What Does "At Arm's Length" Mean for Canadian Charities and Nonprofits?

Published on

June 18, 2025

Last updated on

July 5, 2026

"At arm's length" is one of the most important — and most misunderstood — concepts in Canadian charity law. It determines how the CRA classifies your charity, whether your board decisions hold up under scrutiny, and what penalties apply when related parties transact with each other. This guide explains exactly what arm's length means under the Income Tax Act, who counts as a non-arm's length party, and how to stay compliant in 2026.

What Does "At Arm's Length" Mean?

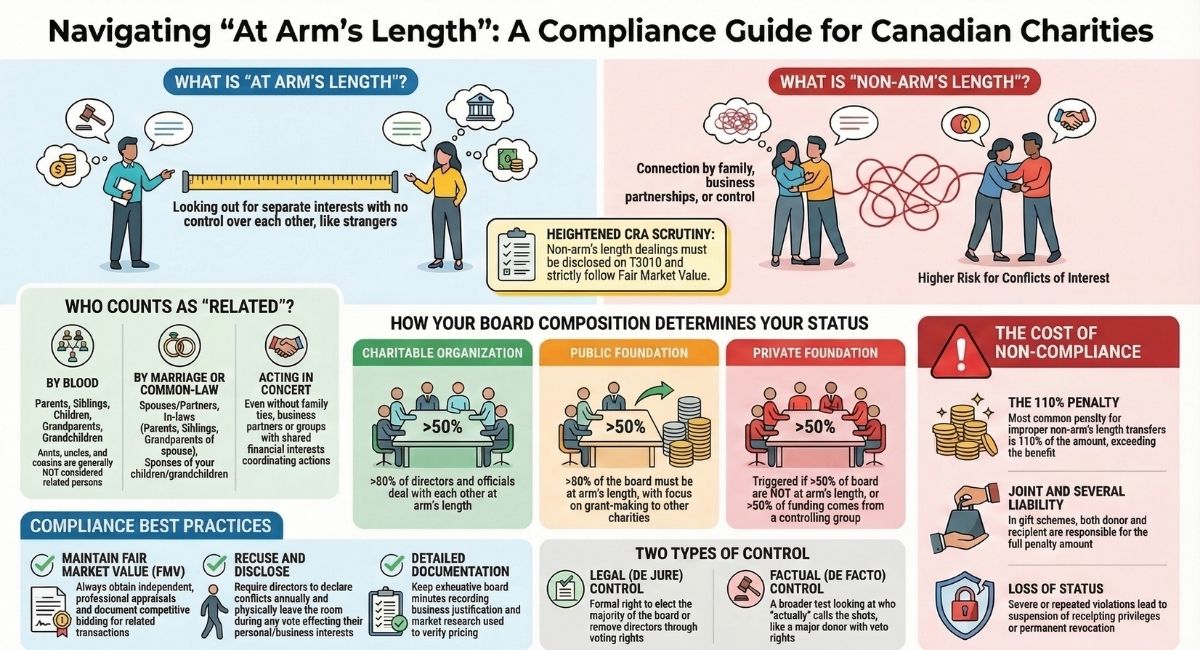

"At arm's length" means two people or organizations are acting independently and are not connected in a way that might affect their decisions. Imagine two strangers making a deal. Neither one controls nor influences the other. They each look out for their own best interest.

This is important because it ensures fair and honest transactions. When two parties deal at arm's length, the deal is made as if they are unrelated.

For Canadian registered charities specifically, this applies to relationships with directors, donors, related organizations, and service providers. When parties deal at arm's length, they negotiate fairly and act in their own separate interests, just like strangers would in a business deal. While nonprofits should also maintain appropriate independence, the specific penalties and compliance requirements discussed in this article—such as financial penalties, suspension, or revocation—apply to registered charities under the Income Tax Act.

Arm's length parties are independent and make decisions separately. They have no personal relationships, family connections, or business ties that could influence their judgment.

Non-arm's length parties have connections that affect their independence, including family relationships or one party controlling the other. This can include family members, business partners, or companies controlled by the same person.

The key difference is whether parties can act completely independently. Non-arm's length relationships need extra scrutiny because there's higher risk of conflicts of interest.

Who Is Considered "Not at Arm's Length"?

The Canada Revenue Agency (CRA) defines related persons as individuals who are related to each other by blood, marriage, common-law partnership, or adoption.

Related by Blood

Examples of blood relatives include:

- Grandparents

- Parents

- Brothers and sisters

- Children

- Grandchildren

Important Note: Aunts, uncles, nieces, nephews, and cousins are generally NOT considered "related persons" for tax purposes under the Income Tax Act. This is a common point of confusion. While these extended family relationships may create ethical considerations or the appearance of conflict, they do not automatically trigger non-arm's-length status for CRA compliance purposes.

Related by Marriage or Common-Law Partnership

The CRA treats common-law partners the same as legally married spouses. Examples of persons related by spousal relationship include:

- The grandparents of a spouse or common-law partner

- The parents of a spouse or common-law partner

- The brothers and sisters of a spouse or common-law partner

- The children of a spouse or common-law partner

- The spouse of a brother or sister

- The spouse of a child

- The spouse of a grandchild

Acting in Concert

Beyond family relationships, parties are also considered not at arm's length when they act in concert without separate interests. This includes:

- Business partners working together

- People with close business ties

- Individuals who share a common financial interest

- Parties where one person has significant influence over another's decisions

Quick Checklist: Are You Dealing at Arm's Length?

Use this checklist to assess whether a relationship triggers non-arm's length rules under the CRA.

- ☐ Is the other party a spouse, common-law partner, or blood relative (parent, sibling, child, grandparent)?

- ☐ Is the other party a spouse or parent of a board member or staff member?

- ☐ Does one party have the power to elect or remove the other's directors?

- ☐ Does one party depend on the other for the majority of its funding?

- ☐ Do they share a common business interest or investment?

- ☐ Does one party hold veto rights over the other's decisions?

- ☐ Have they coordinated their actions to serve a shared purpose?

If you answered yes to any of the above, the parties are likely not at arm's length. All transactions between them must be at fair market value, properly documented, and disclosed on the T3010.

Why Arm's Length Matters for Canadian Charities

Charities and nonprofits must follow special rules to keep their status and make sure they use their resources properly. If they buy or sell something, or make agreements with other people or groups, they need to make sure these deals are fair.

For example, if a charity buys something from a person who is very close to someone in the charity, like a family member or a business partner, this might not be an arm's length deal. This could lead to questions about whether the charity is paying a fair price or if someone is getting special treatment.

CRA Oversight

The CRA monitors arm's length relationships carefully because:

- Charities receive tax-exempt status and can issue donation receipts

- Public trust depends on charities operating transparently

- Charitable assets must be used exclusively for charitable purposes

- Insiders should not benefit personally from their association with the charity

Consequences of Violations

Violations can lead to:

- Financial penalties of 110% of amounts improperly transferred or not expended

- Loss of ability to issue tax receipts

- Suspension of charitable status

- Complete revocation of charitable registration

- Joint liability for both donor and recipient charities in gift schemes

Understanding these rules helps organizations maintain independence and compliance.

What's Changed in 2025–2026: Arm's Length and CRA Compliance

The regulatory landscape for Canadian charities has shifted in ways that directly affect how arm's length rules are applied and enforced. Here's what's new for 2026.

Disbursement Quota Increase

Since Budget 2023, charities with investment assets over $1 million must disburse 5% annually — up from the previous 3.5% rate. This higher quota directly affects how non-arm's length gift transfers are tracked and expended. Charities that previously relied on transfers between related organizations to satisfy their disbursement quota may now find those arrangements fall short or invite greater scrutiny.

Increased CRA Audit Activity

The CRA has increased its audit focus on charities with related-party transactions, board composition issues, and non-arm's length disbursements. In 2025 and into 2026, more charities are receiving compliance letters and desk audits specifically flagging these concerns. If your charity has received a CRA compliance letter, arm's length violations are among the most common reasons cited.

Tightened T3010 Reporting

The CRA has updated its T3010 guidance to require more detailed disclosure of transactions with non-arm's length parties — including the nature of the relationship, the value of the transaction, and the documentation held by the charity. Incomplete or vague T3010 disclosures are themselves a compliance risk.

Types of Charity Designations and Arm's Length Requirements

The CRA assigns one of three designations to registered charities, and arm's length relationships directly affect which designation your charity receives.

Charitable Organization

A charitable organization primarily carries on its own charitable activities. To qualify as a charitable organization:

- More than 50% of directors, trustees, or officials must deal at arm's length with each other

- The organization generally receives funding from a variety of arm's length donors

- It can be incorporated, established by constitution, or created as a trust

Public Foundation

A public foundation generally gives more than 50% of its income to qualified donees (usually other registered charities). To qualify as a public foundation:

- More than 50% of directors, trustees, or officials must deal at arm's length with each other

- The foundation receives funds from arm's length donors

- It focuses on grant-making rather than operating programs

Private Foundation

A private foundation may carry on its own activities and give income to qualified donees. A charity is designated as a private foundation when:

- 50% or more of directors, trustees, or officials do NOT deal with each other at arm's length, OR

- More than 50% of funding comes from a person or group of persons who control the charity or make up more than 50% of the directors

Impact of Designation

Your charity's designation affects:

- Disbursement quota requirements

- Restrictions on business activities

- Ability to transfer funds to other charities

- Compliance and reporting obligations

Important note: If your charity has only one director, trustee, or official, it will automatically be designated as a private foundation. This is because it's impossible to have more than 50% of directors at arm's length when there's only one person.

Understanding Legal Control vs. De Facto Control

The CRA examines two types of control when assessing arm's length relationships: legal control and de facto control. Understanding both is essential for compliance.

Legal Control (De Jure Control)

Legal control is determined by the right to elect the majority of the board of directors. This is the traditional, straightforward test for control:

- Who has the power to vote for board members?

- Who can remove directors?

- What percentage of voting rights does a person or group hold?

De Facto Control (Factual Control)

De facto control is broader than legal control. It exists when a person has directly or indirectly, in any manner whatever, influence that, if exercised, would result in control in fact of the organization.

The CRA looks at the practical reality of who truly controls the charity, regardless of formal legal structures.

Indicators of De Facto Control

The CRA may find de facto control exists when:

- A charity depends on a single donor or small group of donors for the majority of its funding

- A person or entity has veto rights over major decisions

- Exclusive service contracts create dependency on a particular supplier

- One person dominates board discussions and decisions despite not holding a formal majority

- A charity cannot continue operations without the support of a particular individual or organization

Why Both Matter

A charity might appear to have an arm's length board based on legal structure, but the CRA can look beyond formal arrangements to assess the true nature of relationships. Both tests help ensure charities maintain genuine independence.

How Arm's Length Affects Charity Operations

Arm's length relationships impact several key areas of charity operations.

Board Composition

Directors help run charities and nonprofits. They make important decisions and must act honestly and fairly.

At arm's length directors are people who are independent of each other. They do not have close relationships or personal ties that might influence their decisions.

Having directors at arm's length is important because it helps prevent conflicts of interest. For example, if two directors are family members or business partners, they may not be considered at arm's length. This could lead to decisions that benefit a few people instead of the whole charity.

Best practices for board composition:

- Recruit diverse board members without family ties or business relationships with each other

- Limit related individuals serving together

- Avoid letting family or business partners dominate your board

- Ensure a strong majority of independent members

- Document all board decisions carefully, especially those involving payments to connected parties

Transactions and Contracts

For example, if a charity buys something from a person who is very close to someone in the charity, like a family member or a business partner, this might not be an arm's length deal. This could lead to questions about whether the charity is paying a fair price or if someone is getting special treatment.

If a charity or nonprofit makes a deal that is not at arm's length, the CRA might review it to check if the terms were fair. If not, the charity could face penalties or risk losing its status.

Gift Transfers Between Related Charities

When charities transfer funds between organizations that are not at arm's length, special rules apply:

Disbursement Requirements: When a charity receives a gift (other than a designated gift) from another charity with which it does not deal at arm's length, it must expend an amount equal to the fair market value of the property. This expenditure must be:

- In addition to its regular disbursement quota for each taxation year

- Made before the end of the next taxation year

- Spent on the charity's own charitable activities OR

- Transferred as qualifying disbursements to qualified donees or grantee organizations with which the charity deals at arm's length

Penalties for Non-Compliance: Failure to meet these requirements triggers penalties of 110% of the amount not expended or gifted. This severe penalty discourages charities from using related-party transfers to avoid their disbursement obligations.

Joint Liability: Both the donor charity and the recipient charity can be held jointly, severally, or solidarily liable for penalties if:

- The donor charity intended to help avoid or delay expenditures on charitable activities

- The recipient charity knowingly accepted the gift for this purpose

- If the donor charity cannot pay the penalty in full, the recipient charity becomes liable for the outstanding balance

Fair Market Value Requirements

All non-arm's length transactions must be conducted at fair market value to avoid private benefit concerns.

What is Fair Market Value?

Fair market value is the highest dollar value you can get for property in an open and unrestricted market, between a willing buyer and a willing seller who are:

- Knowledgeable about the property

- Informed about market conditions

- Acting independently of each other

- Under no compulsion to complete the transaction

When Fair Market Value Matters:

- Purchasing property from directors or related parties

- Renting space from connected individuals or companies

- Hiring related parties for services

- Accepting donations of property from non-arm's length donors

- Selling charity assets to insiders

Documentation Requirements:

- Obtain independent, professional appraisals for significant transactions

- Document competitive bidding processes

- Keep written records of how fair market value was determined

- Maintain evidence of market research and comparisons

- Record board discussions and decisions regarding non-arm's length transactions

Common Arm's Length Violations to Avoid

Understanding common violations helps charities maintain compliance with CRA requirements.

Hiring Family Members Without Proper Process

The Violation: Hiring family members or relatives of board members without posting positions publicly or conducting competitive recruitment.

Why It's Problematic: This creates an appearance of nepotism and private benefit. Even if the person is qualified, the lack of process suggests the charity isn't acting in its best interests.

How to Avoid It:

- Post all positions publicly

- Conduct competitive recruitment

- Have the related board member or staff person recuse themselves from hiring decisions

- Ensure compensation is at fair market value

- Document the entire hiring process

- Disclose the relationship in board minutes and on the T3010

Purchasing from Director-Owned Businesses at Inflated Prices

The Violation: Regularly purchasing supplies or services from companies owned by directors or their relatives, paying prices significantly above market rates.

Why It's Problematic: The director benefits personally from their position on the board, constituting private benefit. The charity wastes charitable resources.

How to Avoid It:

- Obtain competitive bids for all significant purchases

- Require the director to disclose their interest

- Have the director recuse themselves from procurement decisions

- Document fair market value comparisons

- Consider establishing a policy that limits or prohibits such transactions

Making Loans to Directors or Related Parties

The Violation: Providing loans to board members or to companies owned by board members or their families.

Why It's Problematic: Charitable assets are being used for private benefit. Even interest-bearing loans can be problematic if terms are more favourable than market conditions.

How to Avoid It:

- Establish a policy prohibiting loans to directors and related parties

- If loans are absolutely necessary, ensure they are at fair market interest rates, properly secured, documented with written loan agreements, approved by disinterested directors only, and disclosed on the T3010

Renting Property from Related Parties Without Market Comparisons

The Violation: Renting office space or property from board members or their relatives without obtaining independent rental valuations.

Why It's Problematic: The related party receives rent payments, potentially creating private benefit if rates exceed market value.

How to Avoid It:

- Obtain independent appraisals or rental comparisons

- Document why the rental arrangement benefits the charity

- Ensure rent is at or below fair market value

- Review rental rates annually

- Consider alternative arrangements if market-rate options are available

Entering Exclusive Contracts with Related Entities

The Violation: Signing multi-year exclusive contracts with businesses owned by directors or their business partners, preventing the charity from seeking better terms elsewhere.

Why It's Problematic: The charity loses flexibility and may pay above-market rates. The exclusive nature suggests the arrangement benefits the related party rather than the charity.

How to Avoid It:

- Avoid exclusive arrangements with related parties

- If unavoidable, ensure contracts include fair market pricing with annual reviews, performance benchmarks, termination clauses, and independent verification of value

- Have disinterested directors approve the arrangement

- Document the business justification thoroughly

Failing to Disclose Conflicts of Interest

The Violation: Directors voting on matters affecting their personal interests without disclosing the conflict to the board.

Why It's Problematic: This violates fiduciary duties and can invalidate board decisions. It creates legal liability and damages public trust.

How to Avoid It:

- Implement a comprehensive conflict of interest policy

- Require annual disclosure statements from all directors

- Create a conflict of interest register

- Train directors to recognize and disclose conflicts

- Require immediate disclosure when conflicts arise

- Document all disclosures and how conflicts were managed

Inadequate Documentation

The Violation: Entering into transactions with related parties but failing to document why the terms are fair or how decisions were made.

Why It's Problematic: Without documentation, the charity cannot prove compliance during a CRA audit. The lack of records suggests poor governance.

How to Avoid It:

- Maintain detailed board minutes

- Document fair market value determinations

- Keep competitive bid records

- File all disclosure forms

- Preserve appraisals and valuations

- Record the rationale for decisions involving related parties

Penalties and Consequences for Arm's Length Violations

The CRA has significant enforcement powers to address non-compliance with arm's length rules. Understanding potential penalties helps charities take compliance seriously.

Financial Penalties

110% Penalties: The most common penalty for arm's length violations is 110% of the improper amount. This applies to:

- Delayed expenditures on charitable activities (subsection 188.1(11) of the Income Tax Act)

- Gifts received from non-arm's length charities and not properly expended (subsection 188.1(12))

- Amounts transferred in schemes designed to avoid disbursement quotas

How It Works: If a charity improperly handles $50,000 in a non-arm's length transaction, the penalty is $55,000 (110% of $50,000). This ensures violations cost more than compliance.

Penalties for False Information: Under subsection 188.1(9), penalties apply when a charity or any person involved provides false information on receipts or returns. This can affect the charity itself, individual directors or officers, and authorized representatives or advisors.

Suspension of Charitable Status

A suspension temporarily removes a charity's ability to issue donation receipts. During suspension:

- The charity cannot issue official donation receipts

- The charity remains registered but loses a key fundraising tool

- The suspension appears on the CRA's public charity listings

- Public trust and donor confidence may be damaged

Grounds for Suspension include:

- Receiving gifts from non-arm's length charities and failing to expend them properly

- Having an ineligible individual as a director, trustee, officer, or someone who controls or manages the charity

- Making false statements on the T3010 or in receipt documentation

- Other breaches that warrant intermediate sanctions

Revocation of Charitable Status

Revocation is the complete loss of charitable registration. This is the most severe penalty and is permanent (though charities can reapply for registration after addressing the issues).

Consequences of Revocation:

- Immediate loss of tax-exempt status

- Permanent inability to issue donation receipts (unless re-registered)

- Revocation tax on remaining assets (calculated at corporate tax rates)

- Public listing of the revocation on CRA databases

- Severe damage to reputation

- Potential requirement to wind up operations or transfer assets to other charities

Grounds for Revocation related to arm's length include:

- Accepting gifts from foreign states on designated lists

- Having an ineligible individual control or manage the charity

- Repeated violations after warnings and penalties

- Serious breaches demonstrating the charity is not operated exclusively for charitable purposes

- Conferring undue private benefits on non-arm's length parties

Joint and Several Liability

When charities participate in schemes involving non-arm's length transfers:

- Both the donor and recipient charity can be held responsible for penalties

- If one charity cannot pay, the other becomes liable for the full amount

- This prevents charities from claiming they didn't know about improper arrangements

Intermediate Sanctions

Before proceeding to revocation, the CRA may impose intermediate sanctions designed to correct behaviour while allowing the charity to continue operating. These include:

- Financial penalties proportional to the violation

- Temporary suspensions

- Compliance agreements requiring specific corrective actions

- Increased reporting and monitoring requirements

Audit Triggers

Certain activities increase the likelihood of a CRA audit:

- Significant transactions with related parties

- Changes in charity designation

- Unusually low disbursement quotas

- Transfers between related charities

- Board composition with multiple family members

- Receipting irregularities

- Public complaints about conflicts of interest

Real-Life Examples of Arm's Length Issues in Canadian Charities

Understanding how arm's length rules apply in practice helps charities recognize and avoid similar problems. These examples are drawn from actual situations faced by Canadian charities.

Example 1: The Trinity Christian School Association Case

The Situation: Trinity Christian School Association in Alberta received government funding to support home schooling initiatives. Questions arose about how those funds were used and whether transactions involved entities and individuals who were not at arm's length with the association.

The Arm's Length Issue: Concerns focused on whether transactions occurred between the charity and related parties without proper independence. When charities receive public funds, the scrutiny intensifies because taxpayers expect transparent use of government money.

The Lesson: This case demonstrates that arm's length rules matter not just for CRA compliance but also for other funding relationships. Even when a charity thinks relationships are appropriate, the appearance of conflicts can trigger investigations. Charities receiving government grants must be especially careful about maintaining independence in all transactions.

Key Takeaway: Whether or not Trinity Christian School Association violated arm's length rules, the controversy damaged its reputation and created significant legal costs. Prevention through proper policies is far less expensive than defending against allegations.

Example 2: The Family-Controlled Foundation

The Situation: A family established a charity to support youth education programs. The board consisted of a father, mother, their son, their daughter, and one family friend (five people total, with four being blood relatives).

The Arm's Length Issue: With four of five board members related by blood, more than 50% of directors were not at arm's length. Despite the charity's charitable purposes being legitimate, the board composition automatically triggered private foundation designation.

The Impact: As a private foundation, the charity faced:

- Stricter disbursement quota requirements

- Additional compliance obligations

- Restrictions on certain activities available to charitable organizations

- Enhanced CRA scrutiny of transactions

The Solution: The family had two options:

- Accept private foundation status and comply with additional requirements

- Restructure the board to include a majority of independent, arm's length directors to qualify as a public foundation or charitable organization

They chose to add three independent community leaders to the board, creating an eight-person board where only four members were related. This allowed redesignation as a public foundation.

Key Takeaway: Board composition directly affects your charity's designation and compliance obligations. Families wanting to establish charities while maintaining some involvement need to balance participation with the benefits of having arm's length directors.

Example 3: The Property Purchase Problem

The Situation: A community arts charity needed new gallery space. The board chair's spouse owned a commercial property that could work well. The spouse offered to sell the property to the charity for $850,000.

The Arm's Length Issue: The board chair disclosed the spousal relationship but pushed for a quick decision, arguing the property was perfect for the charity's needs. The board voted to proceed without:

- Obtaining an independent appraisal

- Comparing prices of similar properties

- Having the board chair recuse themselves from discussions

- Documenting why this price was fair market value

The CRA Review: During a routine audit two years later, the CRA questioned the transaction. An independent appraisal obtained by the CRA valued the property at $625,000 at the time of purchase. The charity had overpaid by $225,000.

The Consequences:

- The CRA determined the charity conferred a private benefit of $225,000 on the board chair's spouse

- The charity faced penalties for the excessive payment

- The board chair was required to resign

- The charity's reputation suffered when the overpayment became public

- The charity struggled to recover the excess amount paid

The Proper Approach Would Have Been:

- Board chair discloses the relationship immediately

- Board chair recuses themselves from all discussions and votes

- Charity obtains independent appraisal from qualified real estate appraiser

- Charity researches comparable properties

- Independent directors evaluate whether purchase is in charity's best interest

- If proceeding, ensure price is at or below fair market value

- Document the entire process thoroughly

- Disclose the transaction on the T3010

Key Takeaway: Non-arm's length property transactions require exceptional diligence. The cost of proper appraisals and documentation is minimal compared to the cost of penalties and reputation damage.

Example 4: The Consulting Contract Arrangement

The Situation: A healthcare charity hired a consulting firm to provide strategic planning services. The contract was for $180,000 over two years. What the charity failed to disclose was that the consulting firm was owned by the business partner of one of the charity's directors.

The Arm's Length Issue: The director knew about the connection but didn't consider it a conflict because the director didn't personally own the consulting firm and believed the rates were "competitive." However, the business partner relationship meant the parties were acting in concert without separate interests—classic non-arm's length dealing.

The Discovery: Another board member discovered the connection while reviewing invoices and noticed the consulting firm's principal was someone they knew to be the director's business partner.

The Investigation Revealed:

- The consulting rate was $250/hour, significantly above the $150-175/hour market rate for similar services

- No competitive bidding process had occurred

- The director participated in discussions and voted on the contract

- The excessive rates cost the charity approximately $85,000 over the contract period

The Outcomes:

- The director was removed from the board

- The charity demanded repayment of excess fees from the consulting firm

- The CRA imposed penalties for conferring private benefits

- Several major donors withdrew support upon learning about the arrangement

- The charity implemented strict conflict of interest policies

What Should Have Happened:

- Director discloses the business partner relationship before any discussion

- Director recuses themselves completely from the procurement process

- Charity conducts competitive RFP process

- Charity obtains quotes from at least three firms

- Independent directors evaluate proposals on merit

- If the connected firm is selected, ensure rates are at or below market

- Document justification for selection

- Monitor contract performance by independent directors

Key Takeaway: Indirect connections through business partners still create non-arm's length relationships. Directors must disclose any relationship that could influence their judgment, even when they don't directly benefit financially.

Example 5: The Gift Transfer Scheme

The Situation: Three charities—all controlled by members of the same extended family—transferred funds among themselves in a circular pattern:

- Charity A received a large bequest of $500,000

- Charity A transferred $300,000 to Charity B

- Charity B transferred $250,000 to Charity C

- Charity C transferred $200,000 back to Charity A

The Arm's Length Issue: All three charities had overlapping boards with family members, making them non-arm's length. The circular transfers suggested the charities were trying to avoid disbursement quota requirements rather than furthering charitable purposes.

The CRA Investigation Found:

- None of the charities expended the required amounts on actual charitable activities

- The transfers appeared designed to create the appearance of meeting disbursement requirements

- Funds were essentially "parked" rather than used for charitable purposes

- The scheme allowed the charities to maintain assets while claiming disbursement compliance

The Penalties:

- Each charity faced 110% penalties on amounts not properly expended

- Charity A: $330,000 penalty (110% of $300,000)

- Charity B: $275,000 penalty (110% of $250,000)

- Charity C: $220,000 penalty (110% of $200,000)

- All three charities were jointly liable for each other's penalties

- Total potential liability exceeded $800,000

The Broader Consequences:

- All three charities had their registrations revoked

- The family lost control of approximately $1.2 million in charitable assets

- The assets were distributed to arm's length qualified donees

- The case was publicized as a warning to other charities

Key Takeaway: The CRA looks beyond form to substance. Transferring funds between related charities must serve genuine charitable purposes, not administrative convenience or tax planning. When charities are not at arm's length, every transfer receives heightened scrutiny.

Example 6: The Rental Agreement Problem

The Situation: A nonprofit arts organization rented office space from a property management company owned by the spouse of the organization's executive director. The monthly rent was $4,500 for a 2,000 square-foot space.

The Arm's Length Issue: The executive director failed to disclose that their spouse owned the property management company. The board approved the rental agreement without knowing about the relationship or conducting market research on comparable rental rates.

The Discovery: A new board member with real estate experience noticed the rent seemed high and researched comparable properties. Similar spaces in the area rented for $2,800-$3,200 per month. The board member raised concerns, triggering an internal investigation.

The Investigation Revealed:

- The charity had been overpaying approximately $1,500 per month for three years

- Total excess payments of approximately $54,000

- The executive director had participated in negotiating the lease

- No competitive process or market comparison had been conducted

- The relationship was never disclosed to the board or on the T3010

The Outcomes:

- The executive director was terminated for failure to disclose the conflict

- The charity renegotiated the lease at market rates

- The CRA audit resulted in penalties for private benefit

- The charity recovered a portion of overpaid rent through legal action

- The organization implemented mandatory annual conflict of interest disclosures

What Should Have Happened:

- Executive director discloses spousal ownership before lease discussions

- Executive director recuses themselves from all lease negotiations

- Board obtains independent rental market analysis

- Board considers multiple properties through competitive process

- If spouse's property is selected, ensure rent is at or below market rate

- Document decision-making process thoroughly

- Disclose relationship on T3010 and in financial statements

- Review rental rates annually against market conditions

Key Takeaway: Staff members have the same disclosure obligations as directors when personal relationships create conflicts. Spouses and common-law partners of staff must be treated as non-arm's length parties, and all transactions must be disclosed and conducted at fair market value.

Common Themes from These Examples

These real-life situations illustrate several important principles:

- Disclosure is Essential: Every example involved failures to disclose relationships or inadequate disclosure. Transparency is the foundation of compliance.

- Documentation Matters: Charities that failed to document their decision-making processes faced the most severe consequences. Good records protect charities during audits.

- Fair Market Value is Non-Negotiable: Transactions with related parties must meet or beat market standards, not merely seem reasonable. Independent verification is critical.

- Independence Protects Charities: Charities with truly independent boards avoided these problems or caught issues before they became serious. Arm's length directors provide essential oversight.

- The Appearance of Conflict is Dangerous: Even when no wrongdoing is proven, the perception of impropriety damages charity reputations and donor trust. Prevention is better than defence.

- Professional Advice is Cost-Effective: In every case, the cost of obtaining proper legal and professional advice would have been a fraction of the penalties and consequences faced. Expert guidance saves money and protects status.

- Indirect Relationships Count: Business partners, spouses of staff members, and extended family all create non-arm's length relationships. The CRA looks beyond direct ownership to examine true influence.

- The CRA Looks Beyond Form to Substance: Circular transactions, technical compliance without genuine charitable purpose, and arrangements designed to circumvent rules will be scrutinized and penalized.

Best Practices for Maintaining Arm's Length Compliance

Following these practices helps charities avoid violations and maintain strong governance.

Develop Clear Policies

Create clear conflict of interest policies requiring directors to:

- Declare connections and potential conflicts

- Step out of decisions where they have personal stakes

- Abstain from voting on matters affecting related parties

- Disclose relationships annually and when they arise

Recruit Diverse Boards

Always try to make deals with people or organizations at arm's length. Recruit diverse board members without family ties or business relationships with each other. Limit related individuals serving together and avoid letting family or business partners dominate your board.

Document Everything

Make sure directors are independent and do not have close relationships that affect decisions. If a deal involves related parties, keep clear records and proof that the terms are fair.

Document all board decisions carefully, especially those involving:

- Payments to connected parties

- Property transactions with related individuals

- Service contracts with non-arm's length suppliers

- Employment of relatives

- Any situation where conflicts exist

Seek Professional Advice

Ask for professional advice if unsure about a situation. Understanding arm's length relationships is essential for Canadian charities and nonprofits to maintain their registered status and avoid serious tax consequences.

The rules around legal control, de facto control, and related parties can be complex, and getting them wrong can result in penalties or loss of charitable status.

Implement Fair Market Value Processes

For all non-arm's length transactions:

- Obtain independent appraisals or valuations

- Conduct competitive bidding when possible

- Document market research

- Ensure prices meet or beat market rates

- Review arrangements periodically

Train Board Members

Provide training to all board members on:

- What constitutes an arm's length relationship

- How to identify conflicts of interest

- Disclosure requirements

- Decision-making processes when conflicts exist

- Consequences of non-compliance

Conduct Annual Reviews

Review your charity's compliance annually:

- Assess board composition

- Review all related-party transactions

- Update conflict of interest disclosures

- Ensure policies are followed

- Identify and address any concerns

Conclusion

With CRA audit activity increasing in 2026 and stricter T3010 disclosure requirements now in effect, there has never been a more important time to review your charity's arm's length compliance.

Understanding arm's length relationships is essential for Canadian charities and nonprofits to maintain their registered status and avoid serious tax consequences. The rules around legal control, de facto control, and related parties can be complex, and getting them wrong can result in penalties or loss of charitable status.

If you're uncertain about whether a relationship qualifies as arm's length or need guidance on structuring compliant transactions, don't navigate these waters alone. Contact B.I.G. Charity Law Group today for expert guidance. Reach us at dov.goldberg@charitylawgroup.ca or call 416-488-5888, visit CharityLawGroup.ca, and schedule a FREE consultation to discuss your organization's needs.

Frequently Asked Questions

Here are answers to common questions about arm's length relationships for Canadian charities and nonprofits.

What is charity arm's length?

Charity arm's length means two parties operate independently without one controlling or influencing the other. For Canadian charities, this applies to relationships with directors, donors, related organizations, and service providers. When parties deal at arm's length, they negotiate fairly and act in their own separate interests, just like strangers would in a business deal.

What is the difference between arm's length and non-arm's length?

Arm's length parties are independent and make decisions separately. Non-arm's length parties have connections that affect their independence, including family relationships or one party controlling the other. The key difference is whether parties can act completely independently. Non-arm's length relationships need extra scrutiny because there's higher risk of conflicts of interest.

What is the difference between a nonprofit and a charity in Canada?

A charity must have exclusively charitable purposes and register with the CRA. Charities can issue tax receipts and must follow strict rules. A nonprofit is broader and includes organizations like sports clubs or social groups that cannot issue tax receipts unless they're registered charities. Both must operate without private profit, but charities face more regulations.

Why is the concept of at-arm's-length relationships important for charities and nonprofits?

The concept protects charities from being misused for private benefit. The CRA uses arm's length rules to ensure charities serve public purposes, not personal interests of insiders. Violations can lead to penalties, loss of tax receipts, or losing charitable status. Understanding these rules helps organizations maintain independence and compliance.

What are best practices for board composition to support independent decision-making and avoid non-arm's-length concerns?

Recruit diverse board members without family ties or business relationships with each other. Limit related individuals serving together and avoid letting family or business partners dominate your board. Create clear conflict of interest policies requiring directors to declare connections and step out of decisions where they have personal stakes. Ensure a strong majority of independent members and document all decisions carefully, especially those involving payments to connected parties.

Legal Sources & References

- Income Tax Act (Canada), s. 251(1) & (2): Defines "related persons" (limits blood relationship to linear descendants/ascendants and siblings—excluding uncles/cousins).

- CRA Guidance CG-010: Explains the rules for "Qualified Donees" (Charities) vs. Nonprofits.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)