Can Not-for-Profit Corporations Waive Audit and Review Engagements?

Published on

January 25, 2024

Last updated on

February 1, 2026

Ontario nonprofits often ask whether they can skip costly audit and review engagements. Under the Ontario Not-for-Profit Corporations Act (ONCA), the answer depends on your annual revenue and corporation type. Most nonprofits can waive these requirements if they follow specific procedures.

The ability to waive audit or review engagements can save your organization thousands of dollars annually. However, the rules vary significantly based on whether you're classified as a public benefit corporation and your organization's revenue level. Understanding these requirements ensures your nonprofit remains compliant while managing costs effectively.

ONCA Audit and Review Requirements at a Glance

Here's a quick reference showing when your nonprofit can waive financial examination requirements:

Note: These thresholds may change through future regulation amendments. Always verify current requirements before making decisions.

Understanding ONCA Audit Requirements

The Ontario Not-for-Profit Corporations Act outlines specific rules for audit and review engagements that nonprofits must follow. These requirements ensure financial accountability and transparency while recognizing that smaller organizations may not need the same level of scrutiny as larger ones.

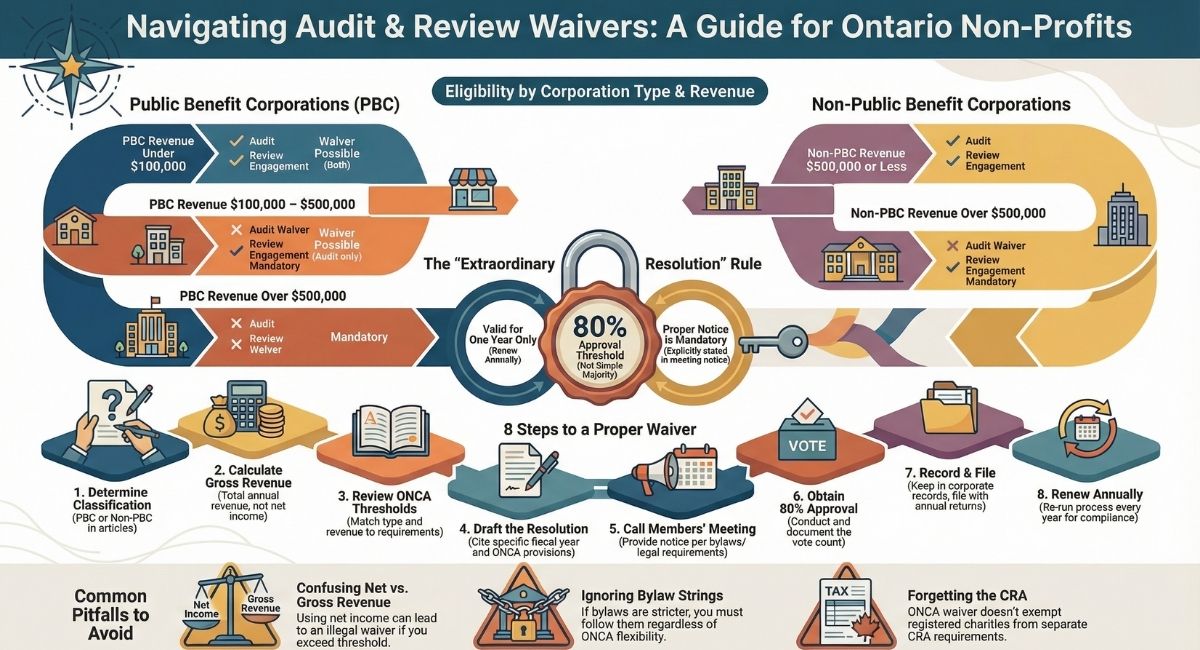

Public Benefit Corporations

If your organization is classified as a public benefit corporation under section 76 of ONCA, your audit and review requirements depend on your annual revenue:

Annual Revenue Under $100,000: Your organization can waive both audit and review engagement requirements. This provides significant cost savings for smaller nonprofits operating on limited budgets.

Annual Revenue Between $100,000 and $500,000: You can waive the audit requirement, but a review engagement remains mandatory. A review engagement provides reasonable assurance about your financial statements without the extensive testing required in a full audit.

Annual Revenue Over $500,000: An audit becomes mandatory and cannot be waived. This ensures larger organizations maintain the highest level of financial scrutiny and public accountability.

Non-Public Benefit Corporations

For nonprofits not classified as public benefit corporations, the requirements differ:

Annual Revenue of $500,000 or Less: Both audit and review engagement requirements can be waived completely. This gives smaller non-public benefit corporations maximum flexibility in managing their financial reporting costs.

Annual Revenue Over $500,000: You can waive the audit requirement, but must conduct a review engagement. This balances cost considerations with the need for financial oversight.

The Extraordinary Resolution Requirement

Regardless of your corporation type or revenue level, waiving audit or review requirements requires an extraordinary resolution. This means at least 80% of your voting members must approve the decision at a properly called meeting.

Key points about extraordinary resolutions:

- They require 80% member approval, not just a simple majority

- The resolution is valid only until your next annual meeting of members

- You must renew the waiver annually if you wish to continue without audits or reviews

- Proper meeting notice must be given to all members

- The resolution should be documented in your corporate records

Failing to obtain the proper level of approval or follow correct procedures can result in legal and financial consequences, including loss of good standing with the Ontario government.

How to Properly Waive Your Audit or Review Engagement

Follow these steps to ensure compliance when waiving financial examination requirements:

Step 1: Determine Your Corporation Classification

Confirm whether your nonprofit is a public benefit corporation or non-public benefit corporation under ONCA. If you're unsure, consult your articles of incorporation or speak with a charity lawyer.

Step 2: Calculate Your Annual Revenue Accurately

Review your financial statements to determine your precise annual revenue. Include all revenue sources to ensure you're using the correct threshold category.

Step 3: Review ONCA Requirements

Match your corporation type and revenue level to the requirements table above to confirm what you can waive.

Step 4: Draft an Extraordinary Resolution

Prepare a clear resolution stating your intention to waive the audit, review engagement, or both. Include the specific fiscal year and cite the appropriate ONCA provisions.

Step 5: Call a Proper Members' Meeting

Provide adequate notice to all members according to your bylaws and ONCA requirements. The notice should clearly state that an extraordinary resolution will be considered.

Step 6: Obtain 80% Member Approval

Hold the vote and ensure at least 80% of voting members approve the resolution. Document the vote count carefully.

Step 7: Record and File the Resolution

Keep the resolution in your corporate records. Some organizations also file it with their annual returns for additional documentation.

Step 8: Renew Annually

Remember that the waiver expires at your next annual meeting. Plan to repeat this process each year if you wish to continue without audits or reviews.

Need help navigating this process? Our ONCA compliance services can guide you through every step.

Common Mistakes When Waiving Audit Requirements

Many Ontario nonprofits make errors when attempting to waive financial examination requirements. Avoid these common pitfalls:

Failing to Achieve 80% Approval: Some organizations assume a simple majority (50% + 1) is sufficient. ONCA specifically requires an extraordinary resolution with 80% approval. Anything less makes the waiver invalid.

Not Documenting the Resolution Properly: Verbal agreements or informal decisions don't count. You must have a written resolution passed at a properly constituted members' meeting with accurate minutes.

Assuming the Waiver Continues Indefinitely: The waiver only lasts until your next annual meeting. If you don't renew it, you'll be required to conduct the audit or review for that fiscal year.

Miscalculating Revenue Thresholds: Some nonprofits use net income instead of total revenue, or exclude certain revenue sources. Use your gross annual revenue from all sources when determining which category you fall into.

Confusing Corporation Types: Public benefit and non-public benefit corporations have different thresholds. Verify your classification before proceeding.

Ignoring Bylaw Requirements: Some nonprofit bylaws contain more stringent requirements than ONCA. Always check your bylaws don't require audits regardless of ONCA provisions.

2026 Compliance Reminders

As of 2026, all Ontario nonprofits should have completed their ONCA transition (the deadline was October 18, 2024). If your organization hasn't transitioned yet, you risk dissolution and loss of corporate status.

Current compliance considerations:

- Verify your bylaws comply with ONCA requirements for extraordinary resolutions

- Review whether your articles correctly identify your corporation as public benefit or non-public benefit

- Confirm your annual revenue calculations align with current accounting standards

- Check if any ONCA regulations have been amended since your last review

- Ensure your annual filings with the Ontario government remain current

If you're unsure about your compliance status, our team can conduct a comprehensive ONCA compliance review for your organization.

Ensuring Proper Financial Oversight

Not-for-profit corporations must carefully consider their annual revenue and legal classification when deciding whether to waive audit and review engagement requirements. While cost savings can be significant, following proper procedures is essential to maintain compliance and organizational credibility.

By understanding ONCA requirements, obtaining appropriate member approval, and documenting decisions properly, nonprofits can make informed choices about their financial examination needs. This approach ensures accountability and transparency while managing resources effectively.

If you're uncertain about your organization's requirements or need assistance with the waiver process, professional guidance can prevent costly mistakes and ensure full compliance with Ontario law.

Need help with ONCA compliance or audit waiver decisions? Book a consultation with our charity law team to discuss your organization's specific situation.

Frequently Asked Questions

Can my Ontario nonprofit completely avoid financial reviews?

Yes, if you're a public benefit corporation earning under $100,000 annually, or a non-public benefit corporation earning under $500,000 annually. In both cases, you can waive both audit and review requirements with an 80% member vote through an extraordinary resolution.

What's the difference between waiving an audit versus a review engagement?

An audit is a comprehensive examination of your financial statements involving extensive testing and verification. A review engagement is less detailed, providing only limited assurance. Organizations with moderate revenue often must keep the review even if they can waive the full audit.

How long does an extraordinary resolution to waive audits last?

Only until your next annual meeting of members. You must renew the waiver annually if you want to continue without financial examinations. The resolution doesn't carry forward automatically.

What happens if we waive our audit requirement incorrectly?

Your corporation could face penalties including loss of good standing with the Ontario government, regulatory sanctions, or legal challenges from members. You may also need to conduct retroactive audits or reviews at significant cost.

Do federal charities follow the same audit waiver rules?

No. Federal nonprofit corporations follow the Canada Not-for-profit Corporations Act, which has different requirements. These rules apply only to Ontario-incorporated nonprofits under ONCA.

Can individual members object to waiving the audit?

While members can vote against the resolution, if 80% approve, the minority cannot prevent it. However, if proper procedures aren't followed, members may have grounds to challenge the decision.

Does the CRA require audits even if ONCA doesn't?

The Canada Revenue Agency has separate requirements for registered charities. Even if you waive ONCA requirements, you must still meet CRA obligations for maintaining charitable status. These are two distinct compliance frameworks.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)