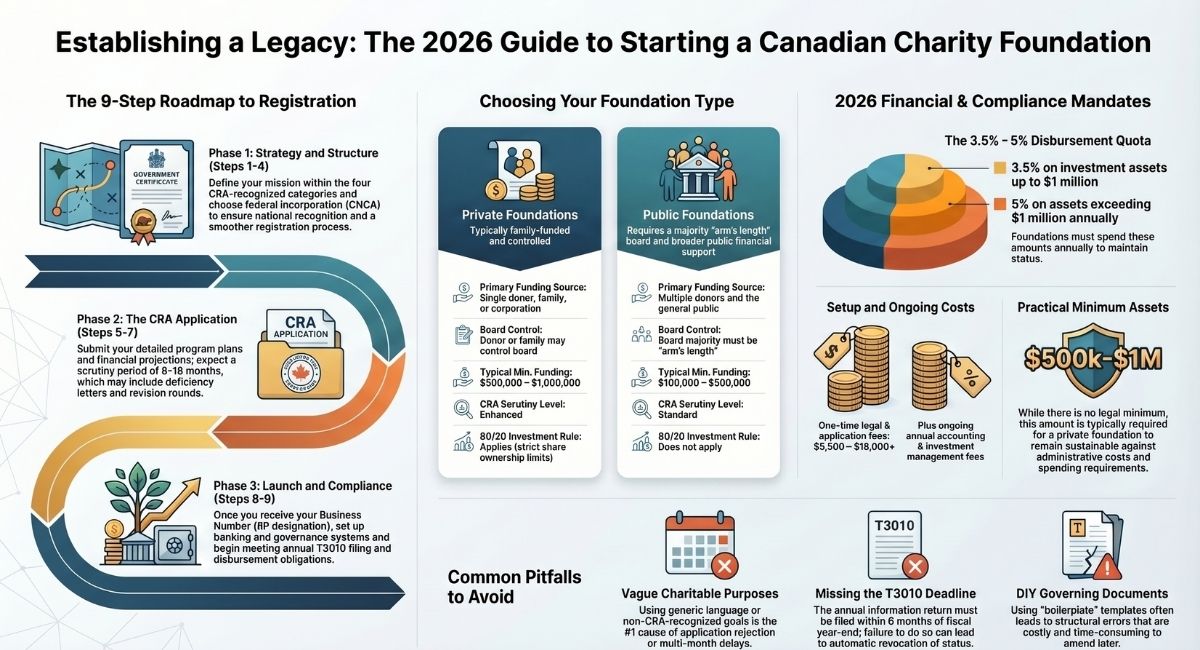

Here is the complete process for establishing a registered charitable foundation in Canada. Following these steps in order — with proper legal guidance at each stage — gives your foundation the best chance of a smooth, timely registration.

Step 1 — Define Your Charitable Mission and Foundation Type

Before any paperwork, determine your charitable purposes and whether a private or public foundation suits your goals. The CRA requires that all charitable purposes fall within one of four recognized categories: relief of poverty, advancement of education, advancement of religion, or other purposes beneficial to the community. Your purposes must be specific, charitable in law, and not merely beneficial to individuals or a private group.

At this stage, also decide whether a foundation is the right structure for you at all, or whether a donor-advised fund, supporting organization, or operating charity might better serve your philanthropic goals.

Step 2 — Choose Federal or Provincial Incorporation

Most foundations incorporate federally under the Canada Not-for-profit Corporations Act (CNCA), which provides the broadest legal recognition and simplifies the CRA registration process. Provincial incorporation is available but may limit your operational scope. Federal incorporation is generally recommended for foundations with national or multi-provincial activities.

Step 3 — Draft Your Articles of Incorporation and Governing Documents

Your Articles of Incorporation must include your charitable purposes, a dissolution clause directing remaining assets to other qualified donees upon wind-up, and a board structure that meets CRA requirements for your foundation type. Your bylaws or operating rules govern how the board meets, votes, and makes decisions.

These documents are scrutinized closely by the CRA during registration. Poorly drafted purposes are the most common reason applications are rejected or significantly delayed. This is where professional legal guidance has the highest impact on your application outcome.

Step 4 — Incorporate Your Foundation

File your Articles of Incorporation with Corporations Canada (federal) or the appropriate provincial registry. You will receive a Certificate of Incorporation confirming your organization's legal existence. This step can typically be completed within a few weeks once your documents are properly finalized.

Step 5 — Apply to the CRA for Registered Charity Status

Submit an Application to Register a Charity to the CRA. This application requires your governing documents, a detailed description of your planned programs and activities, financial projections, board member information, and confirmation of your foundation type (private or public). The CRA reviews foundation applications with enhanced scrutiny due to their regulatory complexity and the significant assets typically involved.

Step 6 — Respond to CRA Queries

The CRA frequently issues deficiency letters requesting clarification or revisions to your application. This is normal and expected. Responding promptly, thoroughly, and accurately is critical — each round of revisions adds approximately 3 to 6 months to your overall timeline. An experienced charity lawyer significantly reduces the likelihood of deficiency letters and improves the quality of your responses when they do occur.

Step 7 — Receive Your Charitable Registration Number

Once the CRA approves your application, it issues a Notice of Registration and a Business Number with an RP designation (for example, 123456789 RP 0001). Your foundation is now a registered charity, legally authorized to issue official donation receipts and operate as a charitable foundation under Canadian law.

Step 8 — Set Up Governance, Banking, and Compliance Systems

Establish your bank accounts, investment accounts, board governance policies, conflict of interest procedures, grant-making criteria, and record-keeping systems. Register for any provincial or territorial requirements that apply to your activities. Build your compliance calendar around your T3010 filing deadline and annual disbursement quota obligations.

Step 9 — Begin Operations and Meet Annual Obligations

Your foundation is now operational. File your T3010 Registered Charity Information Return each year within six months of your fiscal year end. Meet your annual disbursement quota. Maintain proper books and records for all grant-making, receipting, and financial activity. Report any material changes to your purposes, directors, or activities to the CRA.

Private vs Public Foundation: Which to Choose

The first and most important decision you'll make is whether to establish a private foundation or a public foundation. This choice affects everything from governance structure to funding requirements to ongoing obligations.

Understanding Private Foundations

A private foundation is typically controlled by a single donor, family, or small group of related individuals. In Canada, private foundations have these characteristics:

- Usually funded primarily by one source (individual, family, or corporation)

- Board is typically controlled by the donor or donor's family

- More flexibility in grant-making and operational decisions

- Higher regulatory requirements and restrictions

- Subject to stricter rules about business activities and investments

Understanding Public Foundations

Public foundations raise money from multiple sources and serve broader public interests:

- Funded by many donors from the general public

- Board represents diverse community interests, not just donor preferences

- Must maintain arm's length from any single donor or interest group

- More flexibility in business activities and political engagement

- Subject to different (often less restrictive) regulatory requirements

When Private Foundations Make Sense

Choose a private foundation if you:

- Want to maintain control over grant-making decisions

- Plan to fund the foundation primarily with your own assets

- Prefer family involvement in philanthropic decision-making

- Have specific philanthropic interests you want to pursue long-term

- Want to create a lasting family legacy of giving

Many successful business owners and professionals choose private foundations because they provide control and flexibility while creating structured, ongoing charitable impact.

When Public Foundations Are Better

Consider a public foundation if you:

- Want to raise money from multiple donors and sources

- Prefer community input in grant-making decisions

- Need broader public support for your charitable mission

- Want to engage in significant political or advocacy activities

- Plan to operate programs directly rather than just making grants

Hybrid Approaches and Alternatives

Some philanthropists use alternative structures:

- Donor-advised funds through existing public foundations

- Supporting foundations that work with operating charities

- Corporate foundations linked to business operations

- Community foundations that serve specific geographic areas

Making the Strategic Choice

Consider these factors when choosing between private and public foundation structures:

- Control: How much control do you want over ongoing operations?

- Funding: Will you be the primary funder or seek broader support?

- Governance: Do you want family involvement or broader community representation?

- Flexibility: What activities and investments do you want to pursue?

- Legacy: How do you want your philanthropic work to continue after you're gone?

Private vs Public Foundation at a Glance: 2026 Comparison

Foundation Registration Requirements in Canada

Establishing a foundation in Canada involves both incorporation and registration for charitable status, similar to other charities but with additional considerations specific to foundations.

The Two-Step Registration Process

Like other charities, foundations must:

- Incorporate as a nonprofit corporation (federal or provincial)

- Apply for charitable status with the Canada Revenue Agency

However, foundations face additional scrutiny during the registration process because of their unique structure and higher regulatory requirements.

Incorporation Considerations for Foundations

Most foundations choose federal incorporation because:

- Provides consistent legal framework across Canada

- Simplifies charitable status application with CRA

- Offers more flexibility for national or international operations

- Creates clearer regulatory environment for ongoing compliance

Articles of Incorporation for Foundations

Foundation articles of incorporation must include:

- Clear statement of charitable purposes

- Appropriate limitations on business activities

- Proper dissolution clauses directing assets to other qualified donees

- Board structure that meets CRA requirements for foundation type

Charitable Purposes for Foundations

Foundation purposes must fit within the four categories of charitable purposes:

- Relief of poverty

- Advancement of education

- Advancement of religion

- Other purposes beneficial to the community

Foundation purposes should be broad enough to allow flexibility in grant-making while specific enough to provide clear direction for operations.

Enhanced CRA Review for Foundations

The CRA subjects foundation applications to enhanced review because:

- Foundations often involve significant assets

- Complex governance and funding arrangements require careful assessment

- Higher risk of non-compliance due to regulatory complexity

- Greater potential impact if problems develop

Timeline Expectations for Foundation Registration

Foundation registration typically takes longer than other charity types:

- Simple foundations: 8-12 months from application submission

- Complex foundations: 12-18 months or longer

- Applications requiring revisions: Add 3-6 months per revision round

Working with experienced professionals significantly improves approval timelines and success rates.

Minimum Funding Requirements for Foundations

While Canada doesn't legally require minimum funding levels for foundation registration, practical considerations make adequate initial funding essential for successful operations.

No Legal Minimum, But Practical Requirements

The CRA doesn't specify minimum funding amounts for foundation registration, but expects foundations to demonstrate:

- Adequate resources to carry out stated charitable purposes

- Realistic financial projections for ongoing operations

- Sufficient assets to meet disbursement quota requirements

- Proper financial management and oversight capabilities

Practical Minimum Funding Levels

Based on experience with successful foundations, consider these practical minimums:

Private foundations: $500,000 to $1 million minimum

- Provides sufficient income for meaningful grant-making

- Covers administrative costs and professional services

- Meets disbursement quota requirements sustainably

- Demonstrates serious commitment to charitable work

Public foundations: $100,000 to $500,000 initial funding

- Sufficient to begin operations while building broader support

- Demonstrates viability to potential donors and funders

- Covers startup costs and initial program development

- Provides foundation for ongoing fundraising efforts

Factors Affecting Required Funding Levels

Geographic scope: National or international foundations need more funding than local foundations

Grant-making approach: Foundations making many small grants need more administrative capacity than those making fewer large grants

Operating model: Foundations that operate programs directly need more funding than pure grant-making foundations

Professional support: Foundations requiring significant legal, accounting, or investment management need larger asset bases

Funding Structure Considerations

Initial endowment: Many foundations start with a significant initial contribution that provides ongoing income

Ongoing contributions: Some foundations rely on regular contributions from founders or ongoing fundraising

Mixed approach: Combination of initial endowment and ongoing support provides flexibility and sustainability

How Much Does It Cost to Start a Charitable Foundation in Canada?

Understanding the real cost of starting a foundation helps you plan appropriately and avoid surprises. There is no single fixed cost — expenses vary based on foundation complexity, asset size, geographic scope, and the level of professional support you engage. Here is a realistic overview for 2026.

One-Time Setup Costs

Legal fees for incorporation and governing documents: $2,500–$8,000 or more, depending on complexity and whether revisions are required during the drafting process.

CRA application preparation with professional assistance: $3,000–$10,000 or more. This is one of the highest-value investments you can make in your foundation's future — a well-prepared application reduces the likelihood of deficiency letters, revisions, and delays.

Federal incorporation filing fee: Approximately $200 when filed online through Corporations Canada.

Professional consultation and pre-application planning: Varies. Some founders invest in early strategic advice before committing to a specific structure, which often saves money by avoiding structural mistakes that are costly to correct later.

Ongoing Annual Costs

Legal and compliance advice: Varies based on foundation activity, complexity, and whether issues arise. Most foundations budget for at least some annual legal support.

Accounting and T3010 preparation: $1,500–$5,000 or more annually, depending on the volume and complexity of your foundation's financial activity.

Investment management fees: Typically 0.5%–1.5% of assets under management annually. For a $1 million foundation, this is $5,000–$15,000 per year.

Administrative and operational costs: Varies significantly by size. Small foundations may operate with minimal overhead; larger foundations may require dedicated staff.

The Cost of Not Getting It Right

Attempting to register a foundation without professional guidance often results in multiple rounds of CRA revisions, extended timelines, and structural problems that are expensive to correct after registration. Many founders who initially attempted self-registration ultimately engage professional help anyway — at a higher total cost than if they had done so from the start.

Foundation Governance and Board Structure

Effective governance is crucial for foundation success and regulatory compliance. The structure you establish at the beginning shapes operations for the life of your foundation.

Board Composition Requirements

All Canadian foundations must have boards that meet legal requirements:

- Minimum three directors (federal incorporation)

- Majority Canadian residents for federal corporations

- Arm's length directors for public foundations

- Independent oversight even in private foundations

Private Foundation Governance

Private foundations can have boards controlled by donors and families, but still need:

- At least some independent directors for oversight

- Clear conflict of interest policies and procedures

- Proper decision-making processes and documentation

- Regular board meetings and strategic planning

Public Foundation Governance

Public foundations must maintain arm's length from any single donor:

- Board majority must be independent from any donor

- No single donor can control foundation decisions

- Diverse representation from community and stakeholder groups

- Transparent governance processes and public accountability

Board Roles and Responsibilities

Foundation boards have significant legal and practical responsibilities:

- Fiduciary duties to act in the foundation's best interests

- Strategic oversight of foundation direction and priorities

- Financial oversight of investments, spending, and grant-making

- Compliance monitoring to ensure regulatory requirements are met

- Risk management to protect foundation assets and reputation

Essential Governance Policies

Every foundation needs comprehensive governance policies covering:

- Conflict of interest identification and management

- Grant-making criteria and decision-making processes

- Investment management and oversight

- Financial controls and expense management

- Board recruitment, orientation, and evaluation

Understanding proper governance becomes especially important when preparing annual T3010 filings that require detailed reporting about board composition and decision-making processes.

Tax Benefits of Canadian Charitable Foundations

Foundations enjoy significant tax advantages that enable them to maximize their charitable impact, but these benefits come with corresponding obligations and restrictions.

Income Tax Exemption

Registered charitable foundations are exempt from income tax on:

- Investment income from foundation assets

- Capital gains from asset appreciation

- Donations received from individuals and corporations

- Income from charitable activities

This exemption allows foundations to accumulate and invest assets for long-term charitable impact.

Donation Tax Benefits for Contributors

Individuals and corporations donating to foundations receive significant tax benefits:

Individual donors:

- Federal charitable tax credit up to 33% of donation

- Provincial credits varying by province

- Enhanced first-time donor credits in some provinces

- Ability to carry forward unused credits for five years

Corporate donors:

- Deduction against corporate income up to 75% of net income

- Carry forward of unused deductions for five years

- Enhanced deductions for certain types of charitable gifts

Capital Gains Tax Relief

Special tax benefits apply to certain types of gifts to foundations:

- Elimination of capital gains tax on gifts of publicly traded securities

- Reduced capital gains inclusion rates for gifts of private company shares

- Special rules for ecological gifts and cultural property

Estate Planning Benefits

Foundations provide significant estate planning advantages:

- Unlimited charitable deduction for bequests to foundations

- Reduction of estate taxes through charitable giving

- Ability to create lasting family legacy while reducing tax burden

- Flexibility in timing and structure of testamentary gifts

Tax Compliance Obligations

Foundation tax benefits come with corresponding obligations:

- Annual T3010 filing requirements with detailed activity reporting

- Compliance with disbursement quota requirements

- Restrictions on business activities and political involvement

- Proper receipting procedures for all donations received

Foundation Disbursement Quota Requirements

Canadian foundations must spend a minimum percentage of their assets annually on charitable activities, known as the disbursement quota. Understanding these requirements is crucial for foundation planning and operations.

What is the Disbursement Quota?

The disbursement quota is the minimum amount a foundation must spend annually on charitable activities, calculated as a percentage of the average value of investment assets not used directly in charitable programs.

Current Disbursement Quota Rates

As of 2026, the CRA applies the following disbursement quota rates to registered charitable foundations:

- 3.5% of investment assets for the portion not exceeding $1 million

- 5% of investment assets for the portion exceeding $1 million

These rates have been in effect since the 2023 federal budget amendments to the Income Tax Act, which increased the quota for larger asset pools from the previous flat 3.5% rate. Foundations established or actively operating in 2026 must plan their investment strategies, grant-making calendars, and cash flow management around these thresholds from day one.

What Counts Toward Disbursement Quota

Qualifying disbursements include:

- Grants to qualified donees (other registered charities)

- Direct charitable program expenses

- Reasonable administrative costs related to charitable activities

- Certain fundraising expenses for public foundations

What Doesn't Count

Non-qualifying expenditures include:

- Investment management fees

- Excessive administrative expenses

- Political activities beyond legal limits

- Activities that don't directly further charitable purposes

Strategic Implications of Disbursement Quota

The disbursement quota affects foundation strategy:

- Minimum spending requirements ensure foundations actively distribute charitable benefits

- Investment strategy must balance growth with liquidity needs for quota compliance

- Grant-making timing requires planning to meet annual quota requirements

- Reserve management influences how foundations manage surplus funds

Compliance and Penalties

Failure to meet disbursement quota requirements can result in:

- Monetary penalties equal to the shortfall amount

- Requirements to make up missed disbursements in subsequent years

- Enhanced CRA scrutiny and compliance oversight

- Potential revocation of charitable status for chronic non-compliance

Understanding disbursement quota requirements is essential when developing foundation investment strategies and ensuring proper insurance protection for foundation assets and operations.

Investment Rules for Charitable Foundations

Canadian foundations face specific restrictions on their investment activities and business operations that don't apply to other types of charities.

Prohibited Business Activities

Foundations cannot carry on business activities, with limited exceptions:

- Related businesses directly connected to charitable purposes may be permitted

- Passive investments in business entities are generally allowed

- Investment management activities are considered administrative rather than business

The 80/20 Rule for Private Foundations

Private foundations face additional restrictions:

- Cannot own more than 20% of any class of shares in a corporation

- Must consider holdings of non-arm's length parties in calculating ownership

- Must dispose of excess holdings within specific timeframes

- Face penalties for violating ownership restrictions

Investment Management Considerations

Foundations should develop investment policies that address:

- Asset allocation appropriate for long-term charitable objectives

- Risk management to protect foundation capital

- Liquidity needs for disbursement quota compliance

- Professional investment management oversight

Prohibited Investments

Foundations cannot invest in:

- Non-qualifying investments such as resource properties or debt obligations to non-arm's length parties

- Investments that violate the 80/20 rule for private foundations

- Speculative investments inappropriate for charitable assets

Professional Investment Management

Most foundations benefit from professional investment management:

- Expertise in foundation investment requirements and restrictions

- Ongoing compliance monitoring and reporting

- Asset allocation strategies appropriate for charitable objectives

- Integration with disbursement quota planning and cash flow needs

Foundation vs Operating Charity: Key Differences

Understanding the differences between foundations and operating charities helps you choose the right structure for your philanthropic goals.

Primary Function Differences

Foundations primarily:

- Make grants to other charitable organizations

- Maintain endowments for long-term charitable impact

- Focus on funding rather than direct service delivery

- Operate with relatively small staff focused on grant-making

Operating charities primarily:

- Deliver direct services to beneficiaries

- Focus on program operation rather than grant-making

- Maintain larger staffs involved in service delivery

- Raise funds to support their own program operations

Regulatory Differences

Foundations face stricter rules about:

- Business activities and investments

- Disbursement quota requirements

- Related party transactions

- Board composition and governance

Operating charities have more flexibility in:

- Business activities related to their charitable purposes

- Investment strategies and asset management

- Political activities and advocacy work

- Fundraising methods and approaches

Operational Considerations

Foundation advantages:

- Can create lasting impact through endowment funding

- Leverage expertise of other organizations through grants

- Lower operational complexity and staffing requirements

- Ability to support diverse charitable causes and organizations

Operating charity advantages:

- Direct connection to beneficiaries and charitable impact

- More flexibility in activities and operations

- Easier to demonstrate charitable impact for donors and funders

- Greater opportunity for innovation in service delivery

Strategic Decision Factors

Choose a foundation if you:

- Want to support multiple charitable causes through grants

- Prefer to leverage existing expertise rather than building programs

- Have significant assets to endow for long-term impact

- Want to focus on philanthropic strategy rather than service delivery

Choose an operating charity if you:

- Want to deliver services directly to beneficiaries

- Have expertise in specific charitable activities or populations

- Prefer hands-on involvement in charitable work

- Want maximum flexibility in operations and activities

Common Mistakes When Starting a Foundation in Canada

These are the most frequent — and most costly — mistakes founders make during the registration and early operation phases. Knowing them in advance helps you avoid the delays and legal complications that derail otherwise well-intentioned philanthropic plans.

Poorly drafted charitable purposes. Vague, overly broad, or legally insufficient purposes are the leading cause of CRA deficiency letters and application rejections. Purposes must be specific, charitable in law, and drafted using language the CRA recognizes and accepts. Generic statements of intent do not meet this standard.

Underestimating the registration timeline. Many founders assume registration takes a few months and are caught off guard by a process that routinely runs 8 to 18 months. Planning your donor communications, grant commitments, and operations around an unrealistic timeline creates pressure and reputational risk.

Insufficient initial funding. Starting a foundation without adequate assets creates compliance problems from the moment you are registered. If your asset base cannot sustainably generate enough disbursable income to meet your annual quota while covering administrative costs, your foundation faces difficulties from year one.

Confusing private and public foundation rules. The regulatory requirements for private and public foundations are meaningfully different. Operating a private foundation as though it were an operating charity — or failing to understand the 80/20 share ownership rule — leads to violations that are difficult and expensive to correct after the fact.

Using DIY or boilerplate governing documents. Generic articles of incorporation downloaded from the internet routinely fail CRA scrutiny. Governing documents for charitable foundations must be specifically drafted to meet registration requirements. Errors in your articles or bylaws can require formal amendments — a time-consuming and costly process.

Missing T3010 filing deadlines. Your annual T3010 Registered Charity Information Return must be filed within six months of your fiscal year end, every year. Missing this deadline triggers penalties and, with repeated non-compliance, can result in revocation of your charitable status.

Failing to report changes to the CRA. Changes to your foundation's purposes, key activities, directors, or structure must be reported to the CRA. Many foundations assume that post-registration changes are an internal matter — they are not. Unreported changes can be discovered during audits and result in compliance action.

Conclusion

Starting a charitable foundation is a significant undertaking that requires careful planning, adequate funding, and ongoing professional support. Whether you're interested in sponsorship arrangements or comprehensive insurance protection, foundations must maintain compliance with complex regulatory requirements while pursuing their charitable missions.

The key to successful foundation establishment is understanding the legal requirements, planning for adequate funding and governance, and building systems that support long-term sustainability and impact. Professional guidance during the planning and registration phases helps ensure your foundation achieves its philanthropic goals while maintaining full compliance with Canadian charity law.

B.I.G. Charity Law Group provides comprehensive legal services for foundation establishment, from initial planning through registration and ongoing compliance support. Experienced professional guidance helps ensure your foundation creates the lasting charitable impact you envision while meeting all legal requirements.

Ready to establish a charitable foundation that creates lasting impact while maintaining full legal compliance? Work with experienced professionals who understand the complexities of foundation law and can guide you through every step of the process.

Frequently Asked Questions

How long does it take to register a charitable foundation in Canada?

The CRA typically takes 8 to 18 months to process a foundation registration application. Simple applications with well-drafted governing documents and no deficiency letters are processed closer to the 8-month end. Complex foundations, or those that require multiple rounds of revisions, can exceed 18 months. Working with an experienced charity lawyer from the beginning reduces delays significantly by reducing the likelihood of deficiency letters in the first place.

What is the difference between a charity and a foundation in Canada?

In Canada, a foundation is a specific type of registered charity. All foundations are charities, but not all charities are foundations. Foundations are classified as either private or public foundations depending on their funding sources and board structure, and they are subject to stricter investment and disbursement rules than most other registered charities. The key operational difference is that foundations primarily make grants to other charities or maintain endowments, while operating charities deliver programs and services directly to beneficiaries.

Does starting a foundation in Canada require a lawyer?

Working with a charity lawyer is not legally required, but it is strongly recommended. The CRA's registration process for foundations is complex, and the most common cause of delays and rejections is governing documents that do not meet legal requirements. Professional guidance also ensures that your foundation's structure, purposes, and policies comply with the Income Tax Act from the outset — avoiding structural problems that are expensive to fix after registration is complete.

Can a family control a foundation in Canada?

Yes. Private foundations can be controlled by a donor and their family. Family members may make up the majority of the board and be involved in grant-making decisions. However, even privately controlled foundations must have conflict of interest policies, proper governance procedures, and must comply with the Income Tax Act's rules governing self-dealing and related party transactions. The CRA monitors private foundations closely for compliance with these requirements.

What is the disbursement quota for foundations in Canada in 2026?

As of 2026, Canadian charitable foundations must disburse at least 3.5% of investment assets annually on the portion of assets up to $1 million, and 5% on the portion exceeding $1 million. These amounts must be spent on charitable activities, grants to other registered charities, or qualifying administrative expenses directly related to charitable work. Failure to meet the disbursement quota can result in monetary penalties from the CRA.

Can a foundation in Canada give money directly to individuals?

Generally, foundations cannot make grants directly to individuals. Disbursements must go to qualified donees — primarily other registered charities — or be used to fund the foundation's own direct charitable activities. There are limited exceptions, but these require careful legal structuring and must be consistent with the foundation's registered purposes. Distributing money to individuals outside these exceptions creates serious compliance risk.

How much money do you need to start a foundation in Canada?

There is no legally prescribed minimum, but practical experience strongly suggests that private foundations should have at least $500,000 to $1 million in initial assets, while public foundations can begin with $100,000 to $500,000 while actively building broader donor support. Foundations with insufficient assets often struggle to meet annual disbursement quota requirements while covering the administrative, legal, and accounting costs of ongoing compliance.

What happens if a foundation fails to meet its disbursement quota?

Failing to meet the disbursement quota in a given year results in monetary penalties equal to 60% of the shortfall amount. The CRA can also require that the shortfall be made up in a subsequent year. Chronic non-compliance with disbursement quota requirements is grounds for enhanced CRA scrutiny and, in serious cases, revocation of charitable status. Foundations should plan their investment and spending strategies proactively to ensure quota compliance every year.

What is the 80/20 rule for private foundations in Canada?

The 80/20 rule is an investment restriction that applies specifically to private foundations. It prohibits a private foundation from owning more than 20% of any class of shares in a corporation, taking into account the holdings of all persons not dealing at arm's length with the foundation. Holdings that exceed this threshold must be reduced within prescribed timeframes. Violations can result in significant financial penalties. This rule does not apply to public foundations.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)