Can a University Outside Canada Become a Qualified Donee?

Published on

March 26, 2024

Last updated on

April 27, 2026

A university located outside Canada can become a qualified donee under the Income Tax Act — but only if it meets specific criteria set by the Canada Revenue Agency (CRA) and completes a formal registration process. This matters for two groups: Canadian individuals who want to donate to a foreign university and claim a tax credit, and Canadian registered charities that can only make gifts to qualified donees.

Here is what foreign educational institutions need to know about eligibility, the application process, and ongoing obligations.

What is a Qualified Donee?

A qualified donee is an organization that is authorized under the Income Tax Act to issue official donation receipts for Canadian income tax purposes. When a donor makes a gift to a qualified donee, they can claim a charitable donation tax credit on their Canadian income tax return.

Qualified donees are also the only entities that Canadian registered charities are legally permitted to make gifts to. This means a foreign university that is not registered as a qualified donee cannot receive gifts from a Canadian registered charity — doing so would put the Canadian charity at risk of a compliance violation and CRA scrutiny.

Why Qualified Donee Status Matters

For Canadian donors, qualified donee status is the gateway to a tax credit. A gift to a foreign university that is not registered as a qualified donee does not entitle the donor to any credit on their Canadian tax return — no matter how well-regarded the institution is internationally.

For Canadian registered charities, the stakes are equally high. If a Canadian charity wants to support a foreign university — for example, through a research grant or scholarship fund — that university must appear on the CRA's public list of qualified donees. Without that status, the transfer may be treated as a compliance violation and could result in penalties or audits.

Getting on the CRA's list is therefore not only desirable for foreign universities — in many cases it is a prerequisite for receiving Canadian funding at all.

Criteria for Eligibility

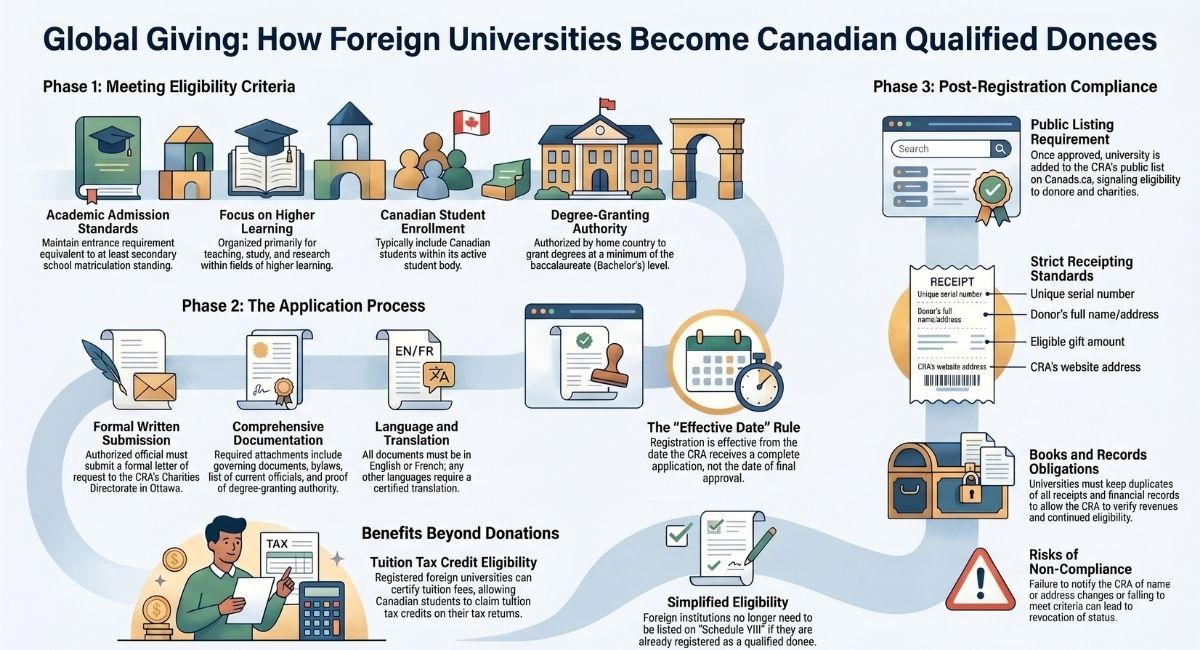

To be eligible for qualified donee status, a foreign educational institution must satisfy all four of the following criteria under the Income Tax Act. The CRA will assess each criterion based on the institution's governing documents and supporting materials submitted with the application.

- Academic Admission Requirements: The institution must maintain an academic entrance requirement equivalent to at least secondary school matriculation standing.

- Teaching, Study, and Research: It must be organized for teaching, study, and research in fields of higher learning.

- Enrolment of Canadian Students: The institution should typically include Canadian students in its student body.

- Degree-Granting Authority: It must have the authority to grant degrees at minimum at the baccalaureate level (bachelor's degree or equivalent), as recognized by the appropriate educational authority in its country.

The CRA will not register an institution that only partially meets these criteria. All four must be satisfied simultaneously, and the onus is on the applying institution to demonstrate compliance through its documentation.

Application Process

If a university outside Canada meets the eligibility criteria, it can apply for qualified donee status by submitting a written application to the CRA's Charities Directorate. The process is outlined in CRA Information Sheet RC191. Here is how it works.

- Submission: An official or authorized representative of the institution must send a letter to the CRA's Charities Directorate stating that the institution is requesting qualified donee status.

- Required Information: The letter must include, or be accompanied by, all of the following:

- The institution's legal name, mailing address, physical address, and phone number(s)

- A list of all current officials, such as directors, trustees, and equivalent officers

- A copy of the institution's complete governing documents, including incorporating documents, any amendments, and current bylaws

- The institution's general admission requirements

- A copy of documents issued by the appropriate educational authority in the institution's country, confirming it is an institution of higher learning with degree-granting authority at minimum at the baccalaureate level

- A list of the degrees the institution grants

- Language Requirements: All documents must be submitted in English or French. Documents in any other language must be accompanied by a certified English or French translation.

- Authorization: The CRA can only communicate with the institution's officials (director, trustee, or equivalent) or individuals the institution has formally authorized. To authorize a representative handling the application, follow the CRA's representative authorization process.

- Where to Send the Application: Mail the application letter and all supporting documents to:

Assessment, Determinations, and Monitoring Division Charities Directorate Canada Revenue Agency Ottawa ON K1A 0L5 Canada

The CRA cannot register an institution as a qualified donee without a complete submission. An incomplete application will not be treated as received and will delay the process.

Assessment and Registration

Once the CRA receives a complete application, it will review the submission against the eligibility criteria under the Income Tax Act.

If approved: The CRA will send the institution a letter confirming its qualified donee registration as a university outside Canada. The institution's name, location, and effective date of registration will be added to the CRA's publicly available list of qualified donees on Canada.ca. This public listing is important — it signals to Canadian donors and registered charities that the institution is eligible to receive Canadian gifts.

Effective date: The effective date of registration is the date the CRA received the complete application — not the date the approval letter was issued. This means that once approved, an institution can issue receipts for gifts received from the date the complete application was received.

If denied: If the institution does not meet the requirements, the CRA will send a letter explaining why the application was denied. The institution may reapply if it is able to address the deficiencies identified.

What Must Appear on an Official Donation Receipt

Once registered, a university outside Canada that receives a gift must issue official donation receipts that comply with the Income Tax Regulations. The information on a receipt must be legible and presented in a way that cannot be easily altered.

For cash gifts, a receipt must include:

- A statement that it is an official receipt for income tax purposes

- The name and address of the qualified donee

- A unique serial number

- The location where the receipt was issued (city, town, or municipality)

- The date the gift was received and the date the receipt was issued

- The full name, including middle initial, and address of the donor

- The amount of the gift

- The amount and description of any advantage received by the donor

- The eligible amount of the gift

- The signature of an individual authorised by the institution to acknowledge gifts

- The name and website address of the CRA

For non-cash gifts, the receipt must also include a brief description of the gift received, and the name and address of the appraiser if the gift was appraised. The amount of a non-cash gift must be its fair market value at the time the gift was made.

Books and Records Obligations

To maintain their qualified donee status, registered universities outside Canada must keep adequate books and records. These must include:

- Information that allows the CRA to verify revenues for which donors can claim tax credits or deductions

- Information that confirms the institution continues to meet qualified donee requirements under the Income Tax Act

- A duplicate of each official donation receipt issued

Books and records may be maintained in the institution's home country, but must be made available to the CRA in Canada upon request. Records include financial statements supporting any donation receipts issued, as well as source documents such as cancelled cheques and bank deposit slips.

Ongoing Compliance and Revocation

A registered university outside Canada must notify the CRA of any changes to its information, including a new legal name, address, or governing documents, so that the CRA's public list remains accurate.

The CRA has the authority to revoke a university's qualified donee registration under the Income Tax Act (ITA 149.1(4.3) and 168(1)) if the institution no longer meets the eligibility criteria or fails to comply with its obligations. Revocation means the institution can no longer issue official Canadian donation receipts, and Canadian registered charities can no longer make gifts to it. The CRA will issue a notice of revocation before taking this step.

Tuition Tax Credit — What Canadian Students Should Know

Foreign educational institutions that are registered qualified donees are also considered universities outside Canada for purposes of the tuition tax credit under the Income Tax Act. Importantly, it is no longer a requirement for foreign institutions to be prescribed and listed on Schedule VIII of the Income Tax Regulations — registration as a qualified donee is now sufficient.

If a Canadian student attends a registered university outside Canada, the institution may certify tuition fees to support the student's claim for the tuition tax credit on their Canadian income tax and benefit return. Students should confirm their institution appears on the CRA's public list of qualified donees before filing.

Frequently Asked Questions

Can a university outside Canada issue Canadian donation receipts?

Yes, but only if it is registered as a qualified donee by the CRA. Once registered, the institution can issue official donation receipts that allow Canadian donors to claim a charitable donation tax credit on their income tax return.

Can a Canadian registered charity donate to a foreign university?

Only if the foreign university is a registered qualified donee. Canadian registered charities are legally prohibited from making gifts to entities that are not qualified donees. Doing so could result in compliance violations and CRA penalties.

How does a foreign university apply for qualified donee status?

An official or authorized representative must send a letter to the CRA's Charities Directorate in Ottawa, along with governing documents, admission requirements, a list of degrees granted, and proof of degree-granting authority from the appropriate educational authority in the institution's country.

Where can I find the list of registered universities outside Canada?

The CRA maintains a public list of registered universities outside Canada on Canada.ca. Search for "List of universities outside Canada registered as qualified donees" or go directly to the CRA's qualified donees listings page.

What happens if a foreign university loses qualified donee status?

If the CRA revokes a university's qualified donee registration, the institution can no longer issue official Canadian donation receipts and Canadian registered charities can no longer make gifts to it. The CRA must issue a notice of revocation before this takes effect.

Does a foreign university need to re-apply every year?

No. Registration does not require annual renewal. However, the institution must continue to meet all eligibility criteria and comply with its ongoing obligations. The CRA can revoke registration at any time if those requirements are no longer met.

Is there a fee to apply for qualified donee status as a foreign university?

The CRA does not charge a fee to apply. However, preparing a complete application — including certified translations, governing documents, and legal authorizations — may involve professional costs. Working with a Canadian charity lawyer can help ensure the application is complete and accurate.

The Bottom Line

Qualified donee status gives a foreign university access to Canadian donations — both from individual donors claiming tax credits and from Canadian registered charities. The registration process requires a complete, well-documented application to the CRA's Charities Directorate, and the obligations do not end at registration. Ongoing compliance, proper receipting, and adequate record-keeping are all conditions of maintaining that status.

If your organization is looking to donate to a foreign university, or if a foreign educational institution wants to pursue qualified donee status in Canada, the rules are detailed and the consequences of getting them wrong can be significant. Speaking with a Canadian charity lawyer before taking action is strongly recommended.

CRA Resources

- List of registered universities outside Canada – CRA

- Registered universities outside Canada – obligations overview

- RC191 – Applying for qualified donee status as a university outside Canada

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)