How Much of a Charity's Budget Should Go to Overhead?

Published on

October 8, 2021

Last updated on

February 12, 2026

Overhead is the term used for expenses of a charity that are not the cost of an actual program or charitable activity. The overhead costs generally fall under the categories of administration, management, and fundraising.

As of 2026, the conversation around charity overhead continues to evolve. CRA compliance expectations remain focused on transparency and reasonable allocation rather than arbitrary percentage limits. Understanding what constitutes reasonable overhead is essential for both charity leaders managing budgets and donors evaluating where to give. In Canada, the CRA monitors these expenses through annual T3010 reporting, but focusing solely on overhead percentages can be misleading.

Quick Answer: Recommended Overhead Percentages for Canadian Charities

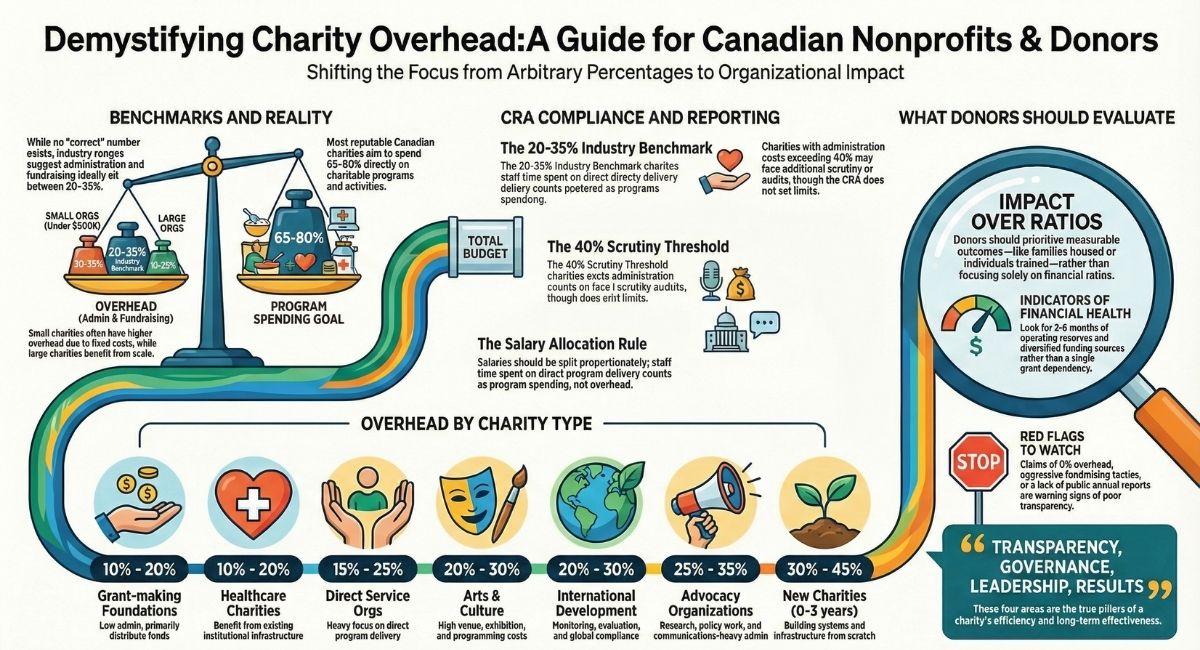

There is no universal "correct" overhead percentage for charities in Canada. The CRA does not mandate a specific overhead ratio. However, generally accepted benchmarks suggest:

Industry-accepted ranges:

- Administration and fundraising combined: 20-35% of total budget

- Program spending: 65-80% of total budget

- Small charities (under $500,000 revenue): May have higher overhead (30-40%)

- Large established charities: Often maintain lower overhead (15-25%)

The focus should be on effectiveness and impact, not just overhead percentages. Context matters significantly based on your charity's age, size, sector, and operational model.

What Are Typical Overhead Costs for a Not-for-Profit and Charity?

Some examples of expenses included in the overhead category:

- Office space

- Utilities

- Supplies and equipment

- Salaries

- Employee compensation

- Legal services and accounting fees

- Website

- Fundraising events

- Insurance

- Corporate governance

- Security

How Does the CRA Track Charity Overhead?

Canadian registered charities must report their expenses on Form T3010 (Registered Charity Information Return) in specific categories:

Required expense reporting:

- Line 4800: Charitable programs

- Line 4810: Management and administration

- Line 4920: Fundraising

- Line 5000: Political activities (if applicable)

The CRA reviews these ratios during compliance audits but does not impose a specific overhead limit. However, charities with unusually high administration costs (above 40%) may face additional scrutiny and should be prepared to justify these expenses.

What the CRA considers reasonable:

- Salaries proportionate to charity size and sector

- Professional fees (legal, accounting) necessary for compliance

- Technology and systems essential for program delivery

- Fundraising costs that generate sufficient return on investment

- Board governance expenses required under corporate law

Proper expense allocation is critical. Many charities make the mistake of lumping all staff salaries into overhead when program delivery staff should be counted under charitable programs. This can artificially inflate your overhead ratio and create misleading financial reports.

Typical Overhead by Charity Type in Canada

Different types of charities naturally have different overhead structures. Here's what's typical across Canadian charity sectors:

Source: Analysis of publicly available T3010 data and sector benchmarks (2024-2025)

Understanding where your charity fits within these ranges helps set realistic expectations and communicate effectively with donors.

The US Better Business Bureau recommends charities spend no more than 35% on administration and fundraising. However, this number is not set in stone. This percentage may seem reasonable for some charities that have the ability to keep their overhead at 10-15% of their funding, but many others are bound to have higher overhead costs, closer to 20-35%. In Canada, Imagine Canada and the CRA provide guidance through the Standards Program and T3010 reporting requirements. Canadian charity watchdog organizations typically use the 20-35% overhead threshold as a general guideline, though sector and organizational factors create significant variation.

Many people have an expectation that overhead be substantially lower than 35%. Studies have shown that donors perceive charities with high overhead rates as less effective in their work. Understandably, donors want to support a cause, not enrich the nonprofit director. However, it's unfair to judge a charity based solely on overhead costs. These financial ratios do not reflect the true impact of the organization. Charities do not need low overhead, they need to demonstrate high performance.

Does Overhead Reflect the Effectiveness of a Charity?

Overhead percentage isn't the only thing to consider when evaluating a charity's performance. There are many different reasons why one charity might seem better than another. Some charities have a direct mission, while others are parent organizations or foundations and don't do any of the work themselves. Furthermore, many charities do not report their overhead costs accurately either because they do not properly understand the differentiation between administration and charitable activities or they simply want to skew their ratio to attract donors. All these factors can affect the percentage of overhead, and therefore overhead costs will vary significantly between charities.

Focusing on one piece of a charity's performance can be harmful. It is crucial to consider all aspects of a charity's financial and organizational performance, because it is only through this comprehensive evaluation that the true value of an organization can be ascertained. Under-investing in critical areas can cause unintended consequences that lead to compromised quality or sustainability. As a result, the overhead ratio is not an accurate measure of how well a nonprofit is performing.

In fact, many charities could spend more money on overhead. The money goes to investments for the charity's future, such as training, planning, evaluation, and internal systems — and also to raise more money. This will allow the charity to get better at their work and sustain themselves.

Although overhead costs do not provide an easy way to measure charity accountability, they are necessary for the charity to function properly. Achieving transparency about overhead costs can be costly and time-consuming, but it's worth it for charities to do so because these costs are necessary for them to function well.

What Donors Should Know When Evaluating Charities

Instead of focusing solely on overhead ratios, donors should consider these factors when deciding where to give:

Financial health indicators:

- Revenue trends over 3-5 years (growing, stable, or declining?)

- Reserve fund adequacy (3-6 months operating expenses is recommended)

- Diversification of funding sources (not relying on a single donor or grant)

- Debt-to-asset ratio and overall financial stability

- Whether the charity files its T3010 on time each year

Impact and effectiveness measures:

- Clear, measurable outcomes reported (not just activities or outputs)

- Third-party evaluations or impact assessments

- Beneficiary testimonials and case studies showing real change

- Progress toward stated goals year over year

- Evidence of program adaptation based on results

Transparency and accountability:

- Annual reports publicly available and easy to find

- Form T3010 filed on time and complete (check the CRA charities database)

- Board composition and governance policies disclosed

- Clear explanation of how donated funds are tracked and allocated

- Willingness to answer donor questions about finances and impact

Red flags to watch for:

- Overhead claims that seem too good to be true (less than 5%)

- Reluctance to provide financial information when asked

- Aggressive or manipulative fundraising tactics

- Frequent board or leadership turnover without explanation

- CRA compliance issues, penalties, or revocation notices

- Significant unexplained changes in program spending year over year

A charity with 30% overhead that achieves significant, measurable impact is far more valuable than a charity with 10% overhead that accomplishes little. The percentage tells you about resource allocation, but not about results.

A charity's efficiency and effectiveness can be measured by focusing on the following four areas:

- Transparency

- Governance

- Leadership

- Results

For more information on how low overhead can limit nonprofit effectiveness, read this article in the Stanford Social Innovation Review as well as this study from the Urban Institute.

How Charity Leaders Can Manage and Communicate Overhead

If you're leading a charity, here's how to handle overhead strategically and communicate effectively with your donors and the CRA.

Calculate your overhead accurately:

- Review your chart of accounts allocation between program, administration, and fundraising

- Ensure salaries are split proportionately based on actual time spent in each area

- Allocate shared costs (rent, utilities, IT) using a reasonable and documented methodology

- Document your allocation decisions for CRA audit purposes

- Review allocations annually as your organization evolves

Getting your allocations right isn't just about compliance. It's about understanding your true costs and making informed decisions about where to invest.

Benchmark against similar organizations:

- Compare your ratios to charities of similar size in your sector using T3010 data

- Use the CRA's publicly available charities database to find comparable organizations

- Consider geographic and operational differences that affect costs

- Look at trends over time, not just single-year snapshots

- Join sector associations that provide benchmarking data to members

Communicate effectively with donors:

Don't hide from overhead conversations. Instead, frame them constructively:

- Explain what your overhead enables: "Our investment in financial systems ensures every dollar is tracked and used effectively"

- Share specific examples: "Our $50,000 investment in donor management software helped us reduce processing time by 60% and increase donor retention by 25%"

- Provide context: "As a charity founded in 2023, our overhead is higher while we build the infrastructure needed for long-term impact"

- Report outcomes, not just percentages: "Our 75% program spending delivered housing for 450 families and job training for 200 individuals"

- Be honest about challenges: "We're working to reduce overhead as we grow, but we won't sacrifice quality or compliance to hit an arbitrary number"

Invest strategically in capacity:

Smart overhead spending creates leverage for greater impact:

- Staff development and training that improves program quality

- Technology and systems that increase efficiency

- Strategic planning and program evaluation

- Fundraising infrastructure that generates positive return on investment

- Compliance support that protects charitable status

- Quality assurance and impact measurement

The goal isn't to minimize overhead at all costs. The goal is to invest wisely in both programs and the organizational capacity needed to deliver those programs effectively and sustainably.

Frequently Asked Questions About Charity Overhead

What percentage of donations should go directly to the cause?

Most reputable Canadian charities spend 65-80% of their budget on charitable programs. However, this varies by charity type, size, and operational model. New charities may spend less on programs initially while building capacity. Grant-making foundations may have lower overhead (80-90% going to programs) because they distribute funds rather than deliver services directly.

How can I find out a charity's overhead costs?

Search the charity's business number or name on the CRA's list of charities at canada.ca/charities-listings. Their Form T3010 shows the breakdown between charitable programs (line 4800), management and administration (line 4810), and fundraising (line 4920). You can view T3010 returns for the current year and several previous years to see trends.

Do overhead costs include staff salaries?

Yes, but salaries should be allocated across categories based on what staff actually do. Program staff salaries count as program expenses. Administrative staff and portions of executive director time spent on general management fall under administration (overhead). Fundraising staff salaries are fundraising expenses. Many charities make errors by putting all salaries in overhead.

Can a charity spend too little on overhead?

Yes. Under-investing in administration can harm long-term sustainability. Charities need adequate systems, staff training, technology, governance, and financial management to deliver programs effectively. The "nonprofit starvation cycle" occurs when charities cut overhead so much that they can't build capacity, leading to poor outcomes and eventual organizational failure.

What is considered management and administration for CRA purposes?

Management and administration includes corporate governance, general management, financial management and reporting, human resources, office administration, information technology, and other central services not directly related to programs or fundraising. The CRA provides detailed guidance in the T3010 instructions.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)